Insurance is a critical component of risk management for individuals and businesses worldwide. However, navigating the complex landscape of insurance law can be challenging, especially when legal issues arise. This comprehensive guide aims to provide a global perspective on the legal aspects of insurance, focusing on coverage and claims. We'll explore key concepts, common challenges, and best practices applicable across various jurisdictions.

Fundamentals of Insurance Law

Insurance law forms the foundation of the global insurance industry, governing the relationships between insurers, policyholders, and other stakeholders. Understanding these fundamentals is crucial for navigating the complex world of insurance. Let's explore the key concepts:

Definition and Purpose of Insurance

Insurance is a contract where one party (the insurer) agrees to compensate another party (the policyholder) for specified losses in exchange for regular premium payments.

Purpose: To transfer risk from the policyholder to the insurer, providing financial protection against potential future losses.

Key Principles of Insurance Law

Utmost Good Faith (Uberrima Fides)

Both parties must act with honesty and full disclosure.

Policyholders must disclose all material facts that could affect the risk.

Insurers must provide clear information about policy terms and conditions.

Insurable Interest

The policyholder must have a legitimate interest in the subject of insurance.

This interest must be financial and recognized by law.

Examples: Property ownership, familial relationships, business partnerships.

Indemnity

Insurance should restore the policyholder to their financial position before the loss.

Prevents policyholders from profiting from insurance claims.

Exceptions: Life insurance and valued policies.

Subrogation

Allows insurers to pursue third parties responsible for the insured loss.

Prevents double recovery by the policyholder.

Proximate Cause

Determines the primary cause of loss for coverage decisions.

Helps establish whether a loss is covered under the policy.

Types of Insurance Contracts

Indemnity Contracts

Most common type (e.g., property, liability insurance)

Compensates for actual financial loss up to policy limits

Non-Indemnity Contracts

Pays a fixed sum upon occurrence of an event (e.g., life insurance)

Not based on actual financial loss

Aleatory Contracts

Performance depends on uncertain events

Unequal exchange of values between parties

Adhesion Contracts

Standard form contracts offered on a "take it or leave it" basis

Often subject to strict interpretation against the insurer

Personal vs. Commercial Insurance

Personal: Covers individuals and families (e.g., home, auto insurance)

Commercial: Protects businesses and organizations (e.g., property, liability, workers' compensation)

Understanding these fundamental concepts provides a solid foundation for exploring more complex legal issues in insurance. As we delve deeper into specific topics, keep these principles in mind, as they often play a crucial role in resolving disputes and interpreting insurance contracts across various jurisdictions.

International Insurance Programs

Global insurance programs are essential for multinational corporations operating across various jurisdictions. These programs aim to provide consistent coverage and centralized risk management. Key aspects include:

- Coordinating coverage across multiple countries, balancing local requirements with global consistency

- Navigating complex compliance issues related to local insurance regulations and tax requirements

- Implementing effective claims handling procedures that work across different legal systems

- Utilizing master policies and local policies to create a cohesive global program

- The role of captive insurance companies in managing global risks and optimizing tax efficiency

Challenges in this area include ensuring regulatory compliance in each jurisdiction, managing currency fluctuations, and addressing coverage gaps or overlaps between local and global policies.

Reinsurance and Its Legal Implications

Reinsurance plays a crucial role in the global insurance market by allowing insurers to spread risk and increase their capacity.

Key legal considerations include:

- The principle of utmost good faith in reinsurance contracts

- The follow-the-fortunes doctrine and its limitations

- Cut-through provisions and their impact on policyholder rights

- Dispute resolution mechanisms specific to reinsurance, such as expert determination

- The effect of insolvency on reinsurance recoveries

Reinsurance disputes often center around contract interpretation, claims documentation, and the scope of coverage. The complex nature of these arrangements can lead to protracted legal battles, highlighting the importance of clear contract drafting and effective communication between cedents and reinsurers.

Insurance in Mergers and Acquisitions

Insurance plays an increasingly important role in M&A transactions, particularly through specialized products like representations and warranties (R&W) insurance.

Key considerations include:

- The use of R&W insurance to facilitate deals by transferring certain transaction risks

- Due diligence on target companies' insurance programs, including adequacy of coverage and claims history

- Strategies for transferring or novating insurance policies in asset sales

- Post-acquisition challenges in integrating and optimizing insurance programs

- The impact of change-in-control provisions on existing insurance arrangements

As M&A activity continues to grow globally, understanding these insurance-related aspects becomes crucial for both buyers and sellers in corporate transactions.

Regulatory Compliance and Reporting

Insurance companies face an increasingly complex regulatory landscape, with requirements varying significantly across jurisdictions.

Key aspects include:

- Solvency requirements and capital adequacy reporting (e.g., Solvency II in the EU, Risk-Based Capital in the US)

- Market conduct regulations and consumer protection measures

- Anti-money laundering (AML) and know-your-customer (KYC) requirements

- The role of appointed actuaries in certifying financial statements and regulatory reports

- Emerging focus areas such as operational resilience and climate risk disclosure

Compliance challenges are exacerbated by the rapid pace of regulatory change and the need to adapt to new technologies and emerging risks.

Insurance and Human Rights

The intersection of insurance practices and human rights is an emerging area of focus, encompassing:

- Non-discrimination in underwriting and pricing, particularly in personal lines of insurance

- The role of insurance in promoting access to healthcare and financial inclusion

- Consideration of human rights impacts in corporate insurance programs

- The insurance industry's potential contribution to sustainable development goals

- Ethical considerations in the use of genetic information and AI in insurance decisions

As social responsibility becomes increasingly important to stakeholders, insurers must navigate the balance between risk-based pricing and broader societal concerns.

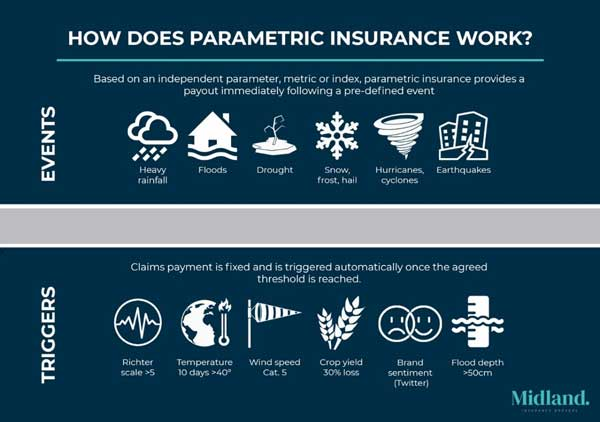

Parametric Insurance and Legal Considerations

Parametric insurance, which pays out based on predefined triggers rather than actual losses, is gaining traction in various markets.

Legal considerations include:

- Regulatory classification of parametric products (insurance vs. derivatives)

- Basis risk and its implications for contract enforceability

- The use of parametric insurance to address protection gaps in developing markets

- Legal challenges in designing triggers that accurately reflect the intended risk transfer

- Potential for parametric solutions in addressing systemic risks like pandemics

As parametric insurance evolves, legal frameworks will need to adapt to ensure appropriate consumer protection while allowing for innovation.

Digital Claims Processing and Legal Implications

The digitalization of claims processing introduces new legal and ethical considerations:

- The use of AI and machine learning in claims adjudication and fraud detection

- Ensuring transparency and explainability in automated decision-making processes

- Data privacy and security concerns in the collection and processing of claims data

- The admissibility and weight of digital evidence in insurance disputes

- Potential biases in AI-driven claims processes and strategies for mitigation

As technology continues to transform claims handling, insurers must balance efficiency gains with legal and ethical obligations to policyholders.

Insurance Fraud: Detection and Legal Responses

Insurance fraud remains a significant challenge for the industry, with legal and technological responses evolving:

- The use of data analytics and AI to detect patterns indicative of fraud

- Legal considerations in sharing fraud-related information among insurers

- The role of specialized insurance fraud units within law enforcement agencies

- International cooperation in combating cross-border insurance fraud schemes

- Balancing aggressive fraud prevention with the duty of good faith in claims handling

Effective fraud prevention requires a multi-faceted approach, combining technological solutions with legal deterrents and industry cooperation.

Insurance Regulation: A Global Overview

Insurance regulation varies significantly across the globe, but there are common themes and emerging trends. This section provides a comparative analysis of regulatory frameworks in key regions.

Insurance Regulation by Region:

United States:

Key Regulatory Bodies: State Insurance Commissioners, National Association of Insurance Commissioners (NAIC)

Primary Focus: Consumer protection, solvency

Notable Features: State-based regulation with federal oversight

European Union:

Key Regulatory Bodies: European Insurance and Occupational Pensions Authority (EIOPA), National Competent Authorities

Primary Focus: Harmonization, consumer protection

Notable Features: Solvency II framework, single market

Asia:

Key Regulatory Bodies: Varies by country (e.g., China Banking and Insurance Regulatory Commission (CBIRC) in China, Insurance Regulatory and Development Authority of India (IRDAI) in India)

Primary Focus: Market development, stability

Notable Features: Rapid regulatory evolution, increasing sophistication

Emerging Trends in Insurance Regulation:

- Increased focus on cybersecurity and data protection

- Integration of climate risk into regulatory frameworks

- Adoption of risk-based capital requirements

- Enhanced reporting and transparency requirements

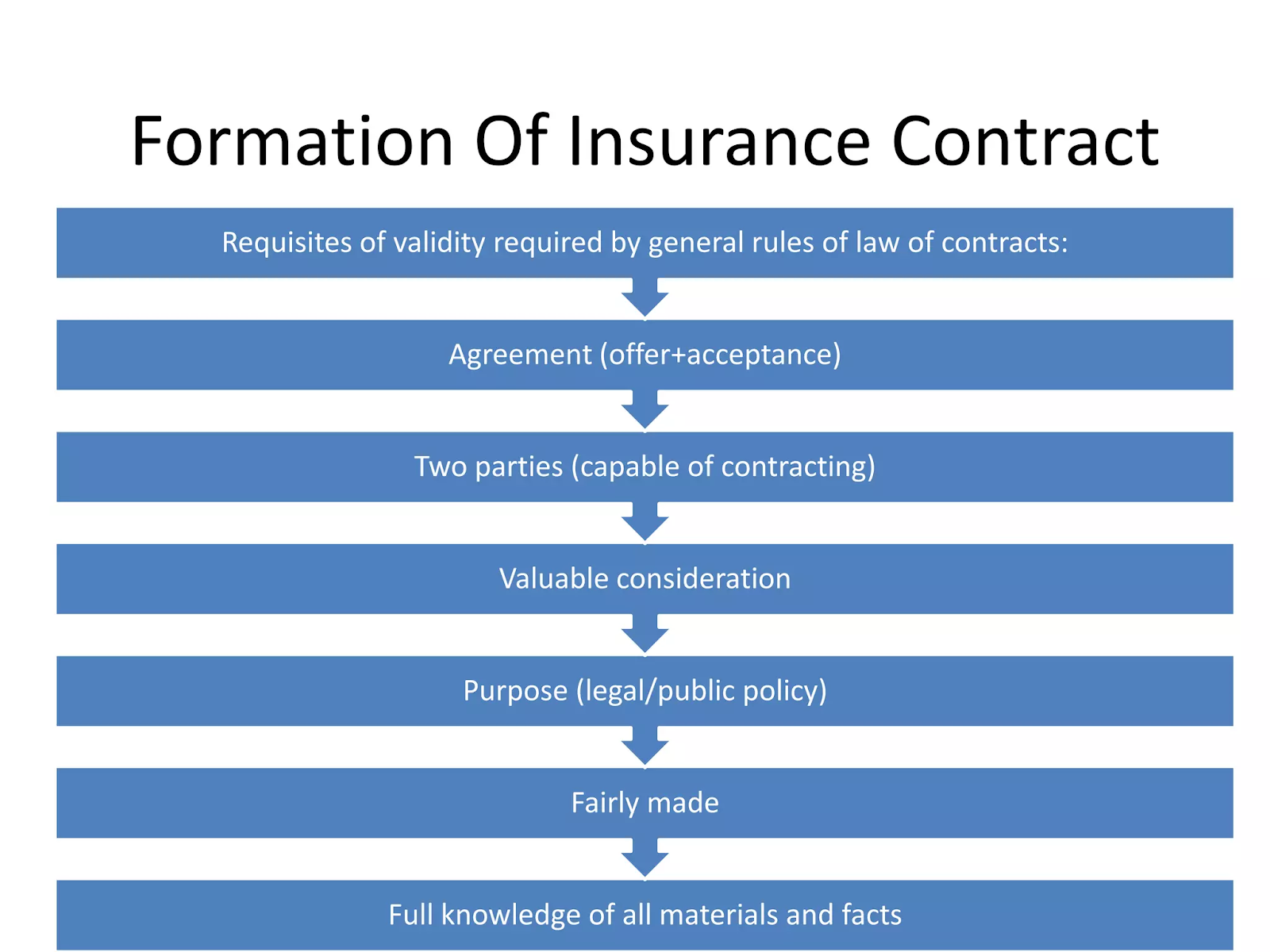

The Insurance Contract: Legal Considerations

The formation and interpretation of insurance contracts are crucial aspects of insurance law. Here's a flowchart illustrating the typical contract formation process:

Key Legal Considerations:

- Policy interpretation: Courts generally interpret ambiguities in favor of the policyholder (contra proferentem rule)

- Duty of disclosure: Policyholders must disclose material facts affecting the risk

- Warranties and conditions: Strict compliance often required for coverage

Common Clauses and Their Legal Implications:

- Exclusion clauses: Limit the scope of coverage

- Choice of law and jurisdiction clauses: Determine applicable law and forum for disputes

- Subrogation clauses: Allow insurers to pursue third parties responsible for losses

Coverage Issues and Disputes

Case Study: Business Interruption Insurance During the COVID-19 Pandemic

Background: Many businesses faced significant losses due to government-mandated closures during the pandemic.

Issue: Does business interruption insurance cover losses stemming from pandemic-related closures?

Analysis:

1. Policy wording: Many policies require "physical loss or damage" to property

2. Causation: Direct vs. indirect causes of business interruption

3. Exclusions: Some policies contain virus or pandemic exclusions

Global Perspectives:

- UK: FCA test case resulted in some coverage for certain policy wordings

- US: Majority of courts ruled in favor of insurers, citing lack of physical damage

- Australia: Some policies found to provide coverage due to specific wording

Key Takeaways:

- Importance of careful policy drafting and review

- Potential for legislative intervention in future pandemics

- Need for specialized pandemic insurance products

The Claims Process: Legal Perspectives

Step-by-Step Guide with Legal Considerations:

1. Notification of Loss

Legal consideration: Timely notice is crucial; late notice may result in claim denial

2. Proof of Loss

Legal consideration: Burden of proof typically on the policyholder

3. Investigation and Adjustment

Legal consideration: Insurer's duty to investigate in good faith

4. Coverage Determination

Legal consideration: Interpretation of policy language and applicable law

5. Valuation of Loss

Legal consideration: Methods of valuation specified in the policy

6. Settlement Negotiation

Legal consideration: Duty to settle within policy limits when appropriate

7. Payment or Denial

Legal consideration: Timely payment required; wrongful denial may lead to bad faith claims

8. Dispute Resolution (if necessary)

Legal consideration: Choice of forum (litigation, arbitration, or mediation)

Bad Faith and Unfair Claims Practices

Q: What constitutes bad faith in insurance?

A: Bad faith occurs when an insurer unreasonably denies, delays, or underpays a claim without proper justification.

Q: What are common examples of bad faith?

A: Examples include:

- Failing to properly investigate a claim

- Misrepresenting policy provisions

- Unreasonably delaying payment

- Making lowball settlement offers

Q: What statutory regulations exist against unfair practices?

A: Many jurisdictions have enacted Unfair Claims Settlement Practices Acts, which prohibit specific unfair behaviors by insurers.

Q: What remedies are available for bad faith?

A: Remedies may include:

- Compensatory damages beyond policy limits

- Punitive damages in egregious cases

- Attorney's fees and costs

- Statutory penalties

Q: How does bad faith vary globally?

A: The concept of bad faith is most developed in the United States. Other jurisdictions may address similar issues through different legal frameworks, such as breach of contract or consumer protection laws.

Alternative Dispute Resolution in Insurance

Mediation and Arbitration in Insurance Disputes

Pros:

- Potentially faster and less expensive than litigation

- Confidentiality of proceedings

- Flexibility in process and outcome

- Ability to choose decision-makers with industry expertise

Cons:

- Limited appeal rights in arbitration

- Potential for bias in industry-specific arbitration forums

- Less formal procedures may limit discovery

- Precedential value of decisions may be limited

International Considerations:

- New York Convention facilitates enforcement of international arbitration awards

- Choice of law and seat of arbitration crucial in cross-border disputes

- Cultural differences may impact mediation effectiveness

Emerging Issues in Insurance Law

Cybersecurity and Data Protection:

• Increasing demand for cyber insurance

• Challenges in quantifying cyber risks

• Regulatory compliance (e.g., GDPR, CCPA) affecting coverage and claims

Climate Change and Natural Disasters:

• Evolving risk models for catastrophic events

• Potential for uninsurable risks due to climate change

• Regulatory pressure for climate risk disclosure

Insurtech and Digital Transformation:

• Legal implications of AI in underwriting and claims processing

• Smart contracts and blockchain in insurance

• Regulatory challenges in adapting to new technologies

Best Practices for Insurers and Policyholders

Checklist for Risk Management and Policy Administration:

For Insurers:

- Implement robust underwriting guidelines

- Regularly review and update policy language

- Maintain comprehensive claims handling procedures

- Provide ongoing training on regulatory compliance

- Implement strong data protection and cybersecurity measures

- Develop clear communication protocols with policyholders

- Establish internal audit processes for claims handling

For Policyholders:

- Conduct thorough risk assessments

- Review policies annually and update as needed

- Maintain accurate records of assets and potential liabilities

- Promptly report any changes that may affect coverage

- Familiarize yourself with policy terms, conditions, and exclusions

- Document all communication with insurers

- Seek professional advice for complex insurance needs

Documentation Best Practices:

- Maintain detailed inventory of insured assets

- Keep records of all policy documents and correspondence

- Document incidents thoroughly when they occur

- Retain expert reports and valuations

- Preserve evidence related to potential claims

Understanding Legal Issues in Insurance

As we've explored in this comprehensive guide, the legal landscape of insurance is complex and ever-evolving. From the fundamental principles that underpin insurance law to the emerging challenges posed by technological advancements and global risks, both insurers and policyholders must navigate a myriad of legal considerations.

Key takeaways include:

- The importance of understanding basic insurance principles and contract formation

- The varied regulatory environments across different jurisdictions

- The critical role of policy wording in determining coverage

- The need for fair and efficient claims handling processes

- The potential for alternative dispute resolution in insurance conflicts

- The emerging challenges posed by cybersecurity, climate change, and insurtech

Looking to the future, we can expect continued evolution in insurance law as it adapts to new risks, technologies, and global challenges. Insurers will need to balance innovation with regulatory compliance, while policyholders must remain vigilant in understanding and managing their insurance needs.

Ultimately, effective risk management and clear communication between all parties are essential for navigating the complex world of insurance law. By staying informed about legal developments and adhering to best practices, both insurers and policyholders can better protect their interests and ensure the continued effectiveness of insurance as a vital risk transfer mechanism in our global economy.