Thailand's dynamic economic landscape and strategic position in Southeast Asia make it a desirable place for business. However, understanding the corporate taxation structure is critical for businesses operating in Thailand. This legal guide gives a complete overview of corporate taxation in Thailand, including the many types of taxes that apply to firms, tax incentives, compliance requirements, and best practices for efficiently managing tax liabilities.

Corporate Taxes in Thailand

Corporate Income Tax (CIT)

Corporate Income Tax is the major tax charged on Thailand-based firms' earnings. The Revenue Department oversees CIT, which applies to both resident and non-resident businesses. Key features of CIT include:

Tax Rates: The normal CIT rate for most businesses is 20%. Small and medium-sized enterprises (SMEs) and corporations listed on Thailand's Stock Exchange (SET) are subject to special rates.

Taxable Income: This refers to all gains obtained from company activities, investments, and other sources of income. Deductions for company costs, depreciation, and losses are permitted under certain circumstances.

Tax Year: In Thailand, the tax year is based on the calendar year, however, corporations can request clearance from the Revenue Department to use a different fiscal year.

Filing and Payment: Companies must submit an annual tax return (Form CIT 50) within 150 days of the end of their accounting period. In addition, mid-year tax returns (Form CIT 51) must be filed two months after the first six months of the accounting year, with advance tax payments based on expected earnings.

Withholding Tax (WHT)

Withholding tax is deducted at the source on certain types of payments made by businesses. Key points include:

WHT applies to a variety of payments, such as dividends, interest, royalties, service fees, and rental income.

WHT rates vary based on the payment method and the recipient's tax status. For example, profits given to resident corporations are subject to a 10% WHT rate, although non-resident companies may incur higher rates unless a tax treaty reduces them.

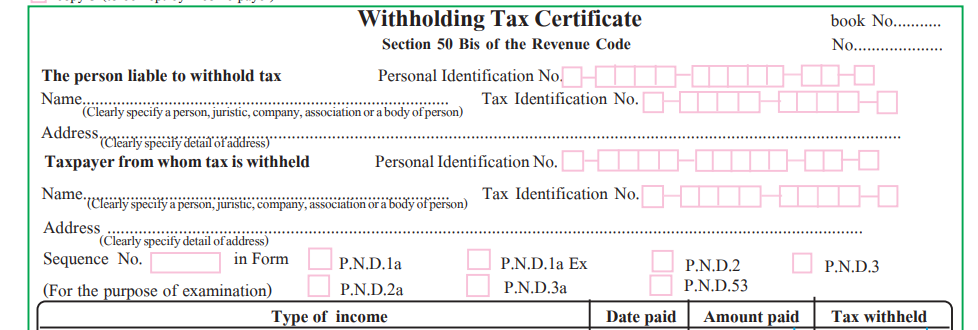

Reporting and Remittance: Businesses must withhold taxes at the time of payment and transmit them to the Revenue Department by the seventh of the following month. A WHT certificate must be provided to the receiver as proof of tax deduction.

Value-Added Tax (VAT)

Thailand levies a consumption tax on the sale of goods and services known as value-added tax (VAT). Important components of VAT include:

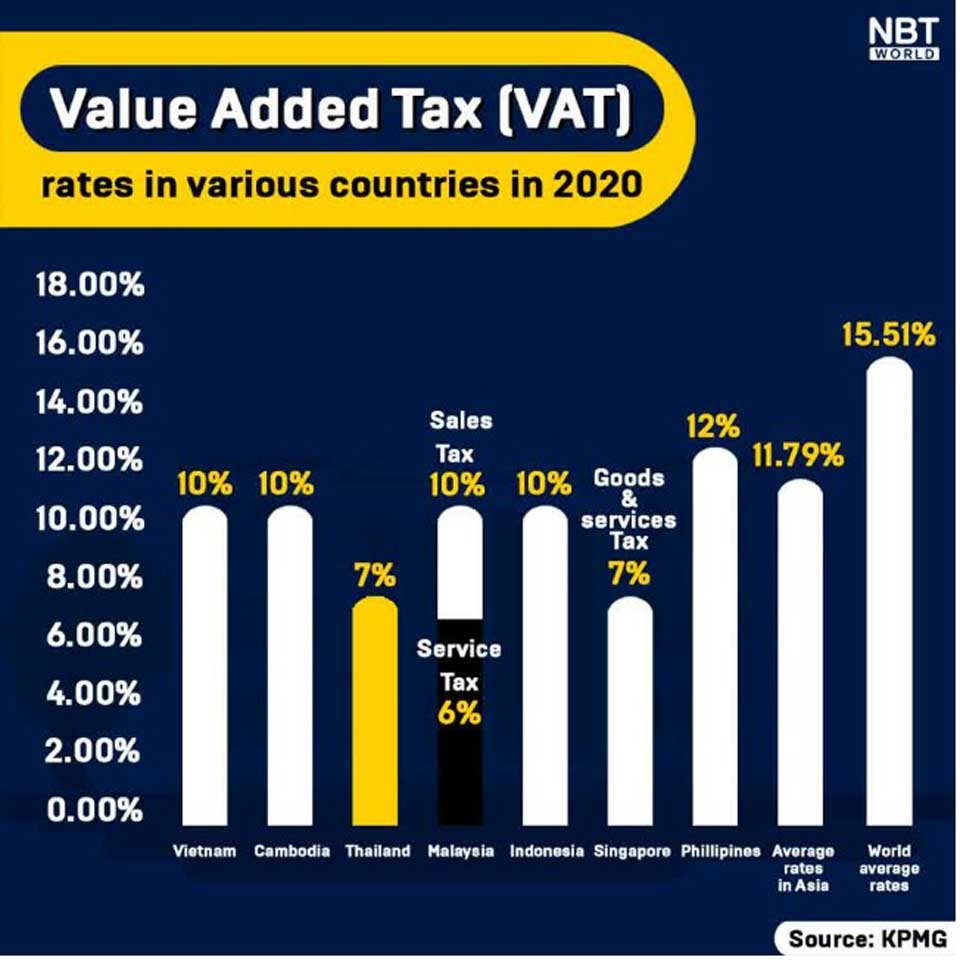

VAT Rates: The usual rate is 7%. Certain products and services, such as exports and necessities, are exempt or have a zero tax rate.

Registration Requirements: Businesses with yearly revenues of more than THB 1.8 million must register for VAT. Small firms can also register voluntarily.

Filing and Payment: VAT returns (Form VAT 30) must be submitted monthly by the 15th of the following month. VAT payments are done at the same time as the filing.

Specific Business Tax (SBT)

Specific Business Tax applies to businesses that are not subject to VAT, such as banking, finance, and real estate. Key points include:

SBT Rates: The rates vary according to the type of company activity. Banking and financial companies, for example, bear a 3% SBT rate on gross receipts, whereas real estate transactions are taxed at 0.11%.

Filing and Payment: SBT returns (Form SBT 40) must be filed monthly by the 15th of the following month, with tax payments made concurrently.

Tax Incentives and Exemptions

Board of Investment Incentives

The Board of Investment offers a variety of tax breaks to encourage investment in Thailand. The main motivations include:

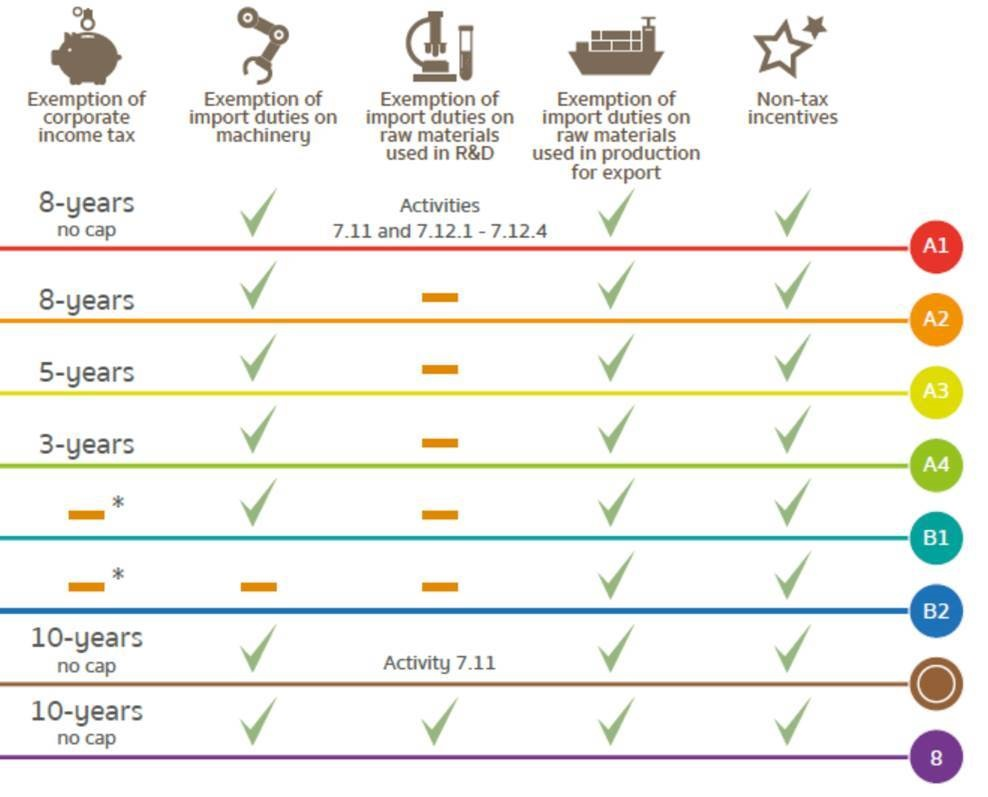

Tax Holidays: CIT exemption for 3 to 8 years, depending on the nature and location of the investment.

Reduced CIT Rates: CIT Rates are reduced for particular sectors or locations.

Exemption from Import Tariffs: Machinery, raw materials, and production-related goods are exempt from import tariffs.

Additional Deductions: Increased deductions for R&D, training, and infrastructure development.

Incentives for International Headquarters (IHQ) and International Trading Centers (ITCs)

Thailand provides tax breaks for businesses establishing International Headquarters or International Trading Centers. This includes:

Reduced CIT Rates: CIT rates have been reduced for eligible revenue such as service fees, royalties, and dividends received from linked firms.

Exemption from WHT: WHT exemption applies to dividends paid to foreign shareholders as well as interest on borrowing from foreign corporations.

Personal Income Tax (PIT) Incentives: Lower PIT rates for expatriates working in IHQs or ITCs.

Regional Operating Headquarters (ROH) Incentive

ROH incentives are offered for corporations who manage regional operations from Thailand. Key advantages include:

Reduced CIT Rates: CIT rates have been reduced for eligible revenue, such as service fees and royalties received from linked firms.

WHT exemption: Dividends given to overseas shareholders are not subject to WHT.

PIT Incentives: Lower PIT rates for expats working in ROHs.

Compliance Requirements and Reporting

Corporate Income Tax Compliance

Annual Tax Return (Form CIT 50): Businesses must submit an annual tax return within 150 days of the end of their accounting period. The return must include financial statements, tax computations, and supporting documentation.

Mid-Year Tax Return (Form CIT 51): Businesses must file a mid-year tax return within two months of the first six months of their fiscal year. This report contains expected earnings and advance tax payments.

The Revenue Department performs tax audits to ensure compliance with CIT laws. Companies must keep correct records and supporting paperwork to back up their tax filings.

Withholding Tax Compliance

WHT Remittance: Businesses must withhold tax at the source and submit it to the Revenue Department by the seventh of the following month. A WHT certificate must be provided to the receiver as proof of tax deduction.

WHT Returns: The Revenue Department must receive monthly WHT returns (Forms PND 1, 2, and 3), which describe the withheld tax and payments paid.

Value-Added Tax Compliance

VAT Registration: Businesses with an annual income of more than THB 1.8 million must register for VAT. VAT registration applications (Form VAT 01) must be filed to the Revenue Department.

VAT Returns: Monthly VAT returns (Form VAT 30) must be submitted by the 15th of the following month. The return provides information about VAT collected on sales and VAT paid on purchases.

VAT Invoices: Businesses must provide VAT invoices for all taxable transactions, which include the VAT amount and registration number.

Specific Business Tax Compliance

SBT Registration: Businesses subject to SBT are required to register with the Revenue Department. An application for SBT registration (Form SBT 01) must be filed.

SBT Returns: Monthly SBT returns (Form SBT 40) must be submitted by the 15th of the following month, documenting gross revenues and tax payments.

Best Practices for Managing Corporate Taxes

Tax Planning and Optimization

Effective tax planning and optimization tactics can help a firm drastically lower its tax burden. Key tactics include:

Utilizing Tax Incentives: Take use of applicable tax breaks, such as BOI promotions, IHQ/ITC incentives, and ROH advantages.

Transfer Pricing Compliance: Follow transfer pricing requirements to avoid fines and double taxes. Proper paperwork and arm's-length pricing are required.

Loss Utilization: Use tax loss carryforwards to offset future taxable earnings. Understand the rules and constraints of carrying forward losses.

Accurate Record-Keeping and Documentation

Maintaining proper records and documentation is critical for tax compliance and auditing purposes. Best practices include:

Maintain comprehensive records of all financial transactions, such as invoices, receipts, contracts, and bank statements.

Ensure that all tax deductions, credits, and exemptions are properly documented. Maintain supporting documentation for at least five years.

Use electronic filing solutions for tax returns and documents to speed up the compliance process and limit the possibility of mistakes.

Regular Tax Audits and Reviews

Regular tax audits and reviews can help uncover possible difficulties and assure compliance with tax legislation. Best practices include:

Internal Audits: Conduct frequent internal audits to check tax filings, detect inconsistencies, and assure regulatory compliance.

External Reviews: Hire independent tax consultants or auditors to analyze tax returns and offer professional advice on compliance and optimization.

Risk Management: Use risk management measures to address possible tax risks, such as making proper reserves for tax payments and staying up to date on regulatory changes.

Staying Informed and Updated

Tax rules and practices are subject to change. Staying educated and updated is critical for long-term compliance. Best practices include:

Monitoring Regulatory Changes: Keep track of changes in tax laws, rules, and policies via official publications, industry groups, and professional networks.

Continuous Education: Attend tax seminars, workshops, and training programs to keep up with the newest advances in business taxation.

Professional Advice and Support

Tax lawyers in Thailand and legal specialists may help assure compliance with changing legislation and provide assistance on complicated tax issues.

Case Study: Effective Corporate Tax Management in Thailand

Background

ABC Manufacturing Co., Ltd., a global organization with operations in Thailand, wanted to reduce its tax liabilities while growing its business. The corporation struggled to comprehend the complicated tax legislation and ensure compliance with Thailand's many sorts of corporate taxes.

Tax Planning and Optimization

ABC Manufacturing hired a team of tax consultants to perform a thorough analysis of its tax situation. The consultants discovered chances to take advantage of tax breaks granted by the Board of Investment (BOI) for the company's new manufacturing plant. The firm qualified for a tax break, import duty exemptions on machinery, and increased deductions for R&D costs.

Transfer Pricing Compliance

Given ABC Manufacturing's worldwide character, transfer pricing compliance was important. The tax advisers supported the corporation in developing transfer pricing rules that followed the arm's length principle. Proper paperwork was developed to support the transfer pricing arrangements, reducing the possibility of fines and disputes with tax authorities.

Accurate Record-Keeping and Documentation

ABC Manufacturing has a strong document management system to ensure proper record-keeping. The system allowed the organization to keep detailed records of all financial transactions, such as VAT invoices, WHT certificates, and contracts. The corporation also switched to electronic filing methods for tax returns, which reduced the possibility of mistakes and increased compliance efficiency.

Regular Tax Audits and Reviews

ABC Manufacturing conducted internal tax audits on a regular basis to detect possible concerns and assure continued compliance. External tax advisers were hired to analyze the company's tax filings and give professional guidance on compliance and optimization. This proactive strategy enabled the organization to rectify anomalies and apply best practices in tax management.

Staying Informed and Updated

ABC Manufacturing realized the necessity of remaining current on regulatory changes. The organization attended tax seminars and workshops and signed up for updates from industry groups and professional networks. This continual education meant that the corporation was informed of the most recent advances in corporate taxation and could adjust its plans accordingly.

Outcome

ABC Manufacturing effectively managed its Thai corporate tax requirements by using efficient tax planning and optimization techniques, guaranteeing transfer pricing compliance, keeping accurate records, performing frequent audits, and remaining informed. The company utilized tax advantages, reduced tax liabilities, and complied with Thai tax legislation, all of which contributed to its overall economic success.

Staying On Top of Corporate Taxation in Thailand

Understanding and managing corporate taxation in Thailand is critical for firms operating within the nation. The complicated regulatory system, which includes Corporate Income Tax, Withholding Tax, Value Added Tax, and Specific Business Tax, necessitates strict compliance and strategic tax planning. Companies may maximize their tax liabilities and comply with Thai tax regulations by exploiting relevant tax benefits, maintaining correct record-keeping, performing frequent audits, and remaining up to date on regulatory changes.

Staying up to date on the latest developments, offering competent tax compliance advice, and aiding with tax planning strategies are all critical for Thai attorneys advising clients on corporate taxes. As the tax environment evolves, continuing education and proactive contact with tax authorities will be critical in managing Thailand's business tax difficulties.