- Registering a Cyprus financial holding company takes one to two weeks and requires filing with the Department of Registrar of Companies and Intellectual Property.

- To secure Cyprus tax residency, the company must pass the "Management and Control" test by keeping its core decision-making and majority board representation local.

- Upcoming EU directives targeting shell companies require Cyprus holding entities to demonstrate genuine economic substance, such as local premises, active bank accounts, and qualified resident directors.

- Structuring operations correctly allows companies to benefit from a 12.5% corporate tax rate, an IP Box regime lowering effective tax to 2.5%, and full tax exemptions on most incoming international dividends.

Step-by-Step Requirements to Register a Cyprus Private Limited Company

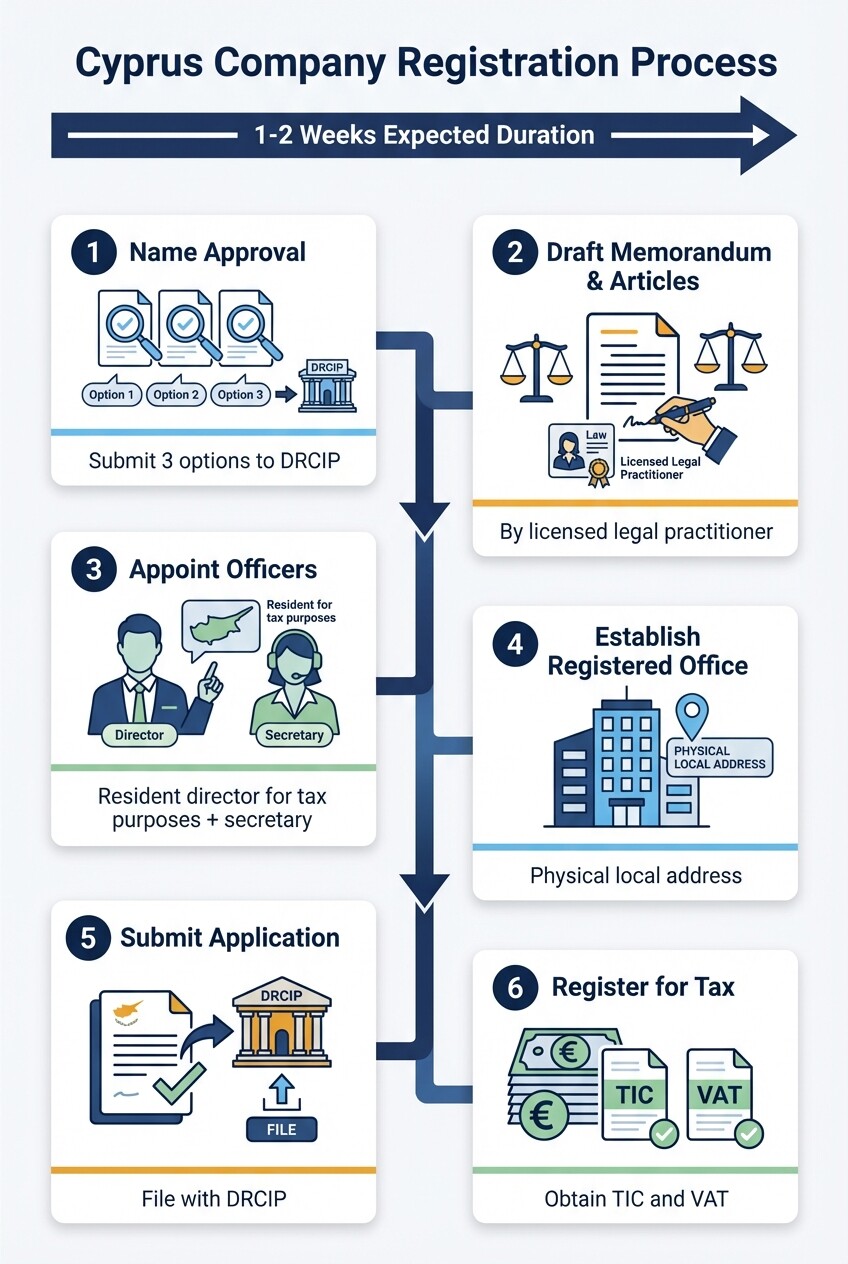

Registering a private limited liability company (LTD) in Cyprus involves securing a unique name, preparing corporate documents, and submitting formal applications to the government. The standard process takes one to two weeks and typically costs between €1,500 and €3,000 in government and professional fees.

The essential steps for incorporation include:

- Name Approval: Submit your proposed company name to the Department of Registrar of Companies and Intellectual Property (DRCIP). You should submit three alternatives to avoid delays if your first choice is rejected for similarity to existing entities.

- Draft the Memorandum and Articles of Association: These constitutional documents must be drafted by a licensed legal practitioner in Cyprus. They define the company activities, shareholder rights, and internal governance rules.

- Appoint Company Officers: You must appoint at least one director and one company secretary. While directors can be non-residents, appointing resident directors is necessary to establish local tax residency.

- Establish a Registered Office: The company must maintain a physical registered address in Cyprus where statutory records are kept and legal notices are served.

- Submit the Application: File the constitutional documents, officer details, registered address, and a statutory declaration by your legal representative to the DRCIP.

- Register for Tax and Social Insurance: Once incorporated, the company must register with the Cyprus Tax Department for a Tax Identification Code (TIC) and VAT (if applicable), followed by the Ministry of Labour if hiring local employees.

Demonstrating Economic Substance for 2026 EU Compliance

To comply with the impending EU Unshell Directive (often referred to as ATAD 3) targeting shell entities, a Cyprus holding company must prove it conducts genuine economic activity and is not merely a paper vehicle. Failure to meet these substance requirements can result in the denial of tax treaty benefits and financial penalties.

Cyprus holding companies must establish clear local substance through the following measures:

- Dedicated Premises: The company must own or secure exclusive use of physical office space in Cyprus. Shared virtual offices or simple mailing addresses no longer meet the threshold for economic substance.

- Active Local Bank Account: The entity must maintain an active corporate bank account within the European Union, preferably in Cyprus, through which its primary operational and holding income flows.

- Local Decision Making: Board meetings must physically take place in Cyprus. Strategic decisions regarding the holding company assets must be documented in minutes recorded locally.

- Qualified Personnel: The company must employ adequate local staff or directors who possess the actual authority and professional qualifications to manage the company assets independently.

Structuring for IP Box Regime and Dividend Tax Exemptions

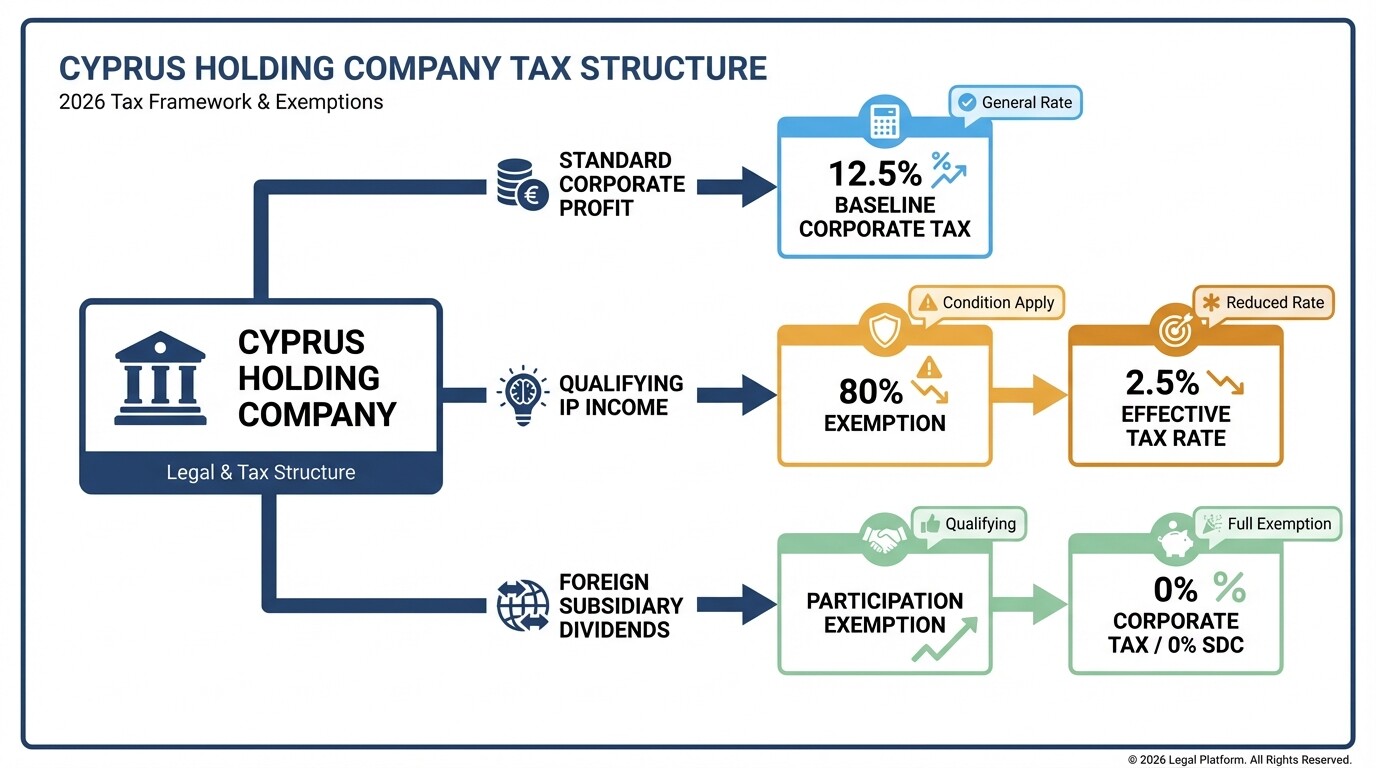

Cyprus offers a highly favorable corporate tax environment, highlighted by a baseline 12.5% corporate tax rate, an advantageous Intellectual Property (IP) Box regime, and participation exemptions on dividends. Structuring your holding company to isolate intellectual property assets and equity holdings can significantly reduce your global tax burden.

Under the Cyprus IP Box regime, 80% of qualifying profits generated from the exploitation of qualifying intellectual property (such as software copyrights and patents) are exempt from corporate tax. This effectively reduces the tax rate on IP income to 2.5%. To qualify, the holding company must demonstrate a clear link between the research and development expenses incurred to create the IP and the income it generates.

For dividend income, Cyprus applies a participation exemption. Dividends received by a Cyprus holding company from foreign subsidiaries are entirely exempt from corporate income tax and the Special Contribution for Defense (SDC). This exemption applies provided the foreign subsidiary does not engage in activities that produce more than 50% investment income, or the foreign tax burden on the subsidiary is not significantly lower than the Cyprus tax rate.

Corporate Governance and Fiduciary Duties for Non-Residents

Corporate governance in Cyprus mandates that directors act in the best interest of the company, maintain accurate financial records, and avoid conflicts of interest. While foreign investors can serve as directors, appointing non-resident directors compromises the ability of the company to claim Cyprus tax residency.

The core principle governing tax residency in Cyprus is the "Management and Control" test. The tax authorities look at where the strategic decisions of the company are actually made. If a holding company is fully directed by non-residents making decisions from abroad, the entity may be deemed a tax resident of that foreign jurisdiction instead.

To satisfy fiduciary and tax requirements, foreign investors typically structure their boards with a majority of qualified Cyprus resident directors. These resident directors must not be mere nominees; they must actively review financial statements, approve transactions, and hold documented board meetings within Cyprus to fulfill their fiduciary duties legally.

Domiciliation and Redomiciliation Alternatives in the Mediterranean

Cyprus allows foreign companies to transfer their legal seat into the country without liquidating their existing corporate structure, a process known as redomiciliation. While Cyprus is a primary choice, investors often compare it to other Mediterranean jurisdictions like Malta and Gibraltar for holding company structures.

Cyprus is often favored for its straightforward 12.5% flat corporate tax and extensive network of double tax treaties. The redomiciliation process requires the foreign company to be in good standing, have authorization in its current constitutional documents to move, and file a comprehensive application with the Cyprus Registrar of Companies.

Alternatively, Malta offers a full imputation tax system. While Malta has a higher nominal corporate tax rate of 35%, shareholders can claim refunds that reduce the effective rate to between 5% and 10%. Gibraltar, outside the EU customs union but highly regulated, appeals to specific finance and gaming sectors. However, Cyprus remains the preferred Mediterranean hub for general EU financial holding structures due to its alignment with EU directives and predictable corporate legal framework modeled on English common law.

Common Misconceptions About Cyprus Holding Companies

Many foreign investors hold outdated or inaccurate beliefs regarding the regulatory environment in Cyprus, leading to structural errors during incorporation.

- A registered address guarantees tax residency: Simply paying for a registered office address does not make a company a Cyprus tax resident. The company must prove actual management and control occurs within the country.

- Cyprus is an unregulated offshore tax haven: Cyprus is a fully compliant European Union member state and adheres strictly to OECD transparency standards, Anti-Money Laundering (AML) directives, and global Common Reporting Standards (CRS).

- Foreigners cannot own 100% of the shares: There are no restrictions on foreign ownership for standard private limited liability companies. Non-EU citizens can own 100% of the shares in a Cyprus holding company.

Frequently Asked Questions

What is the minimum share capital for a Cyprus private limited company?

There is no strict legal minimum share capital required for a private limited liability company in Cyprus. However, standard commercial practice is to authorize and issue a minimum share capital of €1,000, divided into 1,000 shares of €1 each.

Can I open a corporate bank account in Cyprus as a non-resident?

Yes, a Cyprus holding company with non-resident shareholders can open a local corporate bank account. However, local banks enforce strict Know Your Customer (KYC) and Anti-Money Laundering (AML) protocols, requiring detailed business plans, proof of source of funds, and in-person or verified remote interviews.

Are there withholding taxes on outgoing dividends from Cyprus?

Cyprus does not levy withholding tax on dividends paid to non-resident shareholders, regardless of whether the shareholder is a corporation or an individual, and regardless of their country of residence.

Is an annual financial audit mandatory for Cyprus holding companies?

Yes, every Cyprus company must submit audited financial statements prepared by a licensed and registered local auditor to the Tax Department and the Registrar of Companies annually.

When to Hire a Business Registration Lawyer

Structuring an EU financial holding company requires precise alignment between corporate law, international tax treaties, and economic substance regulations. You should consult a legal professional before drafting your constitutional documents or attempting to migrate an existing foreign corporate structure into the jurisdiction. A lawyer will ensure your board composition meets local tax residency tests and your operational setup satisfies the upcoming EU Unshell Directives.

To secure your corporate structure, connect with experienced business registration lawyers in Cyprus who specialize in holding companies and cross-border tax compliance.

Next Steps for Foreign Investors

- Define Your Asset Structure: Identify whether your holding company will primarily hold equity, intellectual property, or financing assets, as this dictates your optimal tax strategy.

- Determine Board Composition: Decide on the mix of resident and non-resident directors necessary to maintain control while satisfying local management and control requirements.

- Draft Substance Plans: Outline exactly how the company will maintain physical offices, local staff, and active bank accounts to comply with 2026 economic substance rules.

- Engage Local Counsel: Partner with a Cyprus-based corporate lawyer to draft the Memorandum and Articles of Association tailored to your specific international holding requirements.