Dutch Holding Company vs Direct Subsidiary: 2026 International Tax Treaties

Key Takeaways

Structuring your European operations through the Netherlands requires balancing robust tax benefits with increasingly strict compliance rules. Preparing for the 2026 regulatory landscape ensures your corporate structure remains legally protected and tax-efficient.

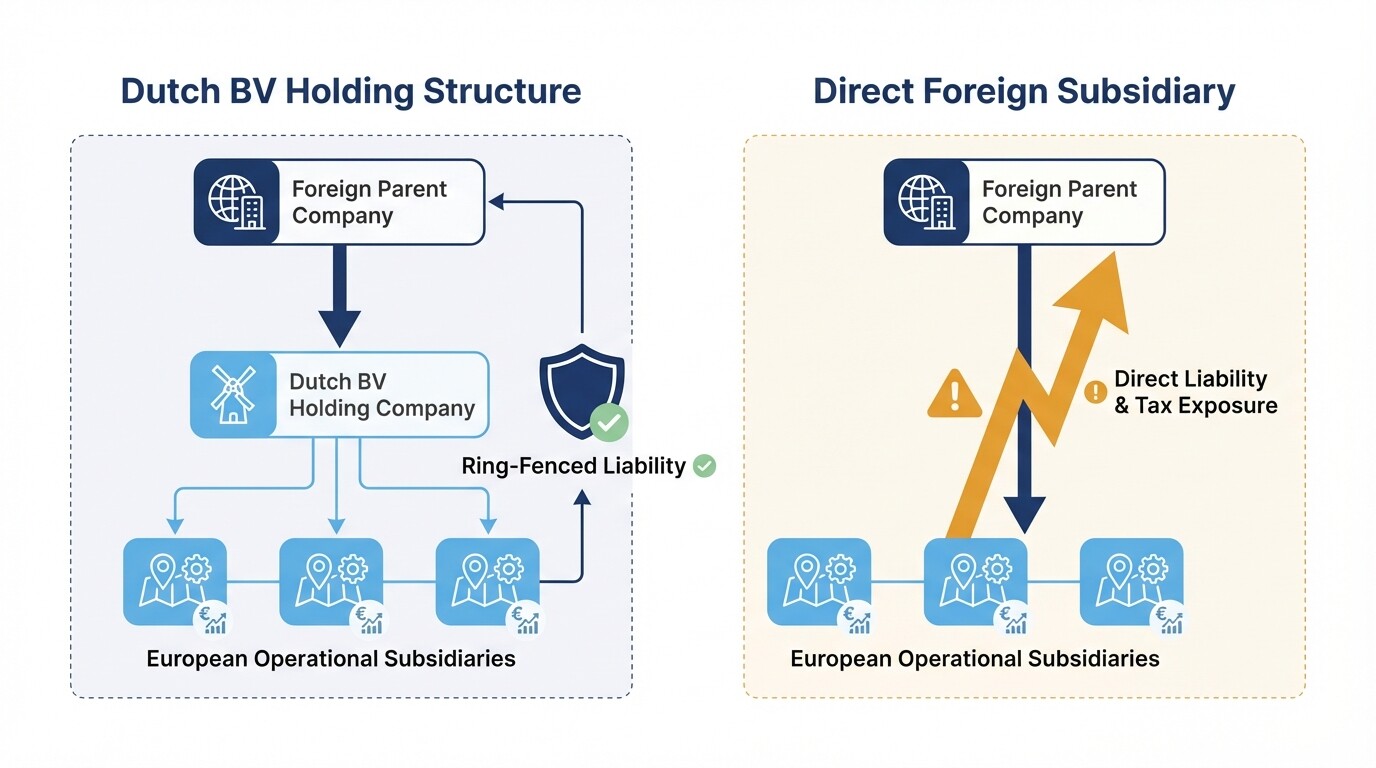

- Corporate Isolation: A Dutch BV holding company protects the parent entity from European operational liabilities, unlike a direct subsidiary structure.

- Participation Exemption: Properly structured Dutch holding companies can receive dividends and capital gains from subsidiaries 100% tax-free.

- 2026 Substance Rules: The upcoming EU ATAD 3 ("Unshell") directive mandates strict local economic nexus requirements, eliminating benefits for pure "letterbox" companies.

- UBO Compliance: Registration in the Ultimate Beneficial Owner (UBO) register is mandatory for all Dutch corporate entities, managed alongside the KVK incorporation process.

Comparing Dutch BV Holding vs Direct Subsidiary Setup

A Dutch Besloten Vennootschap (BV) holding company offers robust legal isolation and tax efficiencies under the participation exemption, whereas a direct foreign subsidiary exposes the parent directly to local operational liabilities. Choosing between these structures depends on your threshold for maintaining Dutch economic substance and your long-term European expansion strategy.

| Feature | Dutch BV Holding Company | Direct Foreign Subsidiary |

|---|---|---|

| Legal Liability | Ring-fenced. Parent company is shielded from subsidiary debts. | Direct exposure. Parent may be held liable for European operations. |

| Tax Treaty Access | Broad access to the extensive Dutch tax treaty network. | Dependent entirely on the parent company's home country treaties. |

| Capital Gains | Generally 100% tax-exempt via the participation exemption. | Subject to parent country's corporate tax rates. |

| Substance Requirements | High. Must prove local management, physical office, and local accounts. | Low to Moderate. Focus is strictly on operational compliance. |

| Setup Cost | Higher (Requires multiple entity formations and local directors). | Lower (Single entity registration). |

The Dutch Participation Exemption

The Dutch participation exemption allows a holding company to receive dividends and capital gains from qualifying subsidiaries completely free from Dutch corporate income tax. To qualify, the Dutch BV must hold at least 5% of the subsidiary's nominal paid-in capital, and the subsidiary must not be held purely as a passive portfolio investment.

2026 Regulatory Substance Requirements for Foreign Investors

Beginning in 2026, the Netherlands and the broader European Union will enforce strict "Unshell" rules (ATAD 3) that require holding companies to prove genuine operational substance to access tax treaties. Entities failing these minimum substance tests will lose treaty benefits, face punitive withholding taxes, and be subject to international information exchange penalties.

To qualify as having adequate substance, a Dutch entity must demonstrate:

- Dedicated Premises: Exclusive use of physical office space in the Netherlands (shared or virtual offices are insufficient).

- Active Bank Account: Maintenance of an active bank account within the European Union, managed from the Netherlands.

- Local Directorship: At least one qualified director residing in the Netherlands who holds the authority to make independent financial and strategic decisions.

- Local Income Generation: The majority of the entity's relevant income must be earned and managed through the local Dutch infrastructure.

Mandatory Documentation for Economic Nexus and Management Control

Tax authorities increasingly conduct anti-abuse audits to verify that management decisions genuinely occur within the Netherlands. Multinational corporations must maintain comprehensive contemporaneous documentation proving that the Dutch entity functions autonomously and is not a shell company designed solely for tax avoidance.

Auditors will demand the following documentation to prove economic nexus:

- Board Minutes: Records proving physical board meetings take place in the Netherlands, documenting core strategic and financial decisions.

- Employment Contracts: Contracts for local directors and staff, demonstrating appropriate compensation for the level of responsibility.

- Lease Agreements: Commercial lease agreements proving exclusive physical office space, alongside utility bills in the company's name.

- Local Bookkeeping: Financial ledgers, tax filings, and audit reports prepared and stored physically or digitally within the Netherlands.

Withholding Tax Documentation for Dividends, Interest, and Royalties

Cross-border distributions are subject to Dutch conditional withholding taxes unless properly documented under an applicable tax treaty or EU directive. Companies must file specific exemption or reduction forms with the Dutch Tax and Customs Administration before remitting payments to avoid default statutory tax rates.

- Dividend Withholding Tax: The statutory rate is 15%, but it can often be reduced to 0% under the EU Parent-Subsidiary Directive or a bilateral tax treaty. You must file an exemption declaration prior to distribution.

- Interest and Royalties: The Netherlands imposes a conditional withholding tax of 25.8% on interest and royalties paid to entities in low-tax jurisdictions (countries with a corporate tax rate below 9%) or non-cooperative jurisdictions.

- Advance Tax Rulings (ATR): Multinationals can apply for an ATR to gain upfront certainty from the tax authorities regarding the withholding tax treatment of specific cross-border transactions, provided local substance requirements are met.

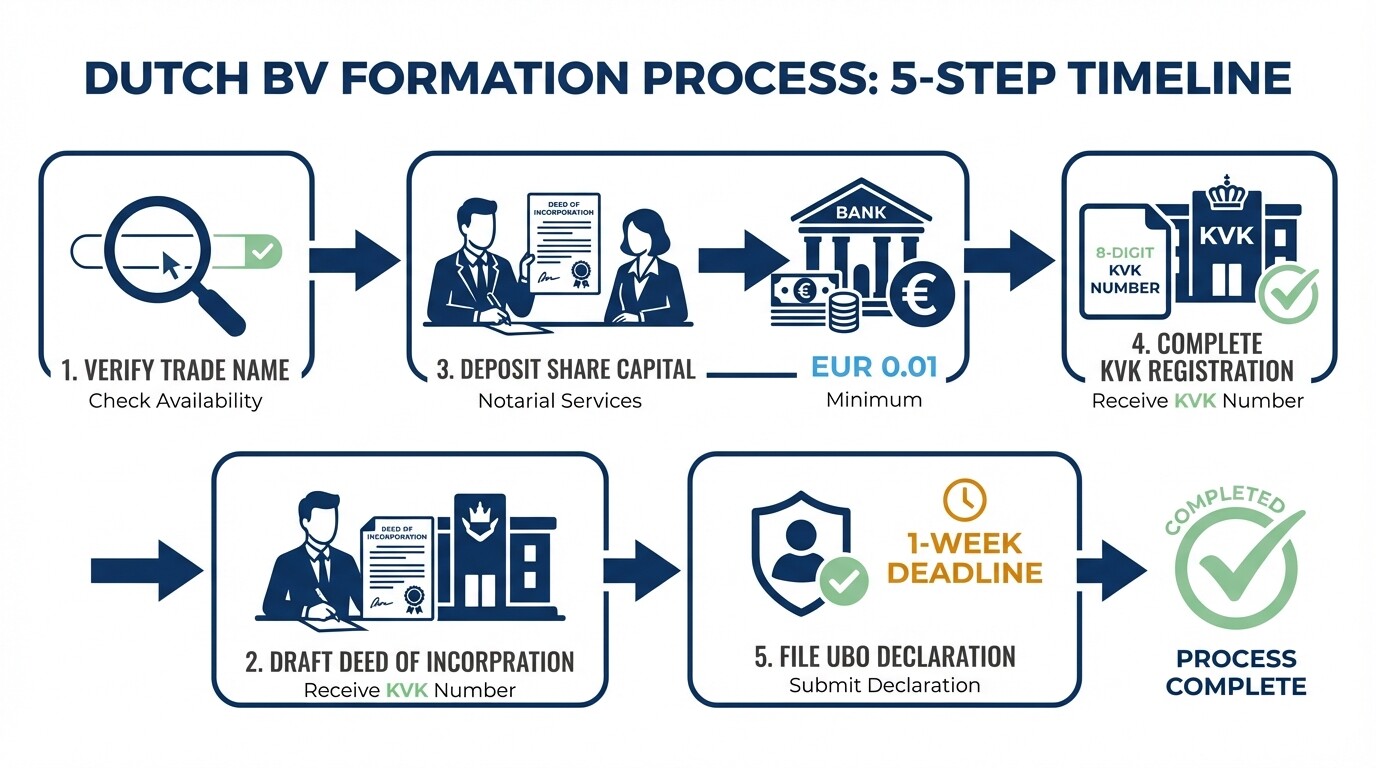

Steps to Register with the KVK and UBO Register

Incorporating a Dutch BV requires utilizing a Dutch civil-law notary who drafts the deed of incorporation and executes the official registration with the Chamber of Commerce (KVK). Simultaneously, ultimate beneficial owners must be declared in the national UBO register to comply with European anti-money laundering directives.

- Verify Trade Name: Conduct a trade name search through the KVK database to ensure your proposed corporate name is unique and does not infringe on existing trademarks.

- Draft the Deed of Incorporation: Engage a Dutch civil-law notary to draft the Articles of Association. This document outlines the company's internal regulations, share structure, and director authorities.

- Deposit Share Capital: Transfer the minimum required share capital for a BV (EUR 0.01) into a corporate bank account. While the minimum is low, adequate capitalization for operational needs is highly recommended.

- Complete KVK Registration: The notary files the finalized deed with the KVK. Upon processing, the KVK issues an 8-digit KVK number, formally establishing the entity.

- File the UBO Declaration: Within one week of incorporation, submit the details of any individual owning more than 25% of the shares or voting rights to the KVK's UBO register.

Common Misconceptions About Dutch Corporate Structuring

Foreign investors often misinterpret the complexity and cost of maintaining a compliant European holding structure. These misunderstandings routinely lead to unexpected tax liabilities and administrative penalties.

- "Virtual offices are enough for tax treaties." Merely renting a mailbox or virtual office in Amsterdam does not grant access to the Dutch tax treaty network. Tax authorities actively reject treaty claims from entities lacking physical premises and local personnel.

- "0% withholding tax is automatic." Reductions to a 0% withholding tax rate on dividends are conditional, not automatic. You must actively file the correct exemption forms and prove compliance with anti-abuse provisions before distributing funds.

- "The UBO register violates all privacy." Following a recent ruling by the European Court of Justice, the Dutch UBO register is no longer fully accessible to the general public. Access is now strictly limited to competent authorities, financial institutions conducting due diligence, and individuals demonstrating a legitimate interest.

Frequently Asked Questions

Can a foreign citizen be the sole director of a Dutch BV?

Yes, there are no nationality or residency restrictions for owning or directing a Dutch BV. However, appointing exclusively foreign, non-resident directors will severely compromise the company's ability to prove local economic substance and access tax treaties.

How long does it take to register a Dutch holding company?

Assuming all KYC (Know Your Customer) documents and apostilled corporate records are prepared, a civil-law notary can incorporate a Dutch BV and register it with the KVK in one to two weeks.

What is the corporate income tax rate for a Dutch BV?

For 2024, the Dutch corporate income tax rate is 19% on the first EUR 200,000 of taxable profit, and 25.8% on all taxable profits exceeding that threshold.

When to Hire a Lawyer

Navigating cross-border tax treaties and corporate substance laws requires specialized counsel. You should retain legal representation when drafting the Articles of Association for your holding company, structuring intercompany financing agreements, or negotiating Advance Tax Rulings with the Dutch tax authorities. Working with experienced business registration lawyers in the Netherlands ensures your corporate structure avoids anti-abuse penalties and complies fully with upcoming 2026 ATAD 3 regulations.

Next Steps

- Map your current European corporate structure and assess the physical and economic footprint of your existing or planned Dutch entities.

- Consult a Dutch civil-law notary to begin drafting the incorporation documents and verifying your proposed company name.

- Gather necessary KYC documentation for all shareholders holding more than 25% equity in preparation for the mandatory UBO registry filing.