- Common Law Foundation: The DIFC operates under an English-language common law framework, offering international investors a familiar legal environment compared to the UAE's onshore civil law system.

- Investment Flexibility: Venture capital (VC) deals in the DIFC utilize sophisticated instruments like SAFEs, KISSes, and convertible notes that are legally recognized and easily enforceable.

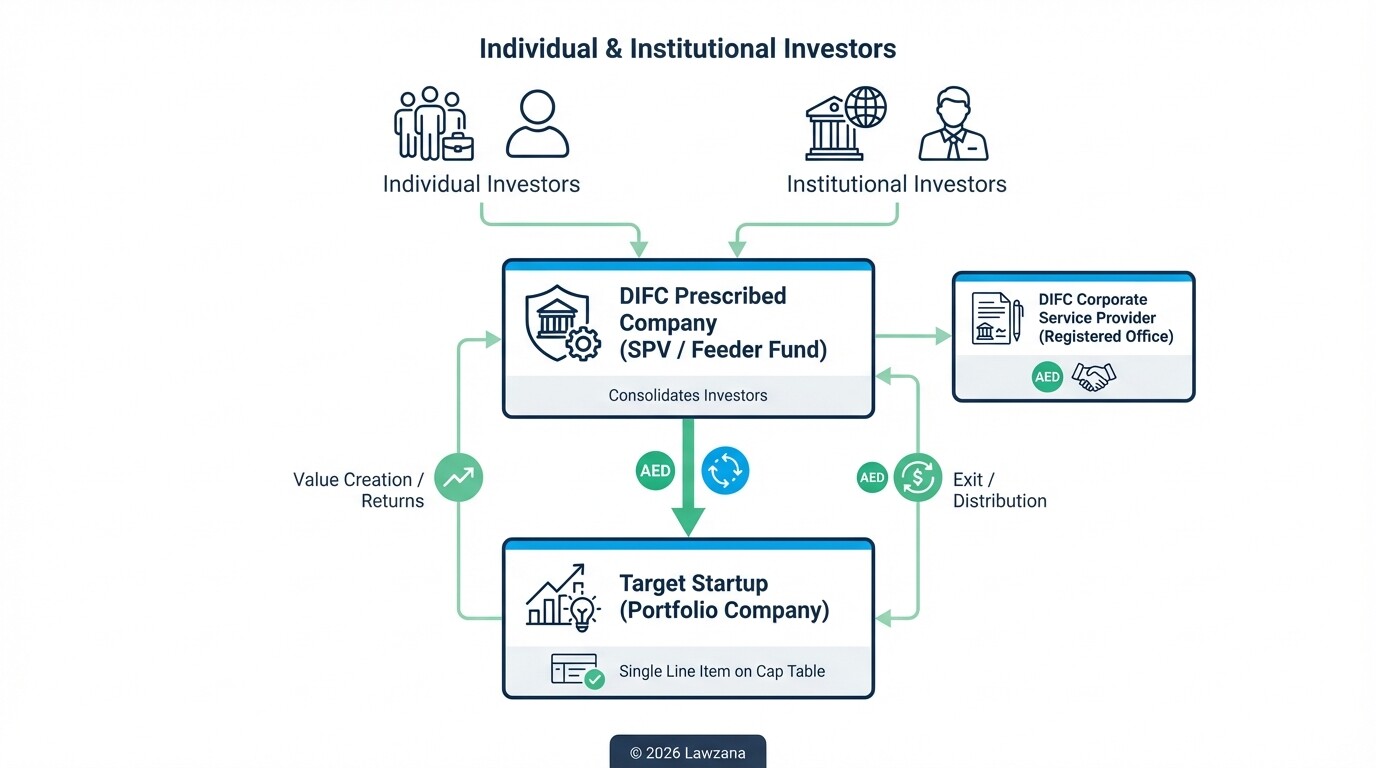

- Special Purpose Vehicles (SPVs): DIFC Prescribed Companies provide a cost-effective, "light-touch" regulatory option for holding assets and structuring deal flow.

- DFSA Oversight: Professional funds and private equity firms are regulated by the Dubai Financial Services Authority (DFSA), ensuring high standards of transparency and investor protection.

- Judicial Certainty: Disputes are handled by the DIFC Courts, an independent English-language judiciary with a proven track record of enforcing complex commercial contracts.

Benefits of DIFC Law vs. UAE Onshore Law for Investors

The Dubai International Financial Centre (DIFC) provides a "carve-out" from UAE federal civil law, allowing for total foreign ownership and the application of its own independent legal system based on English common law. For venture capital and private equity, this offers a level of contractual freedom and legislative clarity that is often difficult to mirror in the UAE onshore environment.

While UAE onshore law has evolved significantly with the new Companies Law, it still operates on a civil law basis, which can be less predictable for complex shareholder arrangements. The DIFC allows investors to utilize nuanced equity structures, such as multiple share classes with varying voting rights, which are essential for VC deals. Furthermore, the DIFC's legal framework is specifically designed to accommodate international finance standards, making it the preferred choice for cross-border investments and institutional capital.

| Feature | DIFC Law | UAE Onshore Law |

|---|---|---|

| Legal System | Common Law (English Language) | Civil Law (Arabic Language) |

| Foreign Ownership | 100% allowed | 100% allowed (subject to activities) |

| Share Classes | Unlimited flexibility | Historically restricted (though improving) |

| Court System | DIFC Courts (Common Law) | UAE Civil Courts |

| Regulatory Body | DFSA (Independent) | Ministry of Economy / SCA |

VC Shareholders' Agreement (SHA) Checklist and Sample Clauses

Structuring a VC deal in the DIFC requires a robust Shareholders' Agreement (SHA) that addresses governance, economic rights, and exit scenarios. Because the DIFC Companies Law (Law No. 5 of 2018) permits high levels of contractual customization, investors should ensure their SHA includes specific protections for minority and lead investors.

Essential SHA Checklist

- Capitalization Table: Clearly defined share classes (Seed, Series A, etc.) and anti-dilution provisions.

- Governance Rights: Board composition, observer rights, and "Reserved Matters" requiring investor consent.

- Transfer Restrictions: Right of First Refusal (ROFR) and Right of First Offer (ROFO).

- Exit Provisions: Drag-along and Tag-along rights to ensure a smooth liquidation or acquisition.

- Information Rights: Requirements for the company to provide audited financials and quarterly management reports.

Sample Clause: Drag-Along Rights

"In the event that a 'Qualified Seller' (as defined herein) proposes a Sale of the Company to a bona fide third-party purchaser, the Qualified Seller shall have the right to require all other Shareholders to sell their respective Shares to the purchaser on the same terms and conditions, provided that the consideration per share is no less than the Liquidation Preference applicable to the Series A Preferred Shares."

Sample Clause: Liquidation Preference

"In the event of any Liquidation Event, the holders of Series A Preferred Shares shall be entitled to receive, prior and in preference to any distribution of any of the assets of the Company to the holders of Common Shares, an amount per share equal to [1.0x] the Original Issue Price plus all declared but unpaid dividends."

Utilizing Special Purpose Vehicles (SPVs) for Deal Flow

SPVs in the DIFC, particularly the "Prescribed Company" structure, serve as efficient holding entities that isolate financial risk and facilitate the pooling of capital for specific investments. These entities benefit from a streamlined setup process and lower annual fees compared to full commercial licenses, making them ideal for private equity firms managing multiple deal flows.

The Prescribed Company regime allows investors to hold assets, shares in other companies, or intellectual property without the need for a physical office space within the DIFC, provided they use a DIFC-registered corporate service provider. This structure is frequently used for "feeder funds" where multiple small investors are aggregated into a single entity to simplify the capitalization table of the target startup.

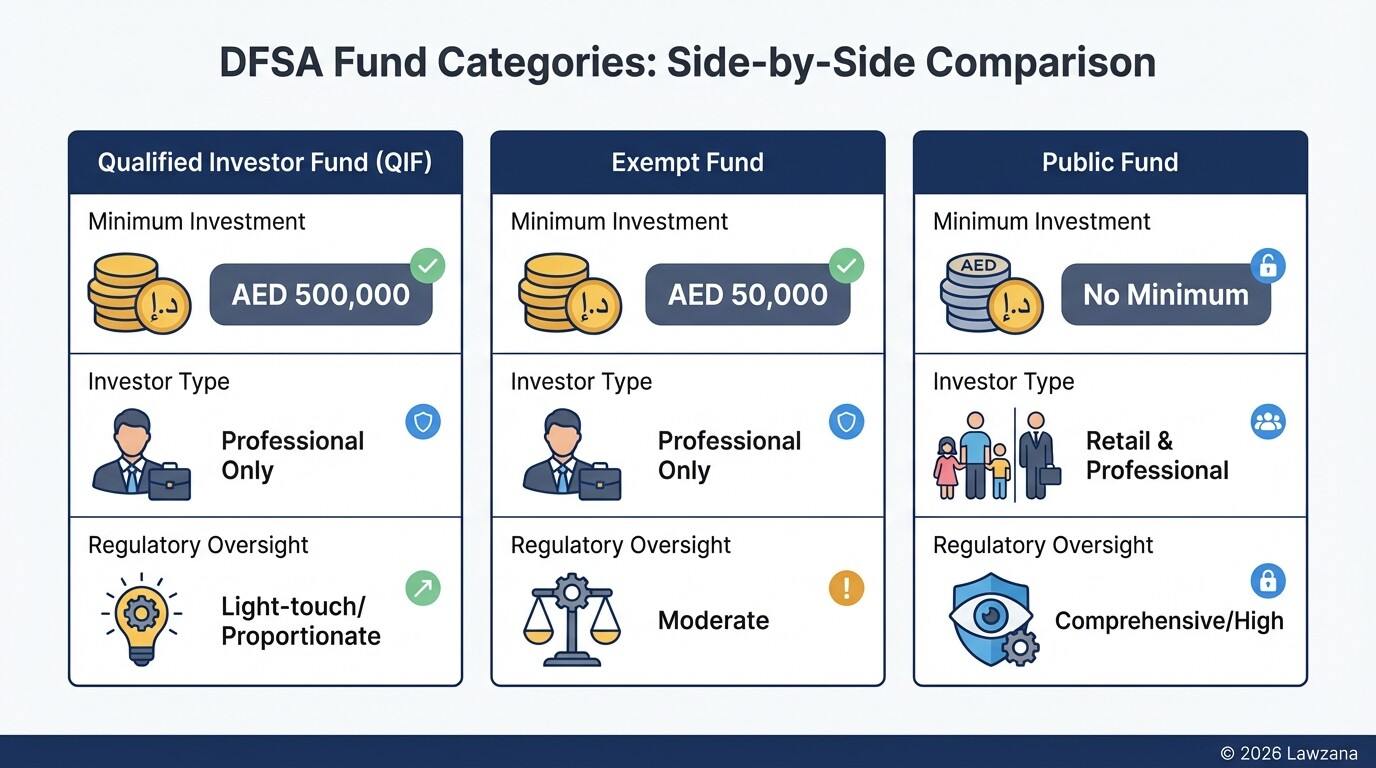

Regulatory Oversight by the DFSA for Investment Funds

Investment activity within the DIFC is strictly regulated by the Dubai Financial Services Authority (DFSA), which ensures that fund managers adhere to international best practices in conduct and prudential standards. For private equity and VC firms, this oversight provides a "badge of quality" that is essential when raising capital from global institutional investors.

The DFSA categorizes funds into different tiers, such as Public Funds, Exempt Funds, and Qualified Investor Funds (QIFs). Most VC and private equity deals fall under the QIF or Exempt Fund categories, which offer a more proportionate regulatory burden in exchange for higher minimum investment thresholds (typically $500,000 for QIFs). Firms must be authorized as a "Fund Manager" or "Domestic Firm" to manage these structures, ensuring that only sophisticated players operate within the ecosystem.

Exit Strategies and Enforcement of Rights in DIFC Courts

Exiting a VC investment in the DIFC is typically achieved through a trade sale, a secondary buyout, or an Initial Public Offering (IPO) on the Nasdaq Dubai. The DIFC framework provides clear mechanisms for these transitions, supported by an English-language court system that understands the complexities of "bad leaver" provisions and warranty claims.

If a dispute arises, the DIFC Courts have the power to issue injunctions and enforce the specific performance of a Shareholders' Agreement. This is a critical advantage for investors; if a founder refuses to honor a drag-along clause, the DIFC Courts can provide a swift remedy that is recognized both within the DIFC and through reciprocal enforcement treaties with other jurisdictions, including onshore UAE and the wider GCC.

Common Misconceptions About DIFC VC Structuring

Myth 1: "DIFC entities are only for companies physically located in Dubai."

Actually, a DIFC SPV or holding company can own assets, shares, and businesses anywhere in the world. It is a popular jurisdiction for "offshore" structuring of "onshore" assets because of the legal protections it offers, regardless of where the target company is headquartered.

Myth 2: "Structuring in the DIFC is too expensive for early-stage startups."

While the initial setup costs may be higher than some "offshore" tax havens, the introduction of the DIFC Innovation License and the Prescribed Company regime has significantly lowered the barrier to entry. The long-term savings in legal certainty and investor confidence often far outweigh the initial setup fees.

Myth 3: "DIFC Courts cannot enforce judgments in onshore Dubai."

This is incorrect. There is a robust judicial mechanism between the DIFC Courts and the Dubai Courts for the reciprocal enforcement of judgments. A ruling from a DIFC judge can be converted into an enforceable order in onshore Dubai without a rehearing of the merits of the case.

FAQ

What is the minimum capital requirement for a DIFC SPV?

There is no statutory minimum share capital for a DIFC Prescribed Company; it can be incorporated with as little as $100. However, regulated fund managers must meet specific capital adequacy requirements set by the DFSA.

Can I use a SAFE note for a DIFC-based startup?

Yes. The DIFC Companies Law is flexible enough to recognize "Simple Agreements for Future Equity" (SAFE) and "Keep It Simple Securities" (KISS), which are standard in Silicon Valley.

How long does it take to set up a DIFC holding company?

An SPV or Prescribed Company can typically be incorporated within 1 to 2 weeks, provided all Know Your Customer (KYC) documentation is in order and the applicant meets the eligibility criteria.

Do I need a physical office in the DIFC to structure a deal there?

Not necessarily. While commercial entities usually require a physical presence, Prescribed Companies can use the registered address of a DIFC-licensed Corporate Service Provider or a parent company already established in the district.

When to Hire a Lawyer

Navigating the DIFC's legal landscape requires professional expertise to ensure that your investment structure is both compliant and protective. You should consult a lawyer when:

- Drafting or negotiating a Shareholders' Agreement with complex equity rights.

- Applying for a Fund Manager license from the DFSA.

- Structuring a cross-border acquisition involving assets in multiple jurisdictions.

- Resolving a dispute between shareholders or enforcing exit rights.

- Converting an onshore UAE company into a DIFC-governed structure.

Next Steps

- Determine Eligibility: Confirm if your project qualifies for a DIFC Innovation License or a Prescribed Company structure to minimize costs.

- Engage a Registered Agent: If you do not plan to have a physical office, contact a licensed DIFC corporate service provider to act as your registered agent.

- Draft the Term Sheet: Outline the core economic and governance terms of the deal before moving to full documentation.

- Consult the DIFC Public Register: Verify the status of potential partners or service providers within the zone.

- Secure Legal Counsel: Work with a firm specialized in DIFC Law to finalize your SHA and Articles of Association.