- Continuity of Existence: Cyprus re-domiciliation laws allow international groups to move their seat of incorporation into or out of Cyprus without liquidating the original entity.

- Tax Optimization: Strategic use of the Cyprus participation exemption can result in 0% tax on capital gains from the sale of shares, provided no immovable property in Cyprus is involved.

- Substance is Mandatory: To remain compliant with 2026 EU anti-shell company regulations (ATAD3), Cyprus entities must demonstrate physical presence and genuine economic activity.

- English Law Influence: The Cyprus legal system is heavily based on English Common Law, providing a familiar and predictable framework for international M&A contracts.

The 2026 Cross-Border M&A Checklist for Cyprus

A successful cross-border transaction in Cyprus requires a phased approach that balances local statutory compliance with international tax standards. By following this checklist, lead counsel and corporate officers can ensure that the transition or acquisition meets all 2026 regulatory benchmarks.

Phase 1: Preliminary Structuring & KYC

- Verify Re-domiciliation Eligibility: Confirm that the foreign jurisdiction's laws permit the company to transfer its seat to Cyprus.

- UBO Disclosure: Prepare the Ultimate Beneficial Owner (UBO) declaration for the Cyprus Department of Registrar of Companies.

- AML/KYC Clearance: Complete Know Your Customer (KYC) documentation for all directors and significant shareholders as required by the Cyprus Bar Association.

Phase 2: Legal & Tax Due Diligence

- Substance Audit: Evaluate the target's physical office space, local payroll, and local management to ensure compliance with EU anti-shell regulations.

- Title Search: Confirm ownership of assets and check for existing charges or encumbrances at the Land Registry or Registrar of Companies.

- Employment Review: Assess Transfer of Undertakings (Protection of Employment) or TUPE implications if the deal involves a transfer of business assets rather than shares.

Phase 3: Transaction Documents

- Draft the SPA: Ensure the Share Purchase Agreement includes Cyprus-specific warranties and the correct tax indemnities.

- Stamp Duty Calculation: Submit the contract to the Tax Department for stamping within 30 days of signing to ensure it remains admissible in court.

- Dispute Resolution Clause: Select the governing law and forum (e.g., Cyprus Commercial Court or LCIA Arbitration).

Phase 4: Closing & Post-Merger

- Corporate Authorizations: Pass board and shareholder resolutions approving the merger or acquisition.

- Filings: Submit Form HE4 (change of directors) and Form HE2 (change of registered office) if applicable.

- Tax Residency Certificate: Apply for a Tax Residency Certificate from the Cyprus Tax Department to utilize Double Tax Treaties.

Utilizing Cyprus 'Re-domiciliation' Laws for International Groups

Re-domiciliation is the legal process that allows a company to change its jurisdiction of incorporation while maintaining its legal identity and history. Under Section 354C of the Companies Law, Cap. 113, foreign companies can "move" to Cyprus without the need for a costly and complex liquidation of the original foreign entity.

This mechanism is highly valued by international groups because it preserves the company's existing contracts, credit history, and property titles. To initiate this, a company must file an application with the Cyprus Registrar of Companies, supported by an affidavit of solvency and proof that the home jurisdiction allows such a move. Once the "Certificate of Temporary Continuation" is issued, the company is treated as a Cyprus entity for all legal and tax purposes. Within six months, the company must provide evidence that it has been struck off the foreign register to receive its final "Certificate of Continuation."

Tax-Efficient Structuring of Share Purchase Agreements (SPA)

Structuring an SPA in Cyprus focuses primarily on leveraging the jurisdiction's extensive tax treaty network and its favorable treatment of capital gains. Because Cyprus does not generally tax the disposal of securities, the primary goal of a well-drafted SPA is to ensure the transaction qualifies for these exemptions.

To maximize efficiency, the SPA should clearly distinguish between the sale of shares and the sale of underlying assets. Capital gains from the sale of shares are 100% exempt from tax in Cyprus unless the company owns immovable property located within Cyprus. Furthermore, there is no withholding tax on dividends paid to non-resident shareholders. Buyers should insist on specific tax indemnities that protect them from any historical "Special Defence Contribution" liabilities that the target company may have accrued but not yet paid.

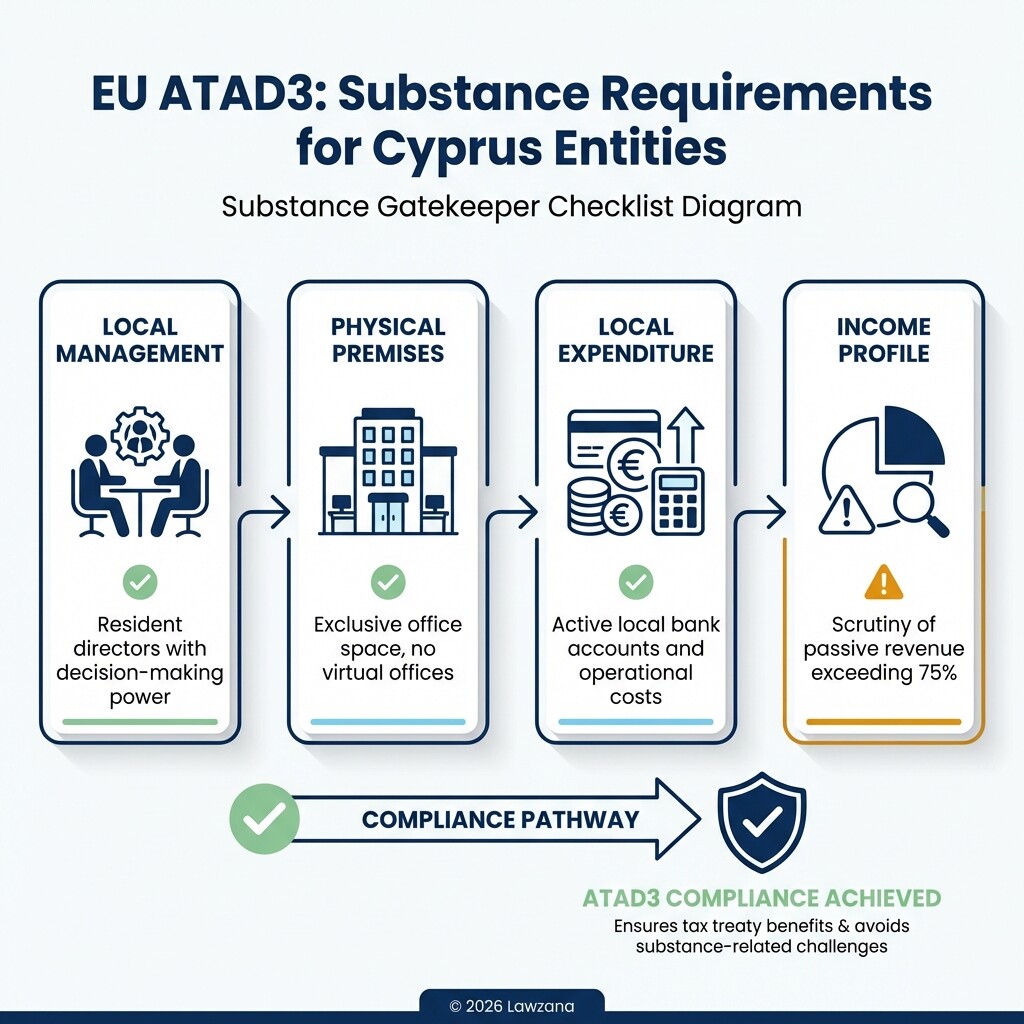

Compliance with EU-Wide Anti-Shell Company Regulations (ATAD3)

The 2026 legal landscape for Cyprus M&A is dominated by the EU's "Unshell" Directive (ATAD3), which targets entities with no or minimal economic substance. Cyprus companies used in cross-border structures must now prove they are not "shell" entities to retain their tax benefits.

To pass the substance test, a Cyprus company should meet the following "gatekeeper" criteria:

- Local Management: At least half of the company's directors should be residents of Cyprus and have the qualifications to make independent decisions.

- Physical Premises: The company must have exclusive use of an office in Cyprus (not just a "virtual office").

- Local Expenditures: The entity must incur operational expenses and hold a local bank account that is actively used for corporate business.

- Income Profile: If more than 75% of a company's revenue is "passive" (dividends, interest, royalties) and earned from cross-border activities, it is more likely to face scrutiny.

Dispute Resolution: Choosing Between Litigation and Arbitration

Parties in a Cyprus M&A deal must decide whether to resolve disputes in the newly established Cyprus Commercial Court or through international arbitration. While litigation was historically slow, the new Commercial Court is designed to handle high-value claims (over €2 million) with specialized judges and expedited procedures in English.

However, arbitration remains the preferred choice for cross-border deals due to confidentiality and the ease of enforcing awards under the New York Convention. When drafting your agreement, consider the following sample language to ensure clarity:

Sample Arbitration Clause:

"Any dispute, controversy, or claim arising out of or relating to this Agreement, including the formation, interpretation, breach, or termination thereof, shall be settled by arbitration in accordance with the [LCIA/ICC] Rules. The seat of arbitration shall be Nicosia, Cyprus. The language of the arbitration shall be English. The governing law of this contract shall be the substantive law of Cyprus."

Estimated Legal Costs for Mid-Market M&A Transactions

Legal and administrative costs for M&A in Cyprus are generally competitive compared to London or Luxembourg, but they vary based on the complexity of the cross-border elements. For a mid-market deal (transaction value between €5 million and €50 million), the following estimates apply:

| Service Category | Estimated Fee Range (EUR) | Timeline |

|---|---|---|

| Legal Due Diligence | €7,500 - €20,000 | 2-4 Weeks |

| SPA Drafting & Negotiation | €10,000 - €30,000 | 3-6 Weeks |

| Re-domiciliation Filings | €5,000 - €12,000 | 4-6 Months |

| Government Filing Fees | €500 - €2,000 | Varies |

| Stamp Duty | Capped at €20,000 | Within 30 days |

Note: These are estimates for legal fees; financial audit and tax advisory fees are typically billed separately.

Common Misconceptions About Cyprus Corporate Law

Myth 1: "Cyprus is a tax haven with no oversight."

Cyprus is a fully compliant EU member state and is on the "White List" of the OECD. While it offers a low corporate tax rate of 12.5%, it adheres to strict Anti-Money Laundering (AML) directives and automatic exchange of information (CRS/FATCA) standards.

Myth 2: "You must use Cyprus law for the SPA."

While the underlying transfer of shares in a Cyprus company must comply with the Cyprus Companies Law, the SPA itself can be governed by a foreign law (such as English law). However, it is often more practical to use Cyprus law to avoid the need for expert legal opinions on foreign law during local court proceedings.

Myth 3: "A 'postbox' address is enough for tax residency."

This is no longer true under 2026 regulations. The "Management and Control" test has evolved; if the actual decisions are made outside of Cyprus, the company risks losing its tax residency status and being taxed in the jurisdiction where the directors actually reside.

FAQ

What is the current corporate tax rate in Cyprus for 2026?

The standard corporate income tax rate remains 12.5%, one of the lowest in the European Union. However, companies must also account for the Global Minimum Tax (Pillar Two) if they are part of a large multinational group with annual revenues exceeding €750 million.

How long does a cross-border merger take in Cyprus?

A standard merger or re-domiciliation typically takes between 4 and 9 months. This timeline includes the preparation of financial statements, the statutory notice period for creditors, and the processing time at the Department of Registrar of Companies.

Is stamp duty mandatory for M&A contracts?

Yes, contracts relating to property or "matters to be done" in Cyprus must be stamped. For M&A deals, stamp duty is tiered based on the contract value but is conveniently capped at a maximum of €20,000 per agreement.

When to Hire a Lawyer

Cross-border M&A involves high stakes and complex regulatory intersections. You should engage a Cyprus corporate lawyer if:

- You are moving a corporate headquarters to Cyprus from a non-EU jurisdiction.

- Your transaction involves a "change of control" that requires notification to the Commission for the Protection of Competition (CPC).

- You need to draft complex shareholders' agreements with specific "drag-along" or "tag-along" rights.

- You are unsure if your current Cyprus structure meets the 2026 EU substance requirements.

Next Steps

- Conduct a Substance Audit: Before initiating an acquisition, review your existing Cyprus entities to ensure they meet 2026 ATAD3 standards.

- Secure Preliminary Tax Advice: Consult with a tax specialist to confirm that your proposed SPA structure qualifies for the participation exemption.

- Engage Local Counsel: Identify a Cyprus-based firm to handle the statutory filings and provide the necessary legal capacity opinions for the closing.