Structuring Commercial Real Estate Investments in Greece

- Greece recently updated its Golden Visa requirements, raising the minimum real estate investment to €800,000 in prime areas and €400,000 in remaining regions for 2024 through 2026.

- Establishing a Greek Private Company (IKE) offers superior liability protection and operational flexibility compared to direct foreign ownership for commercial real estate portfolios.

- Thorough due diligence requires pulling extracts from the Hellenic Cadastre, securing forestry certificates, and verifying zoning compliance with a civil engineer.

- Commercial leases in Greece carry a statutory minimum duration of three years, requiring carefully drafted rent indexation clauses to protect landlord ROI against inflation.

- Corporate investors must account for the 3.09% Property Transfer Tax at acquisition and the annual ENFIA property tax during the holding period.

Navigating the 2026 Greek Golden Visa Investment Thresholds

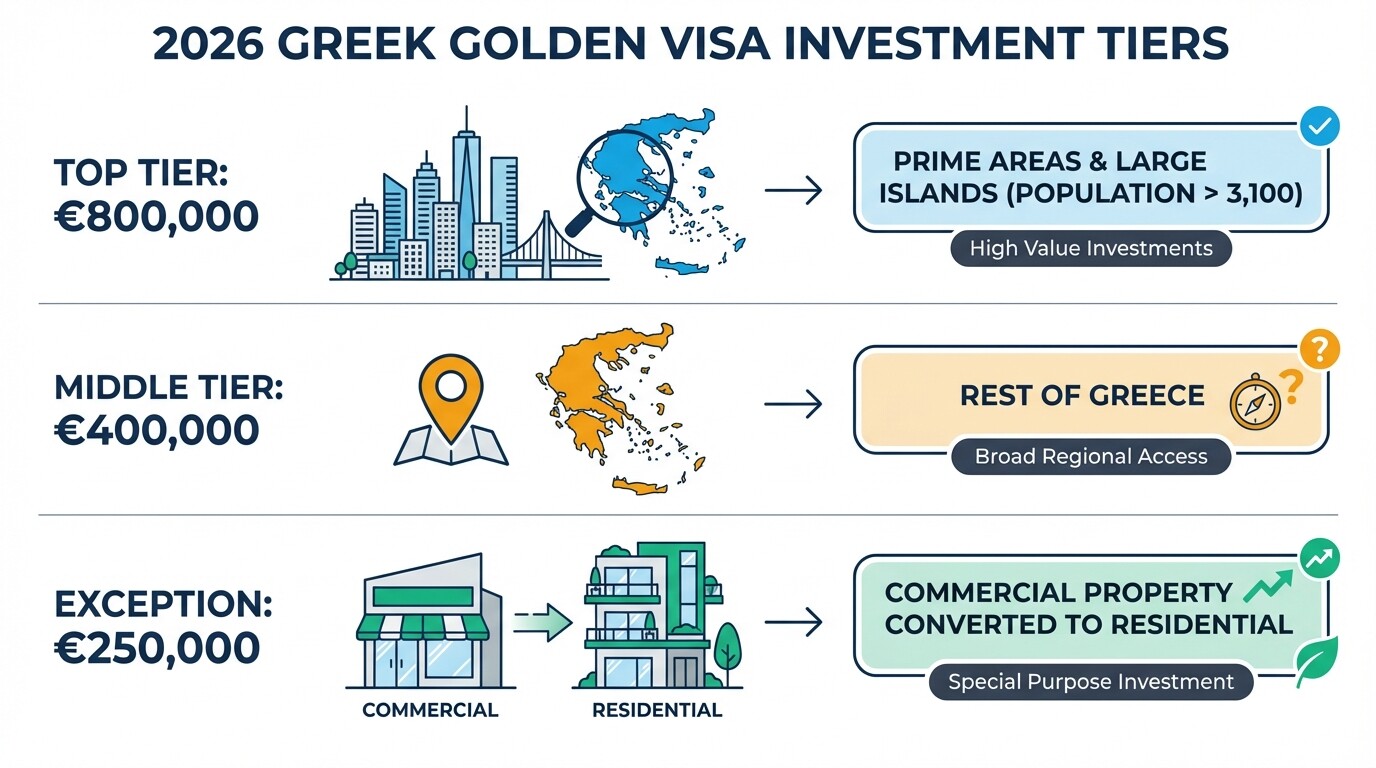

The Greek Golden Visa program offers a five-year, renewable residence permit for non-EU investors, but recent legislative updates have significantly altered the financial requirements. Starting in late 2024 and extending into 2026, the Greek government implemented a tiered system to cool the housing market while still attracting foreign direct investment.

For corporate investors leveraging the program, the investment threshold is now €800,000 for properties in high-demand regions like Attica, Thessaloniki, Mykonos, Santorini, and islands with a population over 3,100. In all other areas of Greece, the minimum investment is €400,000. Under these new rules, the investment must be made into a single property with a minimum surface area of 120 square meters.

There is a notable exception that benefits commercial real estate investors. The minimum threshold drops to €250,000 if the investor purchases a commercial property and officially converts its zoning use to residential before submitting the Golden Visa application. To stay compliant with the Ministry of Migration and Asylum, investors must ensure all funds are transferred from a foreign bank account into a Greek financial institution under the applicant's name prior to executing the final notary act.

What Are the Alternative Structures for Holding Greek Real Estate?

Choosing the right corporate vehicle determines your tax liability, administrative burden, and liability exposure in Greece. International corporate investors typically choose between acquiring commercial property directly through a foreign corporate entity or establishing a local Greek Private Company, known as an IKE (Idiotiki Kefalaiouchiki Etaireia).

Direct foreign ownership is simpler to set up initially but exposes the parent company to direct tax filings in Greece and potential cross-border liability. Establishing an IKE is the preferred route for commercial portfolios. An IKE isolates risk, requires only €1 in statutory minimum capital, and can be established entirely online through the Greek General Commercial Registry (GEMI) within a few days.

| Feature | Direct Foreign Entity Ownership | Greek Private Company (IKE) |

|---|---|---|

| Setup Process | Requires issuing a Greek Tax Number (AFM) for the foreign entity and appointing a local tax representative. | Requires incorporating a local entity via GEMI and opening a Greek corporate bank account. |

| Liability | The foreign parent company assumes direct liability for property-related claims. | Liability is limited to the local Greek entity's assets. |

| Corporate Tax | 22% on Greek-sourced rental income. Subject to double taxation treaties. | 22% flat corporate tax rate on net profits. |

| Dividend Tax | Governed by the parent entity's jurisdiction and tax treaties. | 5% withholding tax on dividends distributed to shareholders. |

| Maintenance | Requires annual tax filings for Greek-sourced income. | Requires full local accounting, annual financial statements, and a registered local address. |

Commercial Real Estate Due Diligence Checklist

Securing a clean title and ensuring regulatory compliance requires rigorous checks against multiple Greek registries before signing a preliminary contract. Missing a single clearance can render a commercial property legally unsellable or block future commercial operations.

Corporate buyers should execute the following due diligence steps in tandem with their legal counsel and a licensed Greek civil engineer:

- Verify Title via the Hellenic Cadastre: Obtain an updated extract from the Hellenic Cadastre (Ktimatologio) or the local Land Registry (Ypothikofylakeio) to confirm the seller has absolute ownership and that no mortgages, liens, or third-party claims exist.

- Confirm Structural Legality: A civil engineer must inspect the property and issue a certificate confirming that the actual built structure matches the approved building permit. Any unauthorized extensions or modifications must be legally settled (regularized) and the corresponding fines paid by the seller before the transfer.

- Obtain Forestry and Archaeological Clearances: For land purchases or out-of-plan developments, you must secure certificates proving the land is not designated as protected forest land or an archaeological site.

- Review Zoning and Urban Planning: Confirm with the local municipality that the property's designated use allows for your intended commercial activity (e.g., retail, logistics, hospitality).

- Secure the Energy Performance Certificate (EPC): The seller must provide a valid EPC, which is a strict legal prerequisite for drafting the final purchase deed and drafting subsequent lease agreements.

- Check Tax and Social Security Clearances: The seller must provide valid certificates proving they owe no debts to the Greek tax authorities or the national social security fund (e-EFKA).

Drafting Bulletproof Commercial Lease Agreements

A robust commercial lease agreement under Greek law must clearly delineate maintenance responsibilities, rent adjustment indices, and exit clauses to protect your return on investment. Standard Greek commercial leases strongly favor tenant stability, so corporate landlords must draft specific protections into the contract.

Under Greek Law 4242/2014, commercial leases have a statutory minimum duration of three years, even if the written contract specifies a shorter term. Landlords cannot evict a tenant during this period without proving a breach of contract, such as unpaid rent. To protect against inflation, corporate investors must include a clear rent indexation clause. If a lease does not specify how rent increases, Greek law mandates an automatic annual increase equal to 75% of the official Consumer Price Index (CPI).

Sample Rent Indexation Provision: "The Parties agree that the Monthly Base Rent shall be adjusted annually on the anniversary of the Commencement Date. The adjusted Monthly Base Rent shall be increased by a percentage equal to the official Consumer Price Index (CPI) of Greece for the preceding twelve months, as published by the Hellenic Statistical Authority (ELSTAT), plus a fixed margin of two percent (2.0%). In no event shall the adjusted Monthly Base Rent be less than the rent payable in the immediately preceding year."

Managing Greek Property Taxes for Corporate Investors

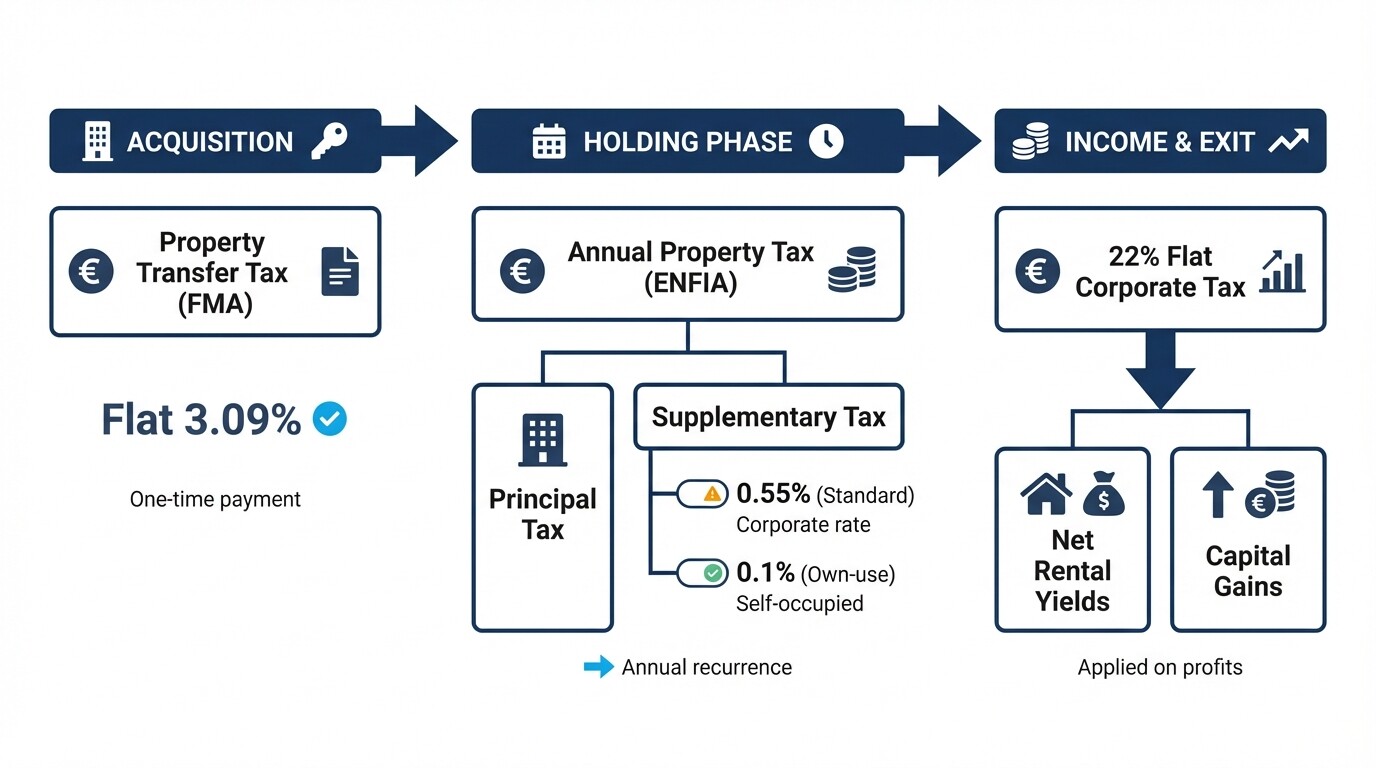

Corporate investors face several direct taxes when acquiring and holding commercial real estate in Greece, including the annual property tax (ENFIA) and corporate income tax on rental yields. Proper structuring minimizes the impact of property transfer taxes and capital gains tax upon exit.

Property Transfer Tax (FMA): Purchasing commercial real estate triggers a flat Property Transfer Tax of 3.09% calculated on the property's objective tax value or the purchase price, whichever is higher. This tax is borne entirely by the buyer and must be paid before signing the final notary deed.

Annual Property Tax (ENFIA): Every property owner in Greece is subject to the Unified Real Estate Ownership Tax (ENFIA). For corporate entities, ENFIA consists of a principal tax based on the property's size, location, and age, plus a supplementary tax calculated at 0.55% of the total objective value of the company's real estate portfolio. Properties used exclusively for the company's own commercial operations enjoy a reduced supplementary tax rate of 0.1%.

Corporate Income and Capital Gains Tax: Rental income generated by an IKE is taxed at the flat corporate rate of 22% after deducting allowable expenses, such as depreciation, maintenance, and interest on financing. When a corporate entity sells a Greek commercial property, the profit is not taxed under a separate capital gains regime. Instead, the gain is treated as ordinary business income and is taxed at the standard 22% corporate rate.

Common Misconceptions About Greek Real Estate Investment

- Purchasing real estate automatically grants tax residency in Greece. Securing a Golden Visa gives you the right to reside in Greece, but you do not become a Greek tax resident unless you spend more than 183 days a year in the country or move your center of vital interests to Greece.

- The notary guarantees the property is structurally legal. A Greek notary public ensures the legal validity of the title transfer and contract execution. They do not visit the property or verify its physical state. A civil engineer must be hired independently to verify structural legality.

- Commercial rent can be increased at will after the lease expires. If a commercial lease expires and the tenant remains in the property paying rent without objection from the landlord, the lease automatically converts to an indefinite-term contract. Evicting a tenant or changing the rent at this stage requires formal legal notice and often litigation.

Frequently Asked Questions

Can a foreign company act as the sole shareholder of a Greek IKE?

Yes. A Greek IKE can be established as a single-member company where 100% of the corporate shares are held by a foreign parent entity. The parent company must obtain a Greek tax number to complete the incorporation.

Are off-plan commercial properties eligible for the Golden Visa?

Yes. Investors can apply for the Golden Visa by signing a notarized preliminary contract for an off-plan property, provided they pay the minimum required investment amount as a deposit and the contract details the exact completion timeline.

How long does it take to complete a commercial real estate transaction in Greece?

A standard commercial real estate transaction takes between two and four months from the time an offer is accepted. The timeline is largely driven by how quickly the seller can gather the mandatory tax, engineering, and forestry clearances.

Can I pass ENFIA property taxes onto my commercial tenants?

Under Greek law, the legal owner of the property is solely responsible for paying ENFIA to the tax authorities. However, landlords can legally negotiate clauses in the lease agreement requiring the tenant to reimburse the landlord for the cost of ENFIA as part of the total annual operating expenses.

When to Hire a Lawyer

Navigating cross-border capital flows, local corporate structuring, and rigorous municipal due diligence requires specialized local counsel. You should engage a legal team before submitting an initial letter of intent or paying a reservation fee. A lawyer will secure your Greek tax number, appoint your local tax representative, conduct the comprehensive registry checks, and draft the final sale and purchase agreement to ensure compliance with Golden Visa thresholds and Greek commercial law.

Next Steps

- Define your investment strategy and determine if your priority is long-term rental yield, capital appreciation, or securing the Golden Visa.

- Select the optimal corporate structure with your tax advisors, weighing the benefits of a local IKE against direct foreign ownership.

- Engage a local legal and engineering team to conduct preliminary due diligence on short-listed properties before making binding offers.

- To find vetted legal partners experienced in structuring cross-border property acquisitions and local entity incorporation, connect with specialized corporate and commercial lawyers in Greece through Lawzana.