- Hong Kong relies on Schemes of Arrangement and formal liquidation rather than a statutory corporate rescue mechanism like US Chapter 11.

- Foreign companies can be wound up in Hong Kong courts if they demonstrate a sufficient connection to the jurisdiction, such as local assets or operations.

- Parent company directors face strict personal liability for fraudulent trading and misfeasance if they allow an insolvent subsidiary to continue incurring debt.

- Cross-border restructuring requires specific documentation to secure recognition of foreign liquidators under Hong Kong common law or mutual agreements.

Restructuring and Insolvency Options in Hong Kong

Multinational parent companies managing distressed Hong Kong subsidiaries can choose between formal liquidation and alternative restructuring mechanisms. The right path depends on the subsidiary's financial viability, creditor consensus, and the parent company's long-term strategic goals.

| Restructuring Option | Best Used For | Court Involvement | Typical Outcome |

|---|---|---|---|

| Scheme of Arrangement | Viable companies needing to restructure complex debt | High (Requires court sanction) | Company survives with new debt terms |

| Creditors' Voluntary Liquidation (CVL) | Insolvent companies with no viable future | Low (Shareholder and creditor driven) | Orderly dissolution of the company |

| Compulsory Winding-Up | When creditors force liquidation due to unpaid debt | High (Initiated by court petition) | Liquidation managed by a court appointee |

| Informal Workout | Situations with a small number of cooperative lenders | None (Private contract) | Refinanced or restructured private debt |

Initiating Voluntary vs Compulsory Winding-Up Procedures

Winding up a Hong Kong subsidiary can happen voluntarily through a shareholder resolution or compulsorily through a court order. Voluntary liquidation is generally faster and more cost-effective, while compulsory liquidation is necessary when creditors force the action due to unmanageable debts.

Creditors' Voluntary Liquidation (CVL) A CVL begins when the shareholders resolve that the company cannot continue its business due to its liabilities. The company then convenes a meeting of creditors, who ultimately have the right to nominate the liquidator. This process keeps the matter largely out of court and allows for a more predictable winding-down of operations.

Compulsory Winding-Up This process is driven by a petition to the High Court under the Companies (Winding Up and Miscellaneous Provisions) Ordinance (Cap. 32). A creditor, shareholder, or the company itself can file the petition.

- The most common ground is the inability to pay debts.

- Creditors often issue a statutory demand first. If the company fails to pay a debt exceeding HKD 10,000 within three weeks, it is deemed unable to pay its debts.

- Once the court grants a winding-up order, the Official Receiver or a provisional liquidator takes control of the subsidiary's assets.

Alternative Debt Restructuring Mechanisms Outside Formal Liquidation

Hong Kong does not currently have a statutory corporate rescue procedure, so companies rely on Schemes of Arrangement or informal debt workouts. These mechanisms allow a distressed subsidiary to negotiate new repayment terms while continuing business operations.

Scheme of Arrangement A Scheme of Arrangement is a statutory procedure that allows a company to reach a binding compromise with its creditors. It requires approval from a majority in number representing 75 percent in value of the creditors present and voting. Once approved by the creditors and sanctioned by the court, the scheme binds all creditors, including dissenting minority voices.

Informal Debt Workouts When a subsidiary owes debt to a small syndicate of banks or a single major creditor, informal workouts are highly effective. These are purely contractual agreements to reschedule or forgive debt. Because they require unanimous consent from all involved parties, they are unsuitable for companies with widely held, fragmented debt.

Required Documentation for Cross-Border Insolvency Recognition Checklist

To recognize foreign insolvency proceedings in Hong Kong, liquidators must apply to the High Court under common law principles or existing mutual recognition frameworks. Accurate documentation is critical to prove the foreign court's jurisdiction and the liquidator's authority to manage local assets.

Use this checklist to prepare a cross-border recognition application:

- Letter of Request: A formal letter issued by the foreign court respectfully requesting the assistance of the Hong Kong High Court.

- Order of Appointment: A certified, authenticated copy of the court order appointing the foreign liquidators or restructuring officers.

- Evidence of COMI: Documentation proving the subsidiary's Center of Main Interests is located in the jurisdiction where the primary insolvency proceedings are taking place.

- Affirmation of Facts: A sworn statement by the foreign liquidator detailing the company's financial position, the assets located in Hong Kong, and the specific powers required from the Hong Kong court.

- List of Hong Kong Creditors: An itemized list of any local creditors whose rights might be affected by the recognition order.

Protecting International Creditor Rights During the Restructuring Process

International creditors operating in Hong Kong are protected by the pari passu principle, which ensures the equal distribution of assets among unsecured creditors. Creditors can actively participate in proceedings by joining the committee of inspection or submitting formal claims to the liquidator.

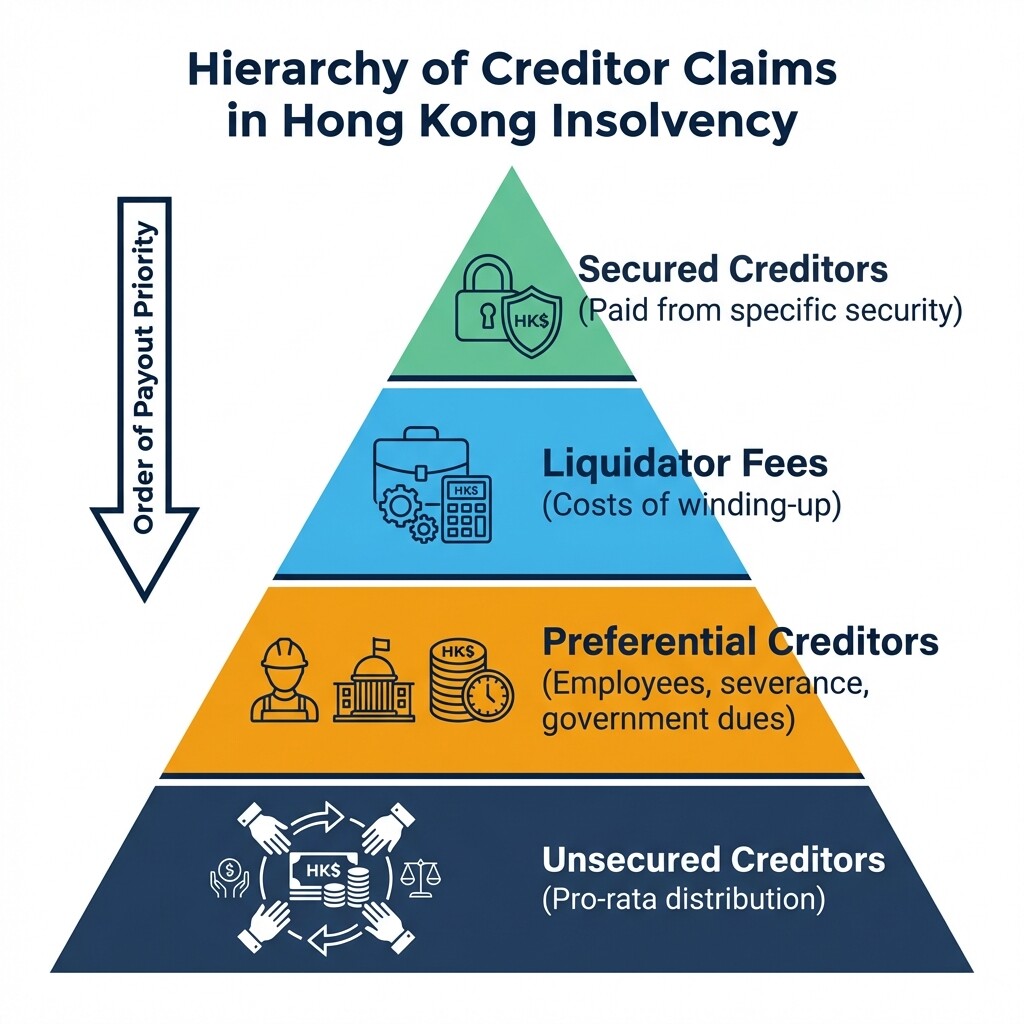

To protect their rights, creditors should understand the statutory priority of claims in Hong Kong. Assets are distributed in a strict hierarchy:

- Secured Creditors: Paid first from the proceeds of their specific security enforcement.

- Liquidator Fees: The costs and expenses of the winding-up process itself.

- Preferential Creditors: Statutory entitlements, such as employee wages, severance pay, and specific government dues.

- Unsecured Creditors: Paid out of the remaining asset pool on a pro-rata basis.

Creditors must submit a formal Proof of Debt form to the liquidator to claim their share of any distribution. The Official Receiver's Office provides specific guidelines and statutory forms for registering these claims during a compulsory winding-up.

Managing Director Liability and Corporate Governance Risks in 2026

Directors of distressed Hong Kong subsidiaries face severe personal liability if they fail to act in the best interests of creditors once insolvency becomes inevitable. The regulatory landscape demands strict adherence to fiduciary duties to avoid claims of unfair preference or fraudulent trading.

Parent company executives acting as directors for a Hong Kong subsidiary must navigate several specific risks:

- Fraudulent Trading: If a company carries on business with the intent to defraud creditors, directors can be held personally responsible for all debts without limitation. This carries both civil and criminal penalties.

- Misfeasance: Liquidators can sue directors for misapplying company funds or breaching their fiduciary duties in the lead-up to insolvency.

- Unfair Preferences: Paying off a specific creditor (such as the parent company) while ignoring others within six months to two years before liquidation can be challenged and reversed by the court.

Common Misconceptions About Hong Kong Insolvency

Parent companies often misunderstand Hong Kong's restructuring framework, leading to costly delays and compliance failures. Correcting these assumptions early prevents unnecessary legal exposure.

- Misconception: Hong Kong has a Chapter 11 equivalent. Many foreign executives assume they can file for immediate statutory protection from creditors while they restructure. Hong Kong does not have a debtor-in-possession rescue regime; a Scheme of Arrangement requires complex planning and does not automatically freeze creditor actions.

- Misconception: Foreign entities cannot be liquidated in Hong Kong. Parent companies often believe a subsidiary incorporated in the BVI or Cayman Islands but operating in Hong Kong cannot be wound up locally. The High Court regularly winds up unregistered foreign companies if they have a sufficient connection to Hong Kong, such as local assets, directors, or operations.

Frequently Asked Questions

What is the threshold for a statutory demand in Hong Kong?

A creditor can issue a statutory demand against a company for any undisputed debt exceeding HKD 10,000. If the debt is not paid within three weeks, the creditor can petition the court for a compulsory winding-up.

How long does a Scheme of Arrangement take to complete?

A straightforward Scheme of Arrangement typically takes four to six months to implement. Highly complex cross-border restructurings can take well over a year due to the need for multiple court hearings and creditor negotiations.

Can a parent company fund the restructuring of its Hong Kong subsidiary?

Yes. Parent companies frequently provide "white knight" funding to facilitate a Scheme of Arrangement. However, this funding must be structured carefully to ensure it does not violate rules against unfair preferences.

When to Hire a Restructuring Lawyer

Engaging legal counsel is essential the moment a Hong Kong subsidiary shows signs of severe financial distress or cannot pay its debts as they fall due. Early intervention allows parent companies to control the narrative, prevent compulsory liquidation petitions, and explore out-of-court solutions.

You should consult restructuring and insolvency lawyers in Hong Kong immediately if creditors threaten statutory demands or if the board is concerned about personal liability for insolvent trading. Legal experts will help you assess whether a Scheme of Arrangement or a strategic winding-up is the safest path forward.

Next Steps for Parent Companies

Taking immediate, documented action protects both the subsidiary's remaining value and the parent company's directors. Follow a structured approach to assess the financial reality and execute the restructuring plan.

- Conduct a Solvency Audit: Review cash flow forecasts to determine exactly when the subsidiary will run out of funds to pay its immediate debts.

- Halt Preferential Payments: Stop all non-essential payments, particularly those to related corporate entities, to avoid subsequent clawback claims by a liquidator.

- Hold Documented Board Meetings: Keep meticulous minutes of all board meetings demonstrating that directors are actively considering the interests of creditors, not just the parent company.

- Engage Financial and Legal Advisors: Hire local professionals to draft a restructuring proposal or prepare the necessary filings for a Creditors' Voluntary Liquidation.