Corporate Governance in Iceland: An Investor's Guide

- Strict Role Separation: Icelandic corporate law distinctly separates the strategic oversight of the Board of Directors from the day-to-day operational control of the Managing Director.

- Mandatory AGM Filings: Companies must hold an Annual General Meeting (AGM) within eight months of the financial year-end and submit audited accounts to the Register of Enterprises.

- Residency Requirements: The managing director and a majority of the board must reside in an EEA or OECD member state unless a special exemption is granted.

- Formal Minute Keeping: Maintaining a legally compliant, signed minute book (gerðabók) is an absolute requirement for validating corporate decisions and shielding directors from liability.

- Personal Liability Risks: Directors can be held personally liable for unpaid corporate taxes or damages caused by gross negligence, making regular governance audits essential.

Roles and Responsibilities: Board vs. Managing Director

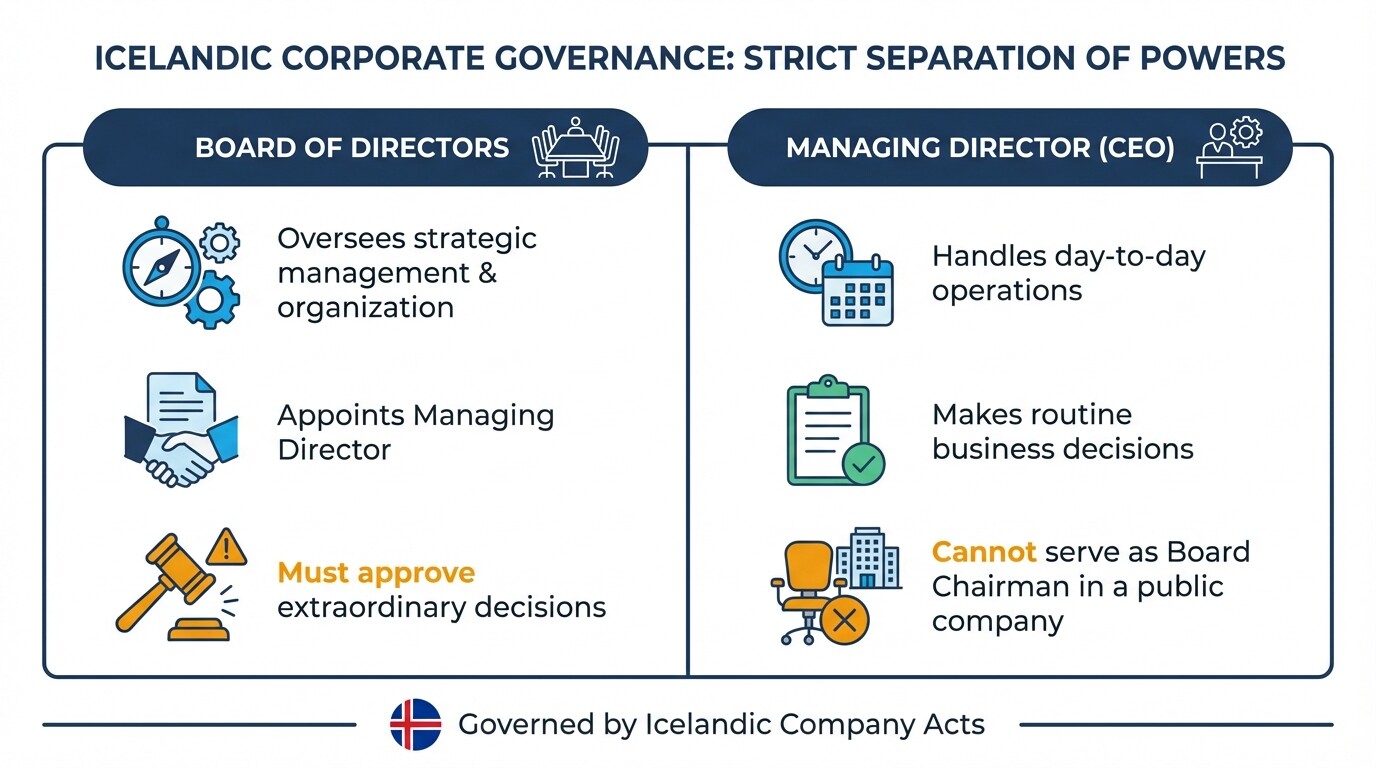

In Iceland, the Board of Directors oversees strategic management and corporate organization, while the Managing Director (CEO) handles day-to-day operations. The law strictly separates these roles to ensure proper corporate oversight, accountability, and prevention of operational overreach.

The legal framework for this separation is defined by the Icelandic Public Limited Companies Act (No. 2/1995) and the Private Limited Companies Act (No. 138/1994). The Board is elected by shareholders and is responsible for appointing the Managing Director. While the Managing Director makes routine business decisions, they cannot make extraordinary or strategically critical decisions without explicit board approval. Furthermore, in a public limited company, the Managing Director cannot simultaneously serve as the Chairman of the Board.

Annual General Meeting (AGM) Documentation and Filing Checklist

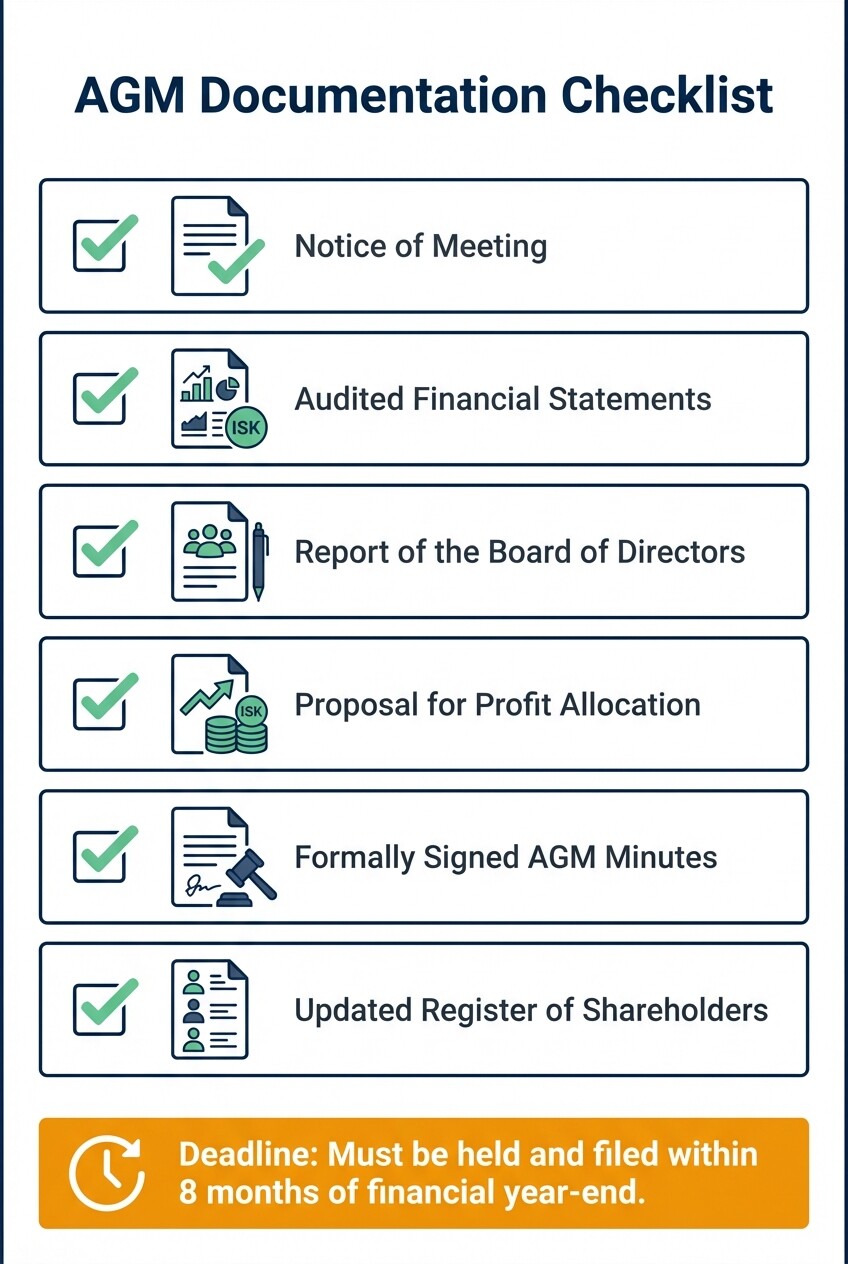

Icelandic corporate law mandates that companies hold an Annual General Meeting within eight months of the financial year's end. Proper documentation, including financial statements and board reports, must be approved during this meeting and subsequently filed with the Register of Enterprises (Fyrirtækjaskrá), which operates under Iceland Revenue and Customs.

Foreign investors and local directors must prepare and execute the following documents to maintain compliance:

- Notice of Meeting: Must be distributed to all shareholders strictly within the timeframe stipulated by the company's Articles of Association.

- Audited Financial Statements: Annual accounts prepared in accordance with the Icelandic Annual Accounts Act, audited or reviewed by a certified public accountant if the company meets size thresholds.

- Report of the Board of Directors: A formal narrative detailing the company's performance, significant events during the year, and future outlook.

- Proposal for Profit Allocation: A formal resolution detailing the distribution of dividends or the allocation of losses, requiring shareholder approval.

- AGM Minutes: A formally signed record of all resolutions passed at the meeting, including the election of board members and auditors.

- Updated Register of Shareholders: Must be present at the meeting and updated if any share transfers occurred.

Requirements for Recording and Retaining Corporate Minutes

Icelandic companies must maintain a formal minute book (gerðabók) recording all decisions made at board meetings and shareholder assemblies. These records are legally binding documents that prove corporate compliance, validate strategic decisions, and protect directors from personal liability claims.

The minute book serves as the definitive legal record of corporate actions. During board meetings, the minutes must capture the attendees, the agenda, the nature of the discussions, and the exact resolutions passed. If a board member disagrees with a decision, they have a legal right and obligation to have their dissenting opinion recorded in the minutes to shield themselves from subsequent liability. All minutes must be formally signed by the attending board members or shareholders. These records must be kept at the company's registered headquarters in Iceland and remain accessible for inspection by authorized parties or auditors.

Common Compliance Mistakes by Foreign Board Members

Foreign investors frequently misjudge Icelandic residency requirements and understate the legal weight of formal administrative procedures. Failing to adapt to local corporate statutes can result in delayed registrations, daily financial penalties, or unexpected personal liability for international directors.

Misconception 1: Email approvals can replace formal meeting minutes. Many foreign executives assume that an email chain confirming a decision is sufficient for corporate record-keeping. Under Icelandic law, electronic communication is helpful, but the decisions must still be formally entered into the official minute book and signed by the directors to be legally valid and enforceable.

Misconception 2: Anyone can serve on an Icelandic board. International investors often attempt to appoint entirely non-European boards to their Icelandic subsidiaries. By law, the managing director and at least half of the board members must be residents of Iceland or another European Economic Area (EEA) or OECD country. Appointing residents from outside these zones requires a specific exemption from the Ministry of Culture and Business Affairs.

Misconception 3: Corporate debt liability is completely shielded. There is a dangerous myth that registering a private limited company (einkahlutafélag) guarantees absolute immunity from corporate debts. If foreign board members act with gross negligence, fail to file taxes, or continue trading while insolvent without notifying shareholders, Icelandic courts can pierce the corporate veil and hold directors personally liable for financial damages and unpaid public levies.

Strategies to Prevent Personal Liability

Board members in Iceland can face personal liability for corporate debts or statutory violations if they act with negligence or fail to oversee the managing director adequately. Conducting regular corporate governance audits is the most effective strategy to identify gaps, ensure statutory compliance, and mitigate these legal risks.

To establish a strong defense against liability claims, boards should implement the following audit and oversight practices:

- Conduct Quarterly Minute Audits: Review the minute book to ensure all strategic decisions, conflict of interest declarations, and dissenting votes are accurately documented and signed.

- Implement Financial Checkpoints: Demand regular, standardized financial reporting from the Managing Director to ensure the company remains solvent. Directors are liable if they allow a company to continue operations when equity falls below half of the registered share capital (minimum 500,000 ISK for private limited companies).

- Verify Tax and Customs Filings: Regularly audit the company's compliance with value-added tax (VAT), withholding taxes, and pension fund contributions. Unpaid public levies are the most common source of personal liability for directors in Iceland.

- Maintain Directors and Officers (D&O) Insurance: Secure comprehensive D&O liability insurance tailored to the Icelandic market to protect board members' personal assets against legal defense costs and settlement claims.

Frequently Asked Questions

What is the deadline for filing annual accounts in Iceland?

Icelandic companies must submit their approved annual accounts to the Register of Enterprises no later than eight months after the end of their financial year. Late submissions trigger daily administrative fines and can eventually lead to the forced dissolution of the company.

Can a foreign national be the managing director of an Icelandic company?

Yes, a foreign national can serve as the managing director provided they are a resident of an EEA or OECD member state. If they reside outside these areas, they must apply for a specific exemption from the Icelandic government.

Are electronic signatures valid for Icelandic corporate documents?

Yes, qualified electronic signatures (such as those issued by Icelandic authorities like Auðkenni or recognized EU trust service providers) are legally binding and routinely used for signing annual accounts, board minutes, and registry filings.

What is the minimum share capital for a company in Iceland?

The minimum share capital for a private limited company (einkahlutafélag or ehf.) is 500,000 ISK. For a public limited company (hlutafélag or hf.), the minimum share capital required is 4,000,000 ISK.

When to Hire a Corporate Governance Lawyer

Engaging legal counsel is crucial when establishing a new corporate entity, drafting Articles of Association, or structuring a board with international members. You should also consult a lawyer immediately if your company approaches insolvency, if shareholders dispute a board decision, or if you need to apply for residency exemptions for foreign directors. Navigating Icelandic corporate law requires precise local knowledge to prevent procedural errors that carry heavy financial penalties.

Next Steps for Foreign Investors

If you are managing an Icelandic subsidiary or joining a local board, begin by conducting a thorough review of the company's existing Articles of Association and the official minute book. Ensure that your current board composition meets the EEA/OECD residency requirements and that all past annual accounts have been successfully filed with Skatturinn. To secure your compliance framework and protect your personal assets, connect with experienced corporate governance lawyers in Iceland who can perform a comprehensive governance audit tailored to your operations.