- Shareholder disputes in India are primarily governed by the Companies Act, 2013, with the National Company Law Tribunal (NCLT) serving as the primary adjudicatory body.

- Minority shareholders holding at least 10% of the issued share capital have the statutory right to file petitions for oppression and mismanagement.

- The NCLT has broad powers to grant interim relief, including staying board meetings, freezing bank accounts, or restraining the transfer of shares.

- Well-drafted Shareholders' Agreements (SHA) can preemptively resolve many disputes through structured buy-sell provisions or mandatory mediation.

- Litigation can significantly hamper a company's ability to raise capital, as venture capital and private equity firms often avoid entities with ongoing "deadlock" or "oppression" claims.

What are the grounds for filing a petition with the National Company Law Tribunal (NCLT)?

Shareholders can file a petition under Section 241 of the Companies Act, 2013, if the company's affairs are being conducted in a manner prejudicial to public interest, the company, or any member. The legal threshold requires proving that the acts are "oppressive" (harsh, burdensome, and wrongful) or constitute "mismanagement" (gross negligence or financial impropriety).

The NCLT reviews specific grievances to determine if they meet the legal standard for intervention:

- Oppression: This involves a visible departure from the standards of fair dealing. Examples include the illegal issuance of shares to reduce a majority to a minority, withholding dividends unfairly, or excluding a director from participating in management despite their right to do so.

- Mismanagement: This relates to the conduct of the company's business. Common grounds include the diversion of corporate funds for personal use, gross inefficiency resulting in heavy losses, or unauthorized sale of company assets.

- Material Change: A petition can also be filed if a significant change has occurred in the management or control of the company (e.g., an alteration in the board of directors or ownership) that makes it likely that the company's affairs will be conducted in a prejudicial manner.

Understanding Minority Shareholders' Rights in India

Minority shareholders in India are protected against the "tyranny of the majority" through statutory rights and contractual protections in the Shareholders' Agreement. While the majority generally has the right to manage the company, the law ensures that minority interests cannot be trampled upon without legal recourse.

Key protections for minority shareholders include:

- Statutory Threshold for Action: Under Section 244, shareholders holding not less than 10% of the issued share capital, or representing at least 100 members (whichever is less), may apply to the NCLT for relief. The Tribunal may waive this requirement in exceptional circumstances.

- Class Action Suits: Section 245 allows shareholders to file a suit collectively if they believe the management or conduct of the company is prejudicial to the interests of the company or its members.

- Right to Information: Shareholders have a right to inspect the register of members, minutes of general meetings, and financial statements to monitor the company's health.

- Contractual Rights: Minority investors often negotiate "Reserved Matters" or "Veto Rights" in their SHA, requiring their specific consent for major decisions like merging the company, changing the business line, or issuing new debt.

Shareholder Dispute Resolution Checklist and Sample Clause

To minimize the cost and duration of conflict, companies should adopt a structured approach to dispute resolution. The following checklist and sample language provide a framework for internal governance.

Pre-Litigation Checklist for Shareholders

- Audit the SHA and AoA: Verify if the Shareholders' Agreement (SHA) and Articles of Association (AoA) are aligned; in India, the AoA generally prevails in the event of a conflict unless the SHA is incorporated by reference.

- Issue a Formal Notice: Send a legal notice detailing the specific breaches and providing a "cure period" (usually 15-30 days).

- Document "Deadlock" Events: If the board is unable to pass resolutions, document the specific votes and reasons for the impasse.

- Evaluate the 10% Threshold: Confirm the petitioner meets the Section 244 eligibility criteria or prepare a waiver application.

- Assess Valuation: Engage a registered valuer to determine the fair market value of shares in case a "buy-out" is the desired outcome.

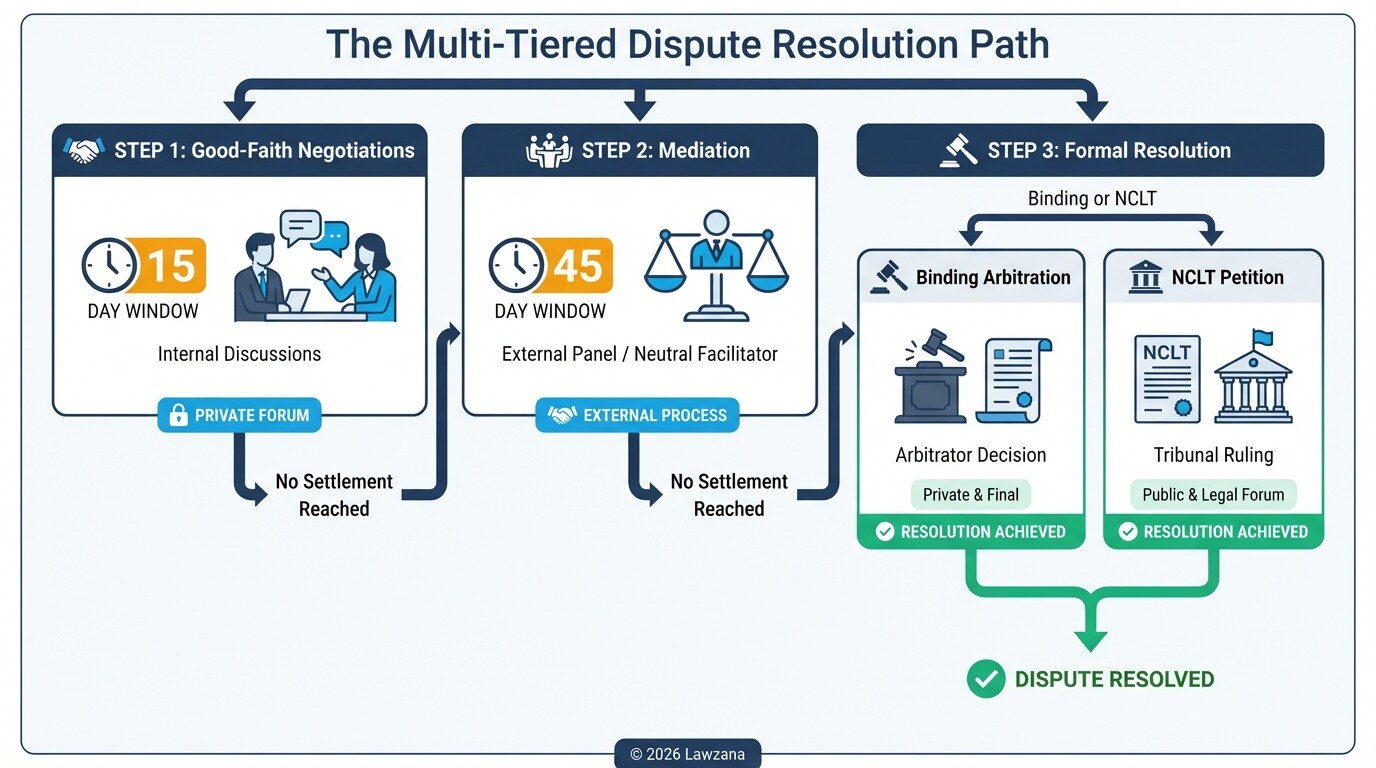

Sample Multi-Tiered Dispute Resolution Clause

"In the event of any dispute arising out of or in connection with this Agreement, the Parties shall first attempt to resolve the matter through good-faith negotiations between their respective Chief Executive Officers. If the dispute remains unresolved after fifteen (15) days, the Parties shall submit the dispute to mediation under the Companies (Mediation and Conciliation) Rules, 2016. Should mediation fail within forty-five (45) days, the dispute shall be finally settled by binding arbitration in [City, India] in accordance with the Arbitration and Conciliation Act, 1996."

Interim Reliefs Available During Ongoing Shareholder Litigation

Interim reliefs are temporary orders passed by the NCLT to preserve the "status quo" and prevent further harm while the main petition is being decided. Because Indian corporate litigation can span several years, these orders are crucial for protecting the value of the company.

Under Section 242(4), the NCLT has the power to grant several types of interim relief:

- Restraining Share Transfers: Preventing the majority from selling their stakes or issuing new shares to dilute the minority's holding.

- Stay on Board Meetings: Halting specific board meetings or the implementation of resolutions passed in contested meetings.

- Appointment of an Administrator: In cases of extreme mismanagement, the NCLT may appoint an independent person to oversee company operations.

- Protection of Assets: Restraining the company from selling, leasing, or mortgaging its immovable properties or core business assets.

- Access to Records: Directing the company to provide the aggrieved shareholder with updated financial records and minutes.

Mediation as a Tool for Resolving Boardroom Deadlocks

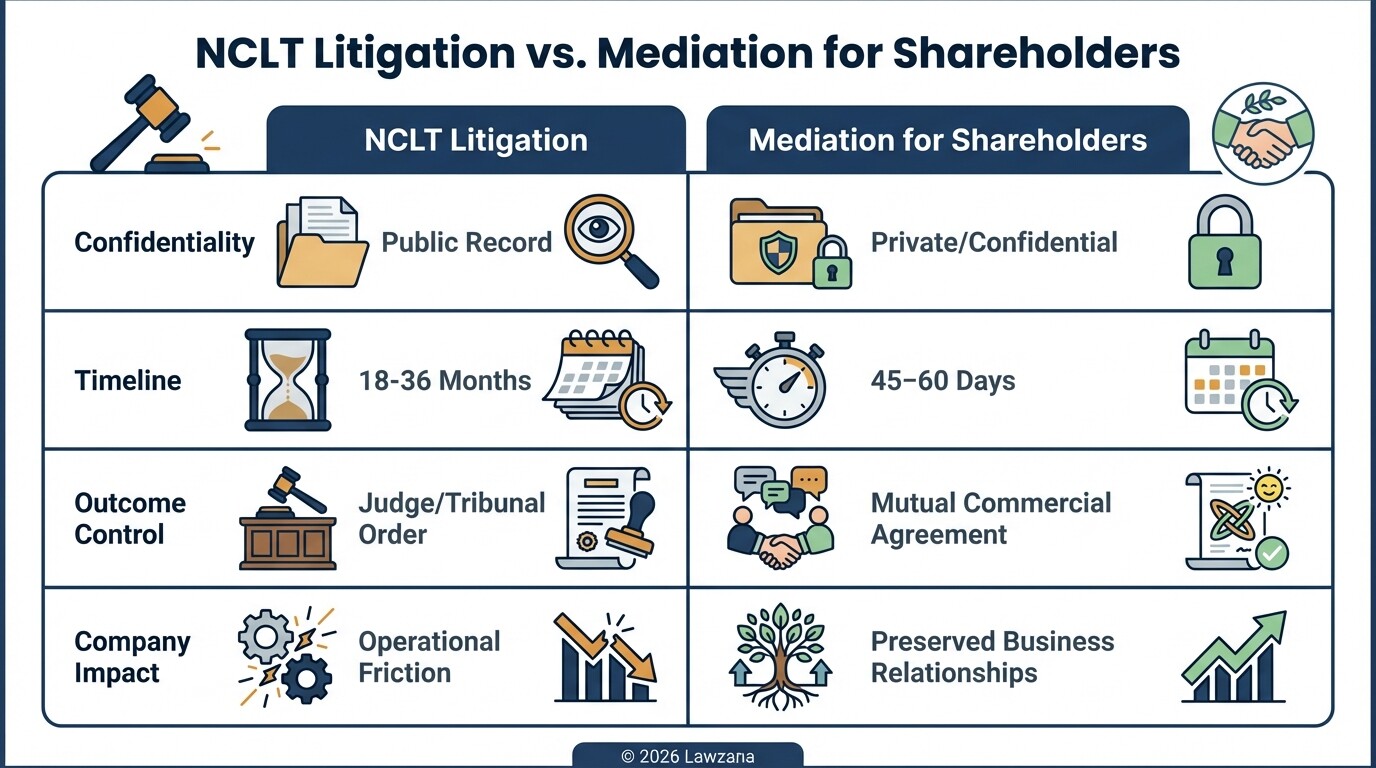

Section 442 of the Companies Act, 2013, introduced a formal mechanism for mediation and conciliation, allowing the Central Government to maintain a panel of experts to facilitate settlements. Mediation is often preferred over NCLT litigation because it is confidential, faster, and allows for "win-win" commercial settlements that a court cannot easily mandate.

- Voluntary vs. Mandatory: Parties can voluntarily agree to mediation at any stage of a dispute. Additionally, the NCLT has the power to refer a pending matter to mediation if it believes a settlement is possible.

- Confidentiality: Unlike NCLT proceedings, which are public, mediation allows directors and founders to resolve sensitive issues without damaging the company's brand or reputation.

- Creative Outcomes: While the NCLT is limited to legal remedies (like removing a director), mediation can result in creative commercial exits, such as "Russian Roulette" or "Texas Shoot-out" buy-sell arrangements.

Impact of a Shareholder Dispute on Business Operations and Funding

A shareholder dispute is often treated as a "red flag" by external stakeholders, leading to immediate operational and financial friction. In the Indian market, where trust and "promoter" stability are highly valued, a public dispute can be catastrophic.

- Freezing of Credit Lines: Banks and financial institutions often freeze working capital limits or refuse to renew credit lines once they become aware of a petition for mismanagement in the NCLT.

- Equity Funding Stall: Investors (VCs/PEs) typically include "No Litigation" warranties in their Term Sheets. An active dispute usually halts due diligence and prevents new funding rounds.

- Operational Paralysis: If the dispute leads to a boardroom deadlock, the company may be unable to approve financial statements, appoint auditors, or sign major commercial contracts, leading to a breach of statutory compliance.

- Employee Attrition: Top-tier talent often leaves companies embroiled in internal conflict, fearing for the long-term stability of their roles and equity incentives.

Common Misconceptions in Indian Shareholder Disputes

Myth: Minority shareholders can block any decision they dislike. Fact: In India, the majority rule generally prevails for day-to-day management. Unless a decision requires a Special Resolution (75% vote) or involves a "Reserved Matter" in the SHA, minority shareholders cannot block routine corporate actions unless they can prove the action is legally oppressive.

Myth: NCLT litigation is the only way to exit a company during a dispute. Fact: Most disputes are resolved through private buy-sell agreements. The NCLT itself often encourages a "parting of ways" where one group buys out the other at a fair valuation determined by a registered valuer.

FAQ

How much does it cost to file an NCLT petition in India?

The official filing fee for a petition under Section 241 is currently ₹25,000 (INR). However, total legal costs, including senior counsel fees for multiple hearings, typically range from ₹5,00,000 to several lakhs depending on the complexity and duration of the case.

How long does it take the NCLT to resolve a shareholder dispute?

While the Companies Act suggests that the NCLT should endeavor to resolve petitions within three months, the actual timeline in busy benches like Delhi or Mumbai is often 18 to 36 months due to the backlog of cases and procedural delays.

Can a shareholder be expelled from a private company?

Expulsion of a shareholder is generally not permitted unless specifically provided for in the Articles of Association and supported by valid reasons. However, the NCLT can order the compulsory purchase of a shareholder's interest as part of a final settlement in an oppression case.

What is the "Rule of Foss v. Harbottle" in India?

This classic principle suggests that for a wrong done to a company, the company itself is the proper plaintiff. However, Indian law provides exceptions (derivative actions) where shareholders can sue on behalf of the company if the wrongdoers are in control and prevent the company from taking action.

When to Hire a Lawyer

You should consult a corporate litigator if any of the following occur:

- You have been excluded from board meetings or denied access to financial information.

- The majority shareholders are attempting to dilute your stake through a rights issue you cannot afford.

- You suspect the directors are siphoning funds or selling assets without proper authorization.

- Your company is in a "deadlock" where no decisions can be made, risking a total business shutdown.

- You are an investor wanting to trigger a "forced exit" or "buy-back" due to a breach of the Shareholders' Agreement.

Next Steps

- Review Your Documents: Locate your Shareholders' Agreement and the company's Articles of Association to identify your specific rights and the agreed-upon dispute resolution process.

- Issue a Statutory Notice: Engage legal counsel to draft a formal notice to the board, which is often a prerequisite for showing that you attempted to resolve the matter internally.

- Gather Evidence: Compile bank statements, email correspondence, and board minutes that support your claim of oppression or mismanagement.

- File for Interim Relief: If the situation is urgent (e.g., an imminent asset sale), prepare to move the National Company Law Tribunal for immediate stay orders.

- Monitor Compliance: Ensure all filings with the Ministry of Corporate Affairs are up to date to prevent the company from being struck off during the litigation.