- Ireland offers a highly favorable legal framework for intellectual property holding companies, combining robust European Union protections with a competitive corporate environment.

- Establishing genuine economic substance in Ireland is mandatory to comply with OECD guidelines and benefit from local tax reliefs.

- Companies must navigate cross-border licensing carefully to ensure all intercompany agreements meet the arm's length standard for transfer pricing.

- Securing patents and trademarks through Irish and EU authorities provides a dual layer of legal protection for your global assets.

- The incorporation and asset transfer process requires strict adherence to Companies Registration Office protocols and typically takes four to eight weeks.

Corporate Law Requirements for Setting Up an Irish Holding Company

To set up an Irish intellectual property holding company, you must register a corporate entity with the Companies Registration Office, appoint at least one European Economic Area resident director, and maintain a physical registered office within the State. Most multinational corporations choose to form either a Private Company Limited by Shares (LTD) or a Designated Activity Company (DAC) to manage their intellectual property.

An LTD is the most common and flexible corporate vehicle in Ireland. It allows for a single director, does not require a stated objects clause, and can be incorporated quickly. A DAC requires at least two directors and is bound by a specific memorandum of association, which some corporate groups prefer for strictly defining the holding company's purpose.

Regardless of the entity type, your company must meet the following baseline legal requirements:

- EEA Resident Director: At least one director must reside in the European Economic Area. If this is not possible, the company must secure a Section 137 Non-Resident Director Bond.

- Company Secretary: Every Irish company must appoint a qualified company secretary to manage statutory compliance and filings.

- Registered Office: The company must have a physical address in Ireland where official documents can be delivered. A simple post office box is not legally sufficient.

- Statutory Filings: Annual returns and financial statements must be filed on time with the Companies Registration Office to maintain the company's legal standing.

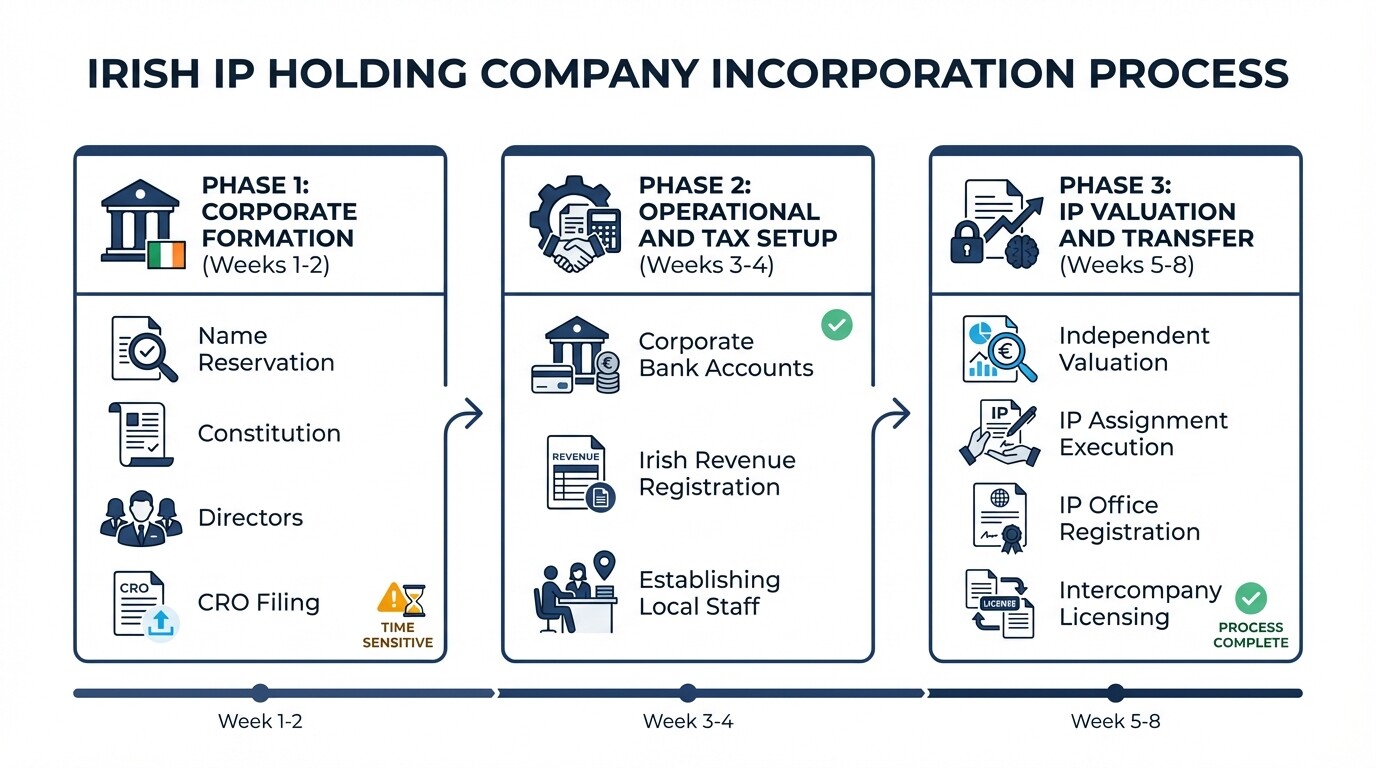

Checklist and Timeline for Incorporation and IP Asset Transfer

Incorporating an Irish IP holding company and transferring assets typically takes four to eight weeks, depending on the complexity of the IP valuation and corporate structuring. Use this checklist to track the critical milestones of your setup phase and ensure no regulatory requirements are missed.

Phase 1: Corporate Formation (Weeks 1 to 2)

- Reserve the proposed company name with the Companies Registration Office.

- Draft the company constitution, tailored to either an LTD or a DAC structure.

- Appoint directors, the company secretary, and establish the registered office.

- Execute incorporation documents and file them with the Companies Registration Office.

Phase 2: Operational and Tax Setup (Weeks 3 to 4)

- Open an Irish corporate bank account to facilitate future royalty payments.

- Register for Corporation Tax, Value Added Tax (VAT), and employer taxes with Irish Revenue.

- Hire local staff or establish a localized board of directors to begin building economic substance.

Phase 3: IP Valuation and Transfer (Weeks 5 to 8)

- Conduct an independent valuation of the intellectual property assets being transferred.

- Draft and execute IP Assignment Agreements to legally move the assets to the Irish entity.

- Register the transfer of ownership with relevant national and international IP offices.

- Execute intercompany licensing agreements with foreign subsidiaries.

Compliance With International Tax Standards and Substance Requirements

Irish IP holding companies must demonstrate genuine economic substance and comply with the OECD Base Erosion and Profit Shifting framework to legally access tax benefits. Shell companies without local operations or decision-making capabilities will face severe regulatory penalties and the denial of international tax treaty benefits.

To satisfy substance requirements, the Irish holding company must actively manage and control the intellectual property from within Ireland. Tax authorities will look at where the strategic decisions are made and where the financial risks are borne.

Key strategies for demonstrating economic substance include:

- Local Decision Making: Board meetings must be held physically in Ireland, with a quorum of directors present who possess the expertise to manage IP assets.

- Qualified Personnel: The company should employ local staff who actively participate in research, development, or the commercial management of the intellectual property.

- Financial Risk Management: The Irish entity must hold sufficient capital to bear the financial risks associated with developing, maintaining, and defending the IP.

- The Knowledge Development Box: Companies that perform active research and development in Ireland or the EU may qualify for the Knowledge Development Box. This initiative reduces the standard 12.5% corporation tax rate to 6.25% on qualifying profits generated from patents and copyrighted software.

Navigating Cross-Border IP Licensing Agreements

Cross-border licensing agreements must be drafted at an arm's length standard to satisfy global transfer pricing regulations and avoid audits from international tax authorities. These agreements dictate exactly how the Irish holding company grants usage rights to foreign subsidiaries while collecting royalty payments in return.

Under Irish law and OECD guidelines, the royalties charged by the Irish holding company to its international subsidiaries must match what would be charged to an independent third party. Failure to accurately price these licenses can lead to double taxation and significant financial penalties.

A compliant intercompany licensing agreement should strictly define:

- Scope of Rights: Clear parameters on which subsidiaries can use the IP, geographical limitations, and whether the license is exclusive or non-exclusive.

- Royalty Rates: A detailed pricing mechanism supported by an independent transfer pricing study to prove the arm's length nature of the transaction.

- Withholding Tax Provisions: Clauses addressing how withholding taxes are managed under Ireland's extensive network of double taxation treaties.

- Dispute Resolution: Mechanisms for resolving internal commercial disputes, often defaulting to arbitration in a neutral European jurisdiction.

Protecting Patents and Trademarks Under Irish and EU Law

Ireland provides a dual layer of IP protection through national registration with the Intellectual Property Office of Ireland and pan-European coverage via European Union institutions. Securing these rights ensures your holding company has legally defensible assets that can be safely licensed across the globe.

Registering your assets properly is the foundation of a holding company's value. Without registered protection, the company has no underlying legal right to demand royalty payments or prevent infringement by competitors.

- Trademarks: You can register a national trademark with the Intellectual Property Office of Ireland for local protection. For broader coverage, registering a European Union Trade Mark with the EUIPO provides protection across all member states through a single application.

- Patents: Irish patents require a formal application detailing the invention's novelty and industrial applicability. For multinational strategies, the holding company can apply for a European Patent to secure rights across multiple European countries simultaneously.

- Copyrights: Under Irish law, copyright protection applies automatically to original literary, dramatic, musical, and artistic works, including software code. No formal registration is required, but maintaining clear records of creation and assignment to the holding company is vital for enforcement.

Common Misconceptions About Irish IP Holding Companies

Multinational executives often misunderstand the regulatory demands of operating an IP holding company in Ireland, leading to compliance failures and unexpected tax liabilities. Clarifying these operational myths is vital for creating a secure corporate structure.

- A simple mailbox address is enough to claim Irish residency. Many businesses assume that renting a registered address is sufficient to establish a holding company. In reality, modern tax laws require demonstrable economic substance, meaning the company needs actual operational presence, competent local directors, and strategic decision-making happening within Ireland.

- All intellectual property qualifies for the 6.25% tax rate. The Knowledge Development Box offers a highly reduced tax rate, but it is not a blanket reduction for all IP. It applies only to specific assets, such as qualifying patents and copyrighted software, and requires the company to have incurred the research and development costs directly.

- Transferring IP is just a matter of changing the owner's name. Moving high-value intellectual property into an Irish entity requires independent valuation and formalized legal assignment. Transferring IP at an artificial value to avoid capital gains taxes in the origin country will trigger aggressive audits from foreign tax authorities.

Frequently Asked Questions

Do I need to live in Ireland to act as a director?

You do not need to live in Ireland, but your company must have at least one director who is a resident of the European Economic Area. If no directors reside in the EEA, the company must purchase a non-resident director bond to satisfy corporate law requirements.

How much does it cost to register an LTD in Ireland?

The mandatory filing fee with the Companies Registration Office is EUR 50 for online applications. However, professional legal and advisory fees for drafting custom constitutions, advising on board structures, and executing IP assignments will significantly increase the total setup cost.

Can I transfer existing IP to a newly formed Irish holding company?

Yes, you can transfer existing intellectual property to an Irish holding company. The transfer must be done via a formal IP Assignment Agreement, and the assets must be transferred at fair market value to comply with international transfer pricing rules.

What happens if my holding company lacks economic substance?

If tax authorities determine your company is a shell entity lacking substance, they can deny you the benefits of Ireland's double taxation treaties. This often results in heavy withholding taxes applied by the countries where your subsidiaries operate.

When to Hire a Lawyer and Next Steps

Engaging legal counsel is strictly necessary before transferring high-value intellectual property assets or finalizing your corporate structure in Ireland. A specialized lawyer ensures your holding company meets the demanding economic substance requirements and complies with complex global transfer pricing rules.

If you are planning to centralize your global IP operations in Ireland, your first step is to conduct an audit of your existing assets and their current ownership structures. Next, consult with a legal professional to design a corporate entity that aligns with both your commercial goals and OECD tax guidelines. You can easily find a corporate and commercial lawyer in Ireland to guide you through the incorporation, valuation, and asset transfer process safely.