Structuring an Irish Holding Company for Multinational Tech Firms

- Optimal Corporate Structure: The Private Company Limited by Shares (LTD) is the standard vehicle for tech firms entering Europe, limiting shareholder liability and simplifying equity management.

- Director Residency Rules: Irish law mandates at least one company director must reside in the European Economic Area (EEA), or the company must secure a non-resident director bond.

- IP Tax Advantages: Transferring Intellectual Property (IP) to an Irish entity allows firms to utilize the Knowledge Development Box (KDB), potentially reducing the tax rate on qualifying IP income to 6.25%.

- EU VAT Simplification: Registering for the EU One Stop Shop (OSS) in Ireland allows digital service providers to manage cross-border VAT obligations across the entire European Union through a single return.

- Strict Annual Compliance: Failure to file annual returns with the Companies Registration Office (CRO) automatically revokes audit exemptions and triggers harsh financial penalties.

Why Choose an Irish Private Company Limited by Shares (LTD)

The Private Company Limited by Shares (LTD) is the most efficient and legally protected corporate structure for multinational tech firms entering the European Union. It limits shareholder liability to their unpaid share capital, allows for a single director, and accommodates seamless future equity structuring.

For tech companies focused on rapid scaling and potential acquisition, the LTD model provides the ideal balance of legal protection and operational flexibility. Unlike older corporate forms, an LTD does not require a stated authorized share capital, and it holds full legal capacity to undertake any lawful business without being restricted by an objects clause. Furthermore, Ireland offers a highly attractive 12.5% corporate tax rate on active trading income, which remains one of the most competitive in the developed world.

To evaluate your options, compare the standard LTD against the Designated Activity Company (DAC), which is sometimes required for joint ventures or specific financial structures:

| Feature | Private Company Limited by Shares (LTD) | Designated Activity Company (DAC) |

|---|---|---|

| Director Requirements | Minimum of one director | Minimum of two directors |

| Objects Clause | No objects clause; unrestricted activity | Required; activities limited by constitution |

| Name Suffix | Must end in "Limited" or "Teoranta" | Must end in "DAC" |

| AGM Requirement | Can be waived by written resolution | Required, unless it is a single-member DAC |

| Best Used For | General tech operations, holding companies, software sales | Joint ventures, highly regulated financial entities |

Irish Holding Company Setup Checklist

Registering an Irish holding company requires specific sequential steps, from reserving a name to securing tax registrations. Following this exact sequence prevents application rejections from the Companies Registration Office (CRO) and ensures rapid market entry.

Execute these steps in order to legally establish your corporate entity:

- Name Search and Reservation: Verify the availability of your proposed company name against the CRO database. The name must be distinctly different from existing Irish entities.

- Draft the Constitution: Prepare a single-document constitution. For an LTD, this is a streamlined document that replaces the traditional Memorandum and Articles of Association.

- Establish a Registered Office: Secure a physical address within the Republic of Ireland. This must be a physical location where legal documents can be delivered, not a P.O. Box.

- Appoint Officers: Nominate at least one director and a distinct company secretary. If you only have one director, a separate person or corporate entity must serve as the secretary.

- File Form A1 with the CRO: Submit the incorporation application detailing initial share capital, registered office, and officer details.

- Register the Beneficial Owners: Within five months of incorporation, register the ultimate beneficial owners (holding 25% or more shares) with the Register of Beneficial Ownership (RBO).

- Complete Tax Registration: Apply to the Irish Revenue Commissioners for Corporation Tax, Employer PAYE, and EU VAT registrations.

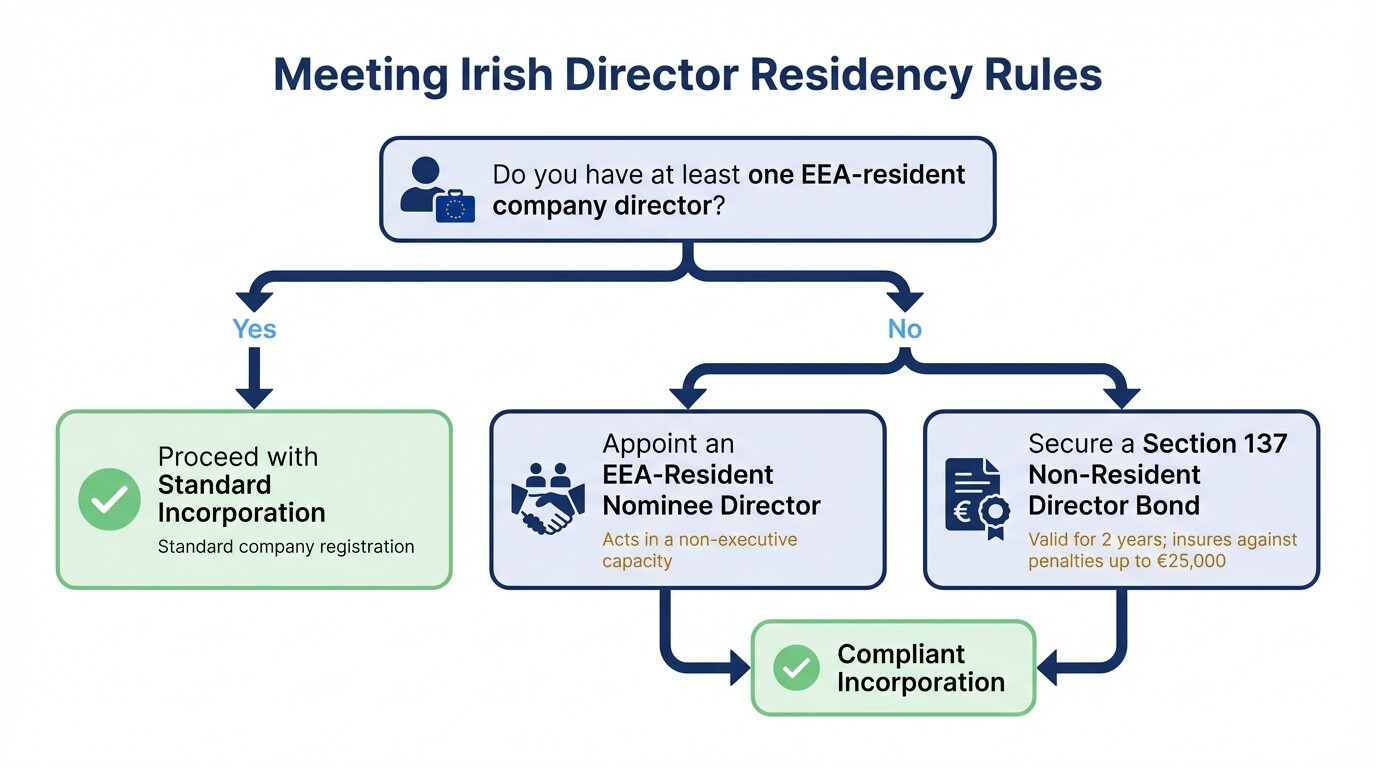

Meeting Director Residency Requirements in Ireland

Irish company law mandates that at least one director of your holding company must be a resident of the European Economic Area (EEA). If your multinational tech firm only has directors based in the US or outside the EEA, you must either appoint a nominee director or secure a non-resident director bond.

According to Section 137 of the Companies Act 2014, failure to meet this requirement prevents the incorporation of the company. A Section 137 Non-Resident Director Bond is a practical solution for US tech founders. This insurance bond guarantees the payment of a fine or penalty (up to €25,000) if the company fails to comply with company or tax laws. The bond must be valid for two years and generally costs around €1,000 to €1,500.

Alternatively, multinational firms often utilize corporate service providers to appoint an EEA-resident nominee director. The nominee acts in a non-executive capacity, satisfying legal residency requirements while executing decisions directed by the US parent company via strict legal indemnities and shareholder agreements.

Structuring IP for the Knowledge Development Box

To benefit from Ireland's Knowledge Development Box (KDB), multinational firms must legally assign their qualifying Intellectual Property to the Irish entity and demonstrate substantial research and development activity within the EU. The KDB effectively cuts the corporate tax rate on qualifying IP income in half, establishing an effective rate of 6.25%.

Qualifying assets generally include computer programs, patented inventions, and supplementary protection certificates. Brand names, trademarks, and mere image rights do not qualify. To legally structure this, the multinational parent must execute a formal Intellectual Property Assignment or Licensing Agreement transferring the economic rights of the software or patent to the Irish LTD.

The tax relief is calculated using the OECD's "nexus approach." This means the tax benefit is directly tied to the proportion of R&D expenditures incurred by the Irish company itself. Simply holding IP in Ireland without localized development efforts or economic substance will not unlock the KDB benefits.

EU VAT Registration and Digital Services Invoicing

Irish holding companies providing digital services across the EU must register for Value-Added Tax (VAT) and issue invoices according to strict cross-border regulations. Utilizing the EU VAT One Stop Shop (OSS) simplifies this process by allowing you to file a single VAT return in Ireland for all EU consumer sales.

For Business-to-Consumer (B2C) digital sales, software and SaaS companies must charge the VAT rate applicable to the consumer's home country. Registering for the OSS through the Irish Revenue Commissioners prevents the need to register for VAT in every individual EU member state.

For Business-to-Business (B2B) cross-border sales within the EU, the "reverse charge" mechanism applies. You do not charge VAT on your invoice; instead, the business customer accounts for the VAT in their own jurisdiction. Your invoices must legally include:

- Your Irish VAT registration number.

- The customer's EU VAT number.

- The exact phrasing: "Reverse Charge applies - Customer to account for VAT."

Annual CRO Compliance and Corporate Governance

Your Irish holding company must submit an Annual Return to the Companies Registration Office (CRO) every year to remain in good standing and avoid severe penalties. Missing the annual return deadline automatically revokes your audit exemption for two years and incurs immediate late filing fees.

The first Annual Return is due exactly six months after the date of incorporation, and this initial filing does not require financial statements to be attached. However, every subsequent Annual Return must include abridged or full financial statements compliant with Irish Generally Accepted Accounting Practice (GAAP) or IFRS.

Failure to maintain compliance does not just result in financial penalties. The CRO actively pursues involuntary strike-offs for non-compliant companies. If your company is struck off, its assets-including valuable intellectual property and bank accounts-become the property of the Irish State until formally restored by the High Court.

Common Misconceptions About Irish Holding Companies

Multinational founders often misunderstand the operational requirements of establishing an Irish entity, leading to compliance failures and unexpected tax liabilities. A mere "paper company" without actual economic substance will not qualify for Ireland's advantageous corporate frameworks.

- Misconception: A virtual office constitutes Irish residency. Establishing tax residency in Ireland requires "mind and management" to occur within the State. Holding board meetings locally and having qualified personnel on the ground is necessary to access the 12.5% trading rate.

- Misconception: US employment contracts can be used for Irish staff. Irish employment law heavily favors the employee compared to "at-will" US states. Multinational firms must draft localized employment contracts that comply with Irish statutory leave, notice periods, and termination procedures.

Frequently Asked Questions

How long does it take to register a company in Ireland?

Standard company registration through the CRO typically takes 3 to 5 business days once all correctly signed documents, including Form A1 and the constitution, are submitted. Delays usually occur when non-EEA directors require a Section 137 bond prior to submission.

Can a US citizen or foreign entity own 100% of an Irish company?

Yes, there are no restrictions on foreign ownership of an Irish company. A US corporation or individual can own 100% of the shares in an Irish Private Company Limited by Shares (LTD).

Do I need to travel to Ireland to set up the holding company?

No, you do not need to physically travel to Ireland. The entire incorporation process, including executing documents and setting up nominee directors or bonds, can be handled remotely through digital signatures and corporate service providers.

What is the Corporation Tax rate for an Irish holding company?

The standard rate is 12.5% for active trading income. Passive income (such as non-trading royalties or rental income) is taxed at 25%, while qualifying R&D software income can drop to 6.25% under the Knowledge Development Box.

When to Hire an Irish Corporate Lawyer

Retaining an Irish corporate lawyer is essential when structuring cross-border intellectual property transfers or managing complex equity agreements between international parent companies. Do not rely on generic templates, as Irish corporate and tax laws strictly govern how assets must be localized and how intercompany agreements are framed. You will need specialized counsel to draft IP assignments, navigate transfer pricing rules, and ensure your corporate constitution properly reflects the US parent company's governance requirements. To find verified legal experts for your expansion, explore business registration lawyers in Ireland.

Next Steps

Taking action requires securing your legal foundation before initiating commercial operations or transferring software rights to Europe. Begin by assessing your director residency options-whether appointing an EEA resident or securing a Section 137 bond. Once leadership is mapped out, engage a corporate service provider or attorney to draft your Irish constitution and submit your registration to the CRO. Immediately after incorporation, prioritize opening an Irish corporate bank account and registering for EU VAT to ensure seamless digital sales.