Key Takeaways

Expanding a multinational corporation into India requires choosing the right legal structure to align with your strategic goals. The decision between a Wholly Owned Subsidiary (WOS) and a Branch Office (BO) dictates your tax rates, permitted business activities, and overall legal liability.

- A Wholly Owned Subsidiary is treated as a domestic company, allowing for comprehensive operations including manufacturing and trading.

- A Branch Office is an extension of the foreign parent company and is strictly prohibited from engaging in manufacturing activities.

- The Reserve Bank of India (RBI) mandates a stringent approval process for a Branch Office, whereas a Subsidiary often benefits from the automatic Foreign Direct Investment (FDI) route.

- A Subsidiary limits the legal liability to the Indian entity, while a Branch Office exposes the foreign parent company to all local liabilities.

- Incorporating a Subsidiary takes roughly 4 to 6 weeks, while a Branch Office setup can extend up to 8 weeks.

Structural Comparison: WOS vs Branch Office

A Wholly Owned Subsidiary operates as an independent Indian company with its own legal identity, protecting the foreign parent company from liability. In contrast, a Branch Office is a mere extension of the foreign parent, meaning the parent company assumes all legal and financial liabilities incurred in India.

Choosing between these structures heavily impacts your operational scope and financial obligations. The table below outlines the primary structural differences multinational companies face when entering the Indian market.

| Feature | Wholly Owned Subsidiary (WOS) | Branch Office (BO) |

|---|---|---|

| Legal Status | Independent legal entity registered under the Companies Act, 2013. | Extension of the foreign parent company; not a separate legal entity. |

| Liability | Limited to the share capital invested in the Indian entity. | Unlimited. The foreign parent company is fully liable for Indian operations. |

| Tax Implications | Taxed as a domestic company. Base corporate tax is generally 22% to 25% (plus applicable surcharge and cess). | Taxed as a foreign company. Base corporate tax is 40% (plus applicable surcharge and cess). |

| Permitted Activities | Can engage in any legal business activity, including manufacturing, trading, and services. | Restricted to specific activities like export/import, research, and technical support. |

| Funding Sources | Equity, debt, and internal accruals. | Entirely funded by the foreign parent company through inward remittances. |

Common Misconceptions About Indian Market Entry

Foreign investors often misunderstand the regulatory limits placed on different corporate structures in India. Correcting these assumptions early prevents costly compliance violations and operational delays.

- Using a Branch Office for manufacturing: This is a critical mistake. Foreign Direct Investment (FDI) policies strictly prohibit Branch Offices from engaging in direct manufacturing or processing activities. Attempting to manufacture through a BO will halt production and trigger severe penalties from regulatory authorities.

- Assuming a Branch Office is faster to set up: Many executives believe that because a BO is not a separate entity, it bypasses bureaucracy. In reality, the mandatory RBI scrutiny required for a Branch Office makes the process longer than registering a subsidiary.

- Treating tax liability identically: Multinationals often assume their Indian operations will be taxed uniformly regardless of structure. However, because India taxes Branch Offices as foreign entities, they face a significantly higher corporate tax rate than domestic subsidiaries.

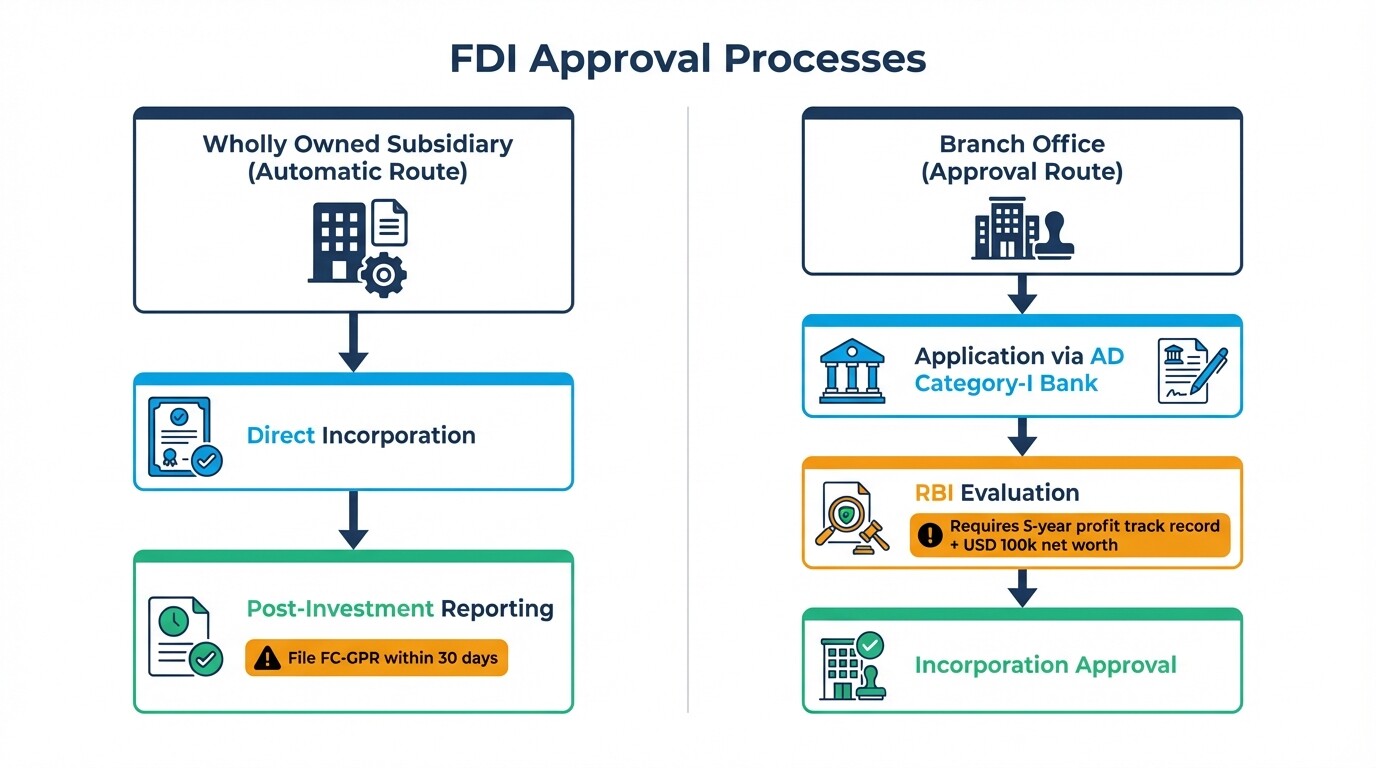

Navigating RBI Approval Under the Foreign Exchange Management Act

Establishing a Branch Office requires explicit approval from the Reserve Bank of India (RBI) under the Foreign Exchange Management Act (FEMA). A Wholly Owned Subsidiary typically benefits from the automatic route for Foreign Direct Investment (FDI), bypassing the need for prior RBI clearance in most sectors.

For a Branch Office, the foreign entity must route its application through a designated Authorized Dealer (AD) Category-I bank. The RBI evaluates the application based on the parent company's financial track record. Specifically, the foreign entity must demonstrate a profitable track record during the immediately preceding five years in its home country and possess a net worth of at least USD 100,000.

Conversely, setting up a WOS under the automatic FDI route only requires post-investment reporting to the RBI. You must file the Foreign Currency Gross Provisional Return (FC-GPR) form within 30 days of issuing shares to the foreign parent company, detailing the inward remittance of capital.

Expected Timelines for Setup

Setting up a Wholly Owned Subsidiary typically takes 4 to 6 weeks, provided all foreign documents are properly notarized and apostilled. A Branch Office usually takes up to 8 weeks due to the mandatory RBI approval process.

The timeline for a Subsidiary largely depends on document preparation in the foreign parent's home country. Drafting, notarizing, and apostilling Board Resolutions, the Memorandum of Association (MOA), and the Articles of Association (AOA) often take 2 to 3 weeks. Once these documents are filed with the Ministry of Corporate Affairs in India, the actual incorporation process is completed within 7 to 10 business days.

A Branch Office requires the same home-country document preparation, but the application must then sit with the Authorized Dealer bank and the RBI for review. This multi-tiered scrutiny adds at least 3 to 4 weeks to the overall timeline, pushing the total setup period to 8 weeks or more.

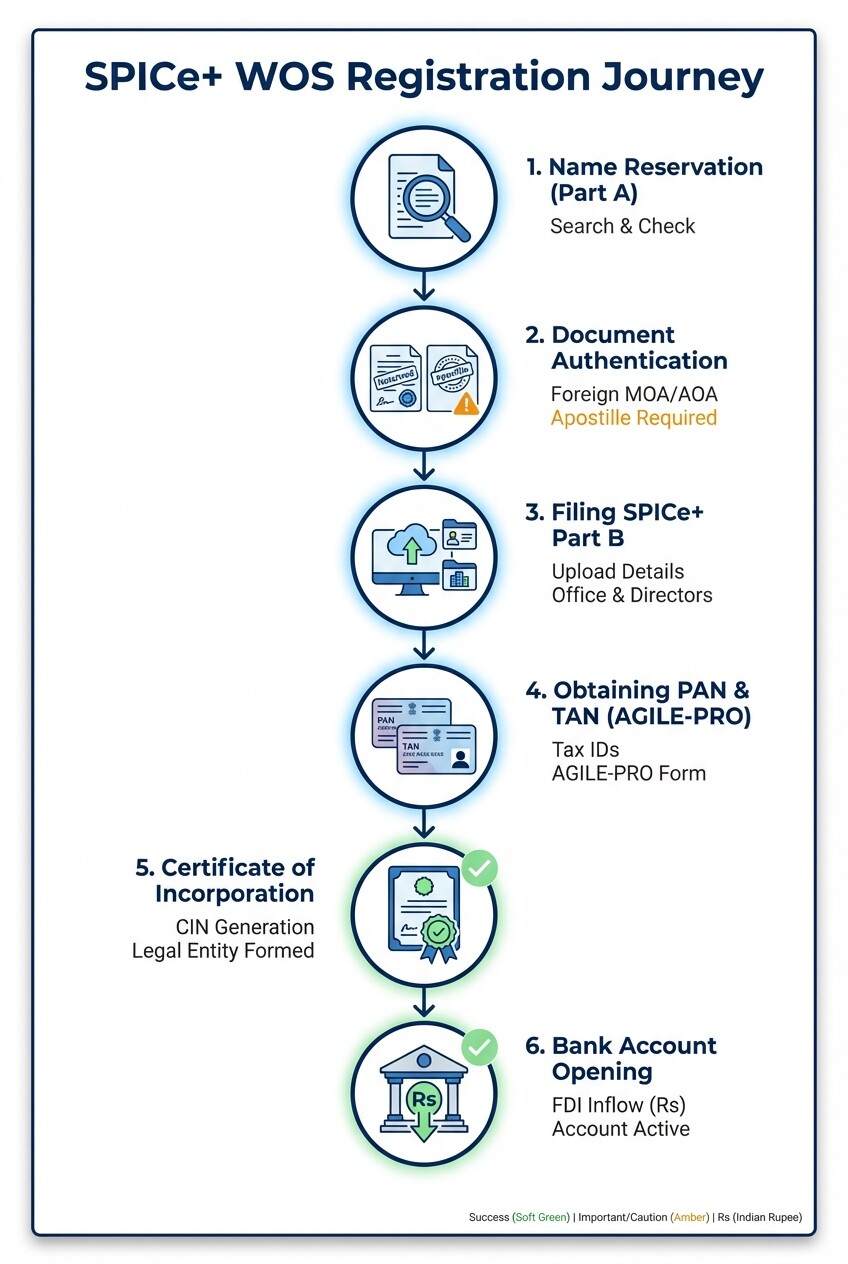

Step-by-Step SPICe+ Registration for a WOS

The Ministry of Corporate Affairs manages company registration through the SPICe+ web form, which consolidates multiple registration processes into a single application. This unified form grants your Certificate of Incorporation, Director Identification Numbers (DIN), and mandatory tax registrations for the foreign entity.

Follow these steps to register a Wholly Owned Subsidiary using SPICe+:

- Name Reservation (SPICe+ Part A): Submit two proposed names for the Indian subsidiary. If the name includes the foreign parent company's trademark, attach a No Objection Certificate (NOC) and board resolution from the parent company authorizing the use of the name.

- Document Authentication: The foreign parent company must draft the MOA and AOA. Because the subscribers are foreign entities, these documents, along with the identity and address proofs of the foreign directors, must be notarized and apostilled in the home country.

- Filing SPICe+ Part B: Upload the apostilled documents and fill in the incorporation details. This section covers the registered office address, authorized share capital, and director appointments.

- Obtaining PAN and TAN (AGILE-PRO): As part of the SPICe+ filing, you must submit forms for the Permanent Account Number (PAN) and Tax Deduction and Collection Account Number (TAN). The apostilled passport and address proof of the authorized foreign director serve as the basis for generating these tax identities.

- Certificate of Incorporation: Once the Ministry approves the SPICe+ forms, you will receive a digital Certificate of Incorporation containing the company's Corporate Identification Number (CIN), PAN, and TAN.

- Bank Account Opening: Use the Certificate of Incorporation and SPICe+ AGILE-PRO integration to open a corporate bank account. The foreign parent must then remit the subscription money into this account to comply with FDI regulations.

Frequently Asked Questions

Foreign corporations evaluating market entry structures must resolve specific regulatory queries early in the process. The answers below address the most common compliance and operational questions regarding Indian subsidiaries and branch offices.

Can a Branch Office acquire property in India?

A Branch Office can acquire immovable property in India provided it is strictly used for carrying out its permitted business activities. However, entities from certain neighboring countries require prior approval from the RBI to purchase real estate.

Does a Wholly Owned Subsidiary require a resident Indian director?

Yes. Under the Companies Act, 2013, every Indian company must have at least one director who has stayed in India for a minimum of 182 days during the current calendar year. The other directors can be foreign nationals.

Can a foreign entity hold 100 percent of the shares in a WOS?

Yes, a foreign entity can hold 100 percent of the shares, provided the business operates in a sector where 100 percent Foreign Direct Investment is permitted under the automatic route. A minimum of two shareholders is required to form a private limited company, so the parent company typically holds 99.9 percent, with one share held by a nominee to satisfy the legal requirement.

When to Hire a Business Registration Lawyer

Navigating India's complex Foreign Direct Investment framework and company laws requires specialized legal counsel. A local attorney ensures your entry structure aligns with your operational goals without triggering regulatory penalties.

Attempting to manage the SPICe+ filing or RBI approvals without local expertise often leads to rejected applications due to incorrectly formatted or improperly apostilled foreign documents. Partnering with experienced business registration lawyers in India helps you structure your subsidiary's share capital, draft compliant MOAs, and ensure swift communication with Authorized Dealer banks during FEMA reporting.

Next Steps

Entering the Indian market requires careful planning and precise execution of statutory requirements. Begin by finalizing your business activities to determine which legal structure best supports your strategic objectives.

- Consult with a corporate tax advisor to model the financial impact of the 40 percent Branch Office tax rate versus the domestic Subsidiary tax rate.

- Identify a suitable local resident to serve as your mandatory Indian director if you proceed with a Wholly Owned Subsidiary.

- Begin gathering and apostilling the required corporate documents from your parent company, as international notarization is often the most time-consuming phase of the setup process.