Insolvency Options for Foreign-Owned Subsidiaries in Italy

- The Italian Crisis and Insolvency Code (CCII) requires subsidiary directors to implement early warning systems to avoid personal liability.

- Out-of-court restructuring through a Negotiated Settlement lets distressed businesses avoid formal bankruptcy.

- Filing for a Negotiated Settlement can provide up to 240 days of protection against local creditor actions.

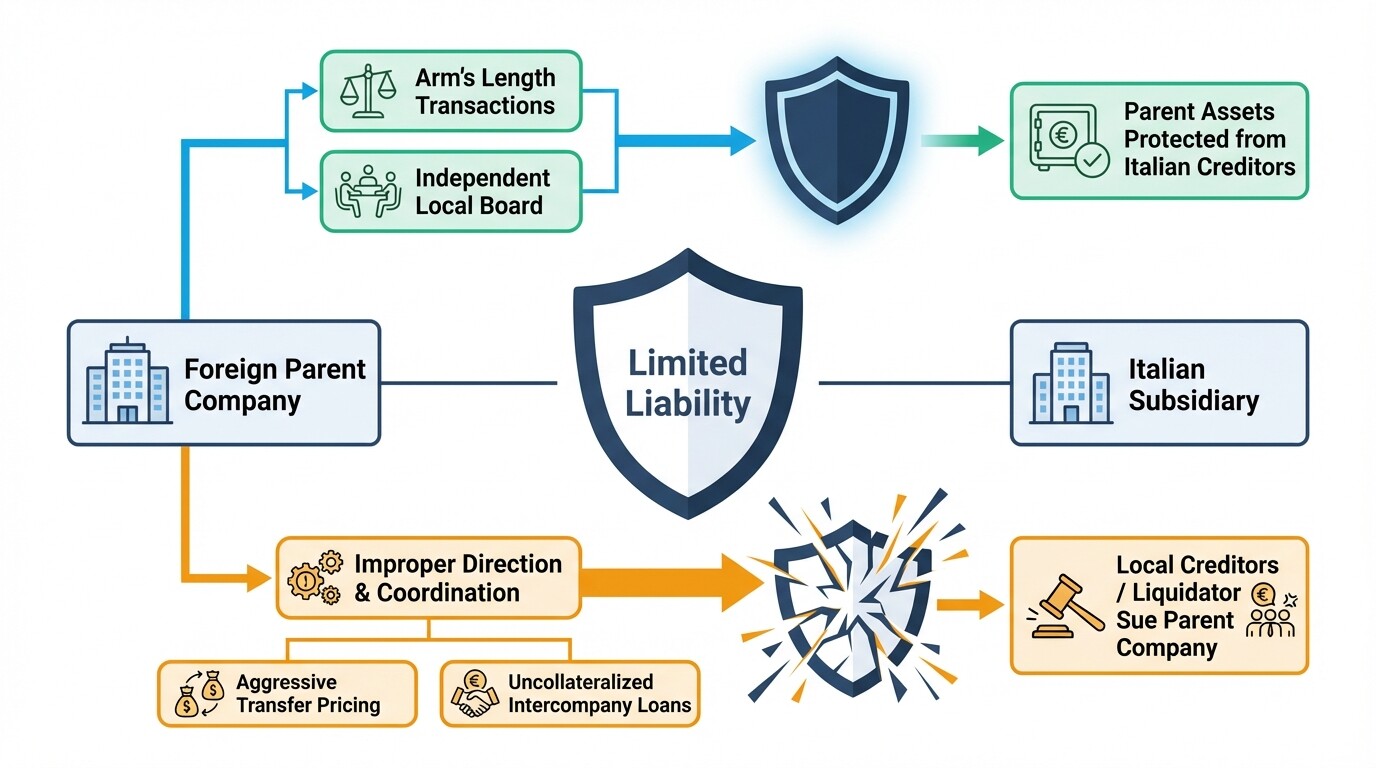

- Limited liability shields foreign parent companies from an Italian subsidiary's debts, unless the parent engaged in improper "direction and coordination."

- Voluntary liquidation is an option only if the Italian subsidiary has enough assets to pay all existing creditors.

Early Warning Mechanisms and Directors' Duties in Italy

Under the Italian Crisis and Insolvency Code (CCII), directors of an Italian subsidiary must implement early warning systems to detect financial distress. Failing to maintain these frameworks exposes local directors to personal liability if the company enters judicial liquidation.

Article 2086 of the Italian Civil Code requires corporate enterprises to establish administrative and accounting structures that detect crises early. Directors must monitor financial indicators like payroll arrears, unpaid VAT, and delayed social security contributions. If these indicators trigger a warning, directors must pursue restructuring options immediately. Statutory auditors (sindaci) must report the board of directors if the board ignores these financial warnings.

Negotiated Settlement vs. Judicial Liquidation

Italian law offers two primary paths for insolvent entities: the voluntary Negotiated Settlement (composizione negoziata della crisi) and Judicial Liquidation (liquidazione giudiziale). A negotiated settlement lets the subsidiary continue operations while restructuring debt out of court. Judicial liquidation places a court-appointed official in control to dissolve the business.

The appropriate path depends on the subsidiary's financial health and the foreign parent's strategy in Italy.

| Feature | Negotiated Settlement | Judicial Liquidation |

|---|---|---|

| Objective | Business continuity and debt restructuring | Asset liquidation and market exit |

| Control | Directors retain control | Court-appointed liquidator takes full control |

| Process Type | Out-of-court, confidential | Public, court-driven |

| Expert Involvement | Independent expert appointed by the Chamber of Commerce | Judge and official liquidator |

| Duration | 6 to 12 months | 3 to 5 years or more |

Timelines for Protecting Assets from Local Creditors

When filing for a Negotiated Settlement, the Italian subsidiary can request immediate protective measures (misure protettive) to pause creditor actions. The local court can grant an initial stay of up to 120 days. This stay can be extended to a maximum of 240 days.

To activate this protection, the subsidiary must file a request with its application on the official Negotiated Settlement platform managed by the Italian Chambers of Commerce. Once the judge approves the measures, creditors cannot initiate or continue enforcement actions, foreclosures, or file petitions for judicial liquidation. During this 120 to 240-day window, the local directors can negotiate debt write-downs or secure new financing without facing sudden asset seizures.

Cross-Border Implications for Foreign Parent Company Liability

Limited liability generally protects foreign parent companies. Italian creditors cannot access the parent's global assets to satisfy the subsidiary's debts. However, courts can pierce this corporate veil if the parent exercised improper "direction and coordination" (direzione e coordinamento) that disadvantaged the Italian subsidiary.

Under Italian corporate law, a holding company that dictates the operational and financial decisions of a subsidiary assumes specific legal responsibilities. If the foreign parent forces the Italian entity into transactions that drain its resources, such as aggressive transfer pricing or uncollateralized intercompany loans, local creditors or the liquidator can sue the parent company for damages. Foreign parent companies minimize this risk by conducting all transactions with the Italian subsidiary at arm's length and allowing the local board independent decision-making authority.

Steps for Orderly Liquidation of an Italian Subsidiary

Winding down a solvent Italian subsidiary requires a formal voluntary liquidation procedure (liquidazione volontaria). This process ensures all local creditors, employees, and tax authorities receive payment before the entity is struck from the Italian Companies Register.

The statutory steps to close an Italian entity include:

- Convene an extraordinary shareholders' meeting: The foreign parent passes a resolution before an Italian Notary Public to place the company into liquidation.

- Appoint a liquidator: Shareholders appoint one or more liquidators to replace the board of directors and assume control of winding down the business.

- Settle outstanding debts: The liquidator sells corporate assets, collects outstanding receivables, and pays all existing creditors. Voluntary liquidation cannot proceed if the company cannot pay its debts in full.

- Draft the final liquidation balance sheet: After liquidating assets and paying debts, the liquidator prepares a final balance sheet and a distribution plan for any remaining capital.

- File for deregistration: Following a mandatory 90-day waiting period for creditor objections, the liquidator files to strike the company from the Italian Companies Register (Registro delle Imprese), dissolving the entity.

Common Misconceptions About Italian Insolvency

Foreign stakeholders often assume Italian insolvency proceedings are highly punitive or entirely dictated by the courts. Recent legislative reforms instead prioritize business rescue and private, out-of-court settlements.

A frequent misconception is that an insolvent subsidiary automatically triggers a criminal bankruptcy investigation (bancarotta fraudolenta). Italian law penalizes fraudulent asset hiding and false accounting, but directors who use the CCII's early warning mechanisms and file for restructuring on time avoid criminal liability.

Another myth is that insolvency proceedings in Italy take decades to resolve. Historical bankruptcy cases were slow, but the Negotiated Settlement framework forces a resolution or restructuring agreement within a 6 to 12-month timeframe.

When to Hire an Italian Insolvency Lawyer

Engage an Italian insolvency attorney when your subsidiary's cash flow projections show an inability to meet debt obligations over the next 12 months. Local counsel is necessary to navigate the strict timelines of the CCII, activate protective measures, and shield foreign directors from liability.

Attempting to resolve financial distress without local representation often leads to missed statutory deadlines, which strips the subsidiary of its right to out-of-court restructuring. You can connect with restructuring and insolvency lawyers in Italy to assess your subsidiary's financial exposure and outline a compliant strategy.

Next Steps for Foreign Holding Companies

Commission an independent financial audit of the Italian subsidiary to assess the depth of the crisis. Convene a board meeting to document the financial situation and review restructuring or liquidation options.

If the business remains viable but carries an unsustainable debt load, instruct local directors to initiate the Negotiated Settlement process via the Chamber of Commerce. If the subsidiary has no path to profitability and sufficient assets to cover its liabilities, draft the shareholder resolutions required for a voluntary liquidation. Documenting this decision-making process protects the parent company and the local board from future liability claims.