Cross-Border Insolvency Under the Dutch WHOA Framework

Key Takeaways

The Dutch WHOA framework provides a powerful, highly efficient mechanism for restructuring corporate debt outside of formal bankruptcy proceedings. Functioning similarly to the US Chapter 11 and the UK Scheme of Arrangement, it is an essential tool for multinational companies navigating financial distress in the Netherlands.

- The WHOA allows viable companies to enforce a restructuring plan on dissenting creditors through a "cross-class cram-down."

- Foreign creditors possess the exact same voting and economic rights as domestic Dutch creditors during the restructuring process.

- International recognition of the plan depends heavily on whether the debtor elects a public or confidential WHOA procedure.

- Restructuring under the WHOA typically resolves within three to six months, significantly faster than traditional Dutch bankruptcy liquidation.

Understanding the WHOA (Court Approval of a Private Restructuring Plan)

The WHOA (Wet homologatie onderhands akkoord) empowers financially distressed but fundamentally viable companies to restructure their debts by legally binding minority dissenting creditors to a private agreement. Enacted as part of the Dutch Bankruptcy Act, it operates as a "debtor-in-possession" framework, meaning the company's management retains control of daily operations during the restructuring.

To utilize the WHOA, a company must be in a state where it is reasonably likely that it cannot continue paying its debts as they fall due. The core advantage of this framework is the cross-class cram-down mechanism. If at least one class of "in-the-money" creditors votes in favor of the restructuring plan, the Dutch court can approve the agreement and impose it on all other creditor classes, provided no class is worse off than they would be in a bankruptcy liquidation.

According to the official Netherlands Chamber of Commerce and government business portal, the WHOA prevents unnecessary bankruptcies by giving companies a statutory cooling-off period, during which creditors cannot enforce claims or seize assets without court permission.

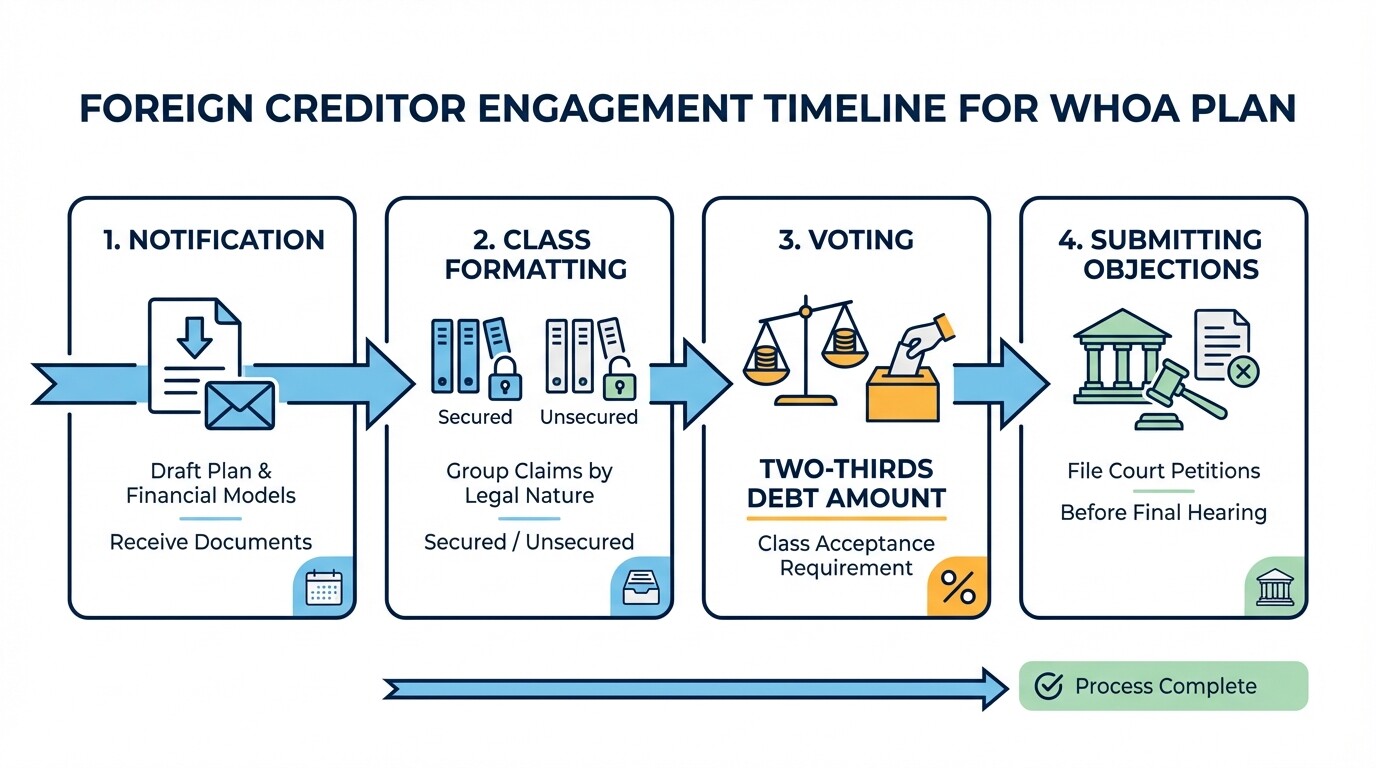

How Foreign Creditors Can Participate in Dutch Restructuring Plans

Foreign creditors participate in a WHOA restructuring under the same statutory rules, timelines, and voting structures as Dutch domestic creditors. The framework strictly prohibits discrimination based on the nationality or geographic location of the creditor.

When a Dutch company initiates a WHOA plan, international creditors should expect the following engagement process:

- Notification: The debtor (or a court-appointed restructuring expert) must formally notify all affected foreign creditors of the draft plan, providing sufficient time to review the proposal and its financial modeling.

- Class Formatting: Creditors are divided into classes based on the legal nature of their claims (e.g., secured, unsecured, subordinated). Foreign security interests are evaluated based on how they would rank under Dutch bankruptcy law.

- Voting: Creditors cast their votes electronically or via written submission. A class is deemed to have accepted the plan if creditors representing at least two-thirds of the total debt amount within that voting class vote in favor.

- Submitting Objections: Foreign creditors who disagree with the plan or their class placement can file a petition with the Dutch court prior to the final confirmation hearing, often challenging the valuation of the company or the liquidation scenario.

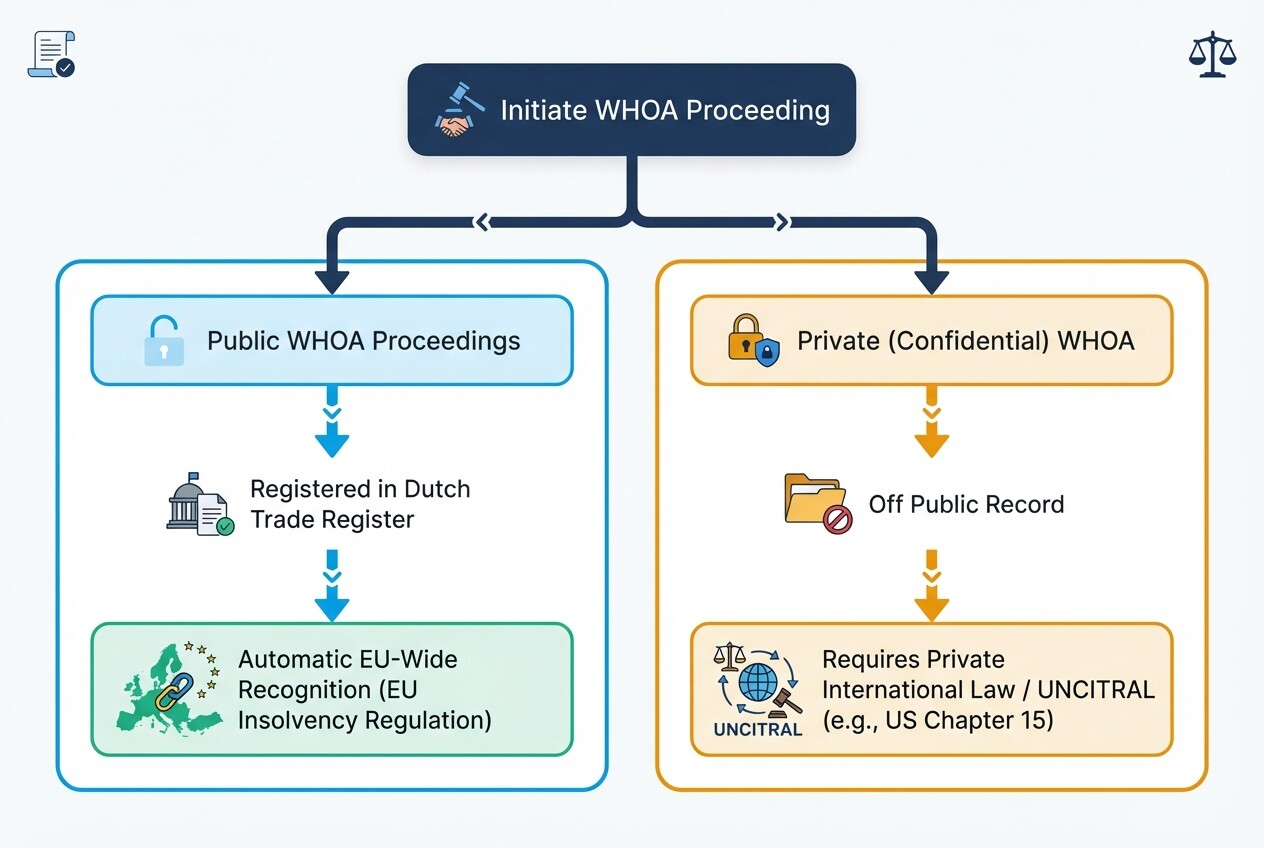

Recognition of Dutch Insolvency Proceedings in International Jurisdictions

The cross-border enforceability of a Dutch WHOA restructuring depends entirely on whether the debtor chooses a public or private procedure at the outset. Companies must strategically select their procedure based on where their assets and key foreign creditors are located.

For multinational businesses, international recognition breaks down into two distinct pathways:

- Public WHOA Proceedings: These are registered in the Dutch Trade Register and trigger automatic recognition across the European Union under the EU Insolvency Regulation (Recast). Creditors across the EU are bound by the Dutch court's ruling, making this ideal for companies with extensive European assets.

- Private (Confidential) WHOA Proceedings: These remain off the public record to protect the debtor's commercial reputation. Because they fall outside the EU Insolvency Regulation, cross-border recognition relies on private international law or the UNCITRAL Model Law on Cross-Border Insolvency. In the United States, a private WHOA can be recognized through a Chapter 15 bankruptcy filing.

Timeline Expectations: Debt Restructuring vs. Formal Bankruptcy

A WHOA restructuring typically takes three to six months from the drafting of the plan to final court confirmation, whereas formal bankruptcy liquidation in the Netherlands often drags on for several years. The WHOA is designed for speed to preserve enterprise value and minimize business disruption.

| Phase / Action | WHOA Restructuring | Formal Bankruptcy (Faillissement) |

|---|---|---|

| Initial Filing & Preparation | 2 to 4 weeks to draft the plan and model valuations. | Immediate court declaration upon filing. |

| Operational Control | Debtor-in-possession (Management stays in control). | Court-appointed bankruptcy trustee takes total control. |

| Cooling-Off Period | Up to 4 months (extendable to 8 months maximum). | Asset freezes immediately; trustee liquidates over time. |

| Creditor Voting | Minimum 8 days notice before the vote. | No creditor vote; trustee distributes available funds. |

| Total Duration | 3 to 6 months | 1 to 5+ years (depending on asset complexity). |

Asset Protection Strategy for International Entities

Multinational parent companies and foreign creditors must actively safeguard their collateral and intellectual property as soon as a Dutch subsidiary or counterparty shows financial distress. Once a WHOA cooling-off period is ordered, enforcement actions are frozen, requiring proactive asset management.

Use this checklist to secure international corporate assets before and during a Dutch restructuring:

- Verify Retention of Title: Ensure your supply contracts contain explicit, properly drafted retention of title (Eigendomsvoorbehoud) clauses valid under Dutch law.

- Register Security Rights: Confirm that any pledges on shares, inventory, or intellectual property are properly registered with the Dutch tax authorities or corporate registries.

- Audit Intercompany Loans: Clearly document parent-company loans to Dutch subsidiaries to ensure they are properly classed during the voting phase, rather than subordinated as equity.

- Monitor Ipso Facto Clauses: Be aware that the WHOA invalidates "ipso facto" clauses. You cannot automatically terminate a contract or revoke an IP license simply because the Dutch company entered a WHOA proceeding.

- Assess Valuation Models: Hire local Dutch financial experts to review the debtor's liquidation valuation to ensure your collateral is not being undervalued in the restructuring plan.

Common Misconceptions About Dutch Restructuring

Many international businesses misunderstand the scope and requirements of the WHOA, leading to missed opportunities for debt recovery or unnecessary panic during cross-border disputes.

- Misconception: All creditors must agree for the WHOA to pass. Reality: The court can approve the plan even if entire classes of creditors vote against it, provided at least one "in-the-money" class approves and the plan is deemed fair and reasonable.

- Misconception: Shareholders lose everything in a WHOA. Reality: Unlike formal bankruptcy, the WHOA allows existing shareholders to retain their equity if the restructuring plan provides adequate value to creditors, making it a valuable tool for parent companies.

- Misconception: The WHOA is only for large multinational corporations. Reality: The legislation includes specific provisions tailored for Small and Medium-sized Enterprises (SMEs), ensuring cost-effective restructuring options for businesses of all sizes.

Frequently Asked Questions

Can a foreign creditor initiate a WHOA proceeding for a Dutch debtor?

Yes. Creditors, shareholders, and employee representatives can petition the Dutch court to appoint a restructuring expert to draft a WHOA plan, even if the debtor's management has not initiated one.

How much does a WHOA proceeding cost?

Costs vary widely depending on the complexity of the debt structure, but a standard mid-market WHOA typically ranges from €75,000 to €250,000 in advisory, valuation, and legal fees.

Does a WHOA proceeding affect employee contracts?

No. The WHOA framework explicitly excludes employment contracts. Employees retain their full rights, and their salaries and benefits cannot be reduced or restructured through this mechanism.

What happens if the court rejects the WHOA plan?

If the Dutch court refuses to confirm the restructuring plan, the debtor cannot appeal the decision. The company will likely have to file for formal bankruptcy (faillissement) or attempt a voluntary, unanimous out-of-court settlement.

When to Hire a Restructuring Lawyer

International creditors and parent companies should engage local legal counsel the moment they receive notice of a WHOA proceeding or suspect a Dutch subsidiary is approaching insolvency. Because the WHOA moves incredibly fast-often requiring creditors to review complex valuation models and submit votes within weeks-early legal intervention is critical to ensuring your claims are placed in the correct voting class and properly valued.

If you are navigating cross-border insolvency, connecting with experienced restructuring and insolvency lawyers in the Netherlands ensures your financial interests are protected under the Dutch statutory framework.

Next Steps

- Review Counterparty Health: Audit your current contracts with Dutch entities to identify exposure to companies experiencing liquidity issues.

- Fortify Contracts: Update terms and conditions to strengthen retention of title and security pledges under Dutch law.

- Establish Local Counsel: Have a qualified Dutch insolvency attorney ready to act swiftly to evaluate restructuring proposals and file court objections if a WHOA plan undervalues your claims.