FAQ: Restructuring Multinational Operations in the Netherlands via WHOA

- Powerful Restructuring Tool: The Dutch WHOA framework functions similarly to the US Chapter 11 or UK Scheme of Arrangement, allowing companies to enforce a restructuring plan on dissenting creditors.

- Holding Company Advantage: Multinational groups frequently use the Netherlands to centralize their restructuring efforts because of its flexible jurisdiction rules and robust corporate holding structures.

- Dual Procedure Options: Companies can choose between a public WHOA procedure, which guarantees automatic EU recognition, and a private, confidential procedure.

- Cross-Class Cramdown: The court can approve a plan even if certain classes of creditors or shareholders vote against it, provided they are not worse off than in a bankruptcy scenario.

- Cost and Speed: A typical WHOA process takes three to six months, offering a highly efficient path compared to drawn-out formal insolvency proceedings.

What is the Dutch WHOA Framework?

The WHOA (Wet homologatie onderhands akkoord) is the Dutch legal framework that allows financially distressed companies to enforce a private restructuring plan on dissenting creditors and shareholders outside of formal bankruptcy. It provides a fast, flexible mechanism to restructure debt, modify burdensome contracts, and secure the survival of viable businesses.

For multinational groups, the Netherlands serves as a premier jurisdiction for corporate holding structures. The WHOA allows international companies with a sufficient connection to the Netherlands to restructure global debt from a centralized Dutch entity. Under the official Dutch Judiciary guidelines for WHOA procedures, the court only intervenes when specifically requested, such as to declare a cooling-off period, vote on a plan, or formally approve (homologate) the final agreement. This limited court involvement keeps the process efficient and heavily driven by the debtor and key stakeholders.

FAQ: How the WHOA Process Impacts International Subsidiaries

This section addresses the most critical questions corporate boards and foreign creditors ask when a Dutch holding company initiates a WHOA restructuring.

Can a Dutch WHOA plan restructure foreign subsidiary debt?

Yes, a WHOA plan can encompass the debt of foreign subsidiaries if the Dutch court assumes international jurisdiction. Jurisdiction is typically established if the foreign subsidiary has its center of main interests (COMI) in the Netherlands, or if the debt is guaranteed by the Dutch holding company and inextricably linked to the group's overall restructuring plan.

Do dissenting foreign creditors have to comply with a WHOA plan?

Dissenting foreign creditors are legally bound by the plan once it is homologated by the Dutch court. The WHOA features a "cross-class cramdown" mechanism, meaning that if at least one in-the-money class of creditors votes in favor of the plan, the court can force dissenting classes to accept the terms. Foreign creditors receive the same legal protections as domestic creditors, including the guarantee that they will not receive less under the plan than they would in a liquidation scenario.

How are shareholder rights affected during a WHOA restructuring?

Shareholder rights can be significantly altered or completely wiped out without their consent under a WHOA plan. If the company is deeply insolvent and the equity holds no underlying economic value, the restructuring plan can dilute existing shares or transfer ownership to creditors through a debt-for-equity swap. Shareholders cannot block a plan if doing so would unreasonably prejudice the creditors.

Does filing for WHOA trigger default clauses in international contracts?

Filing for a WHOA process explicitly protects the debtor from ipso facto clauses. Counterparties cannot terminate contracts, suspend performance, or demand immediate payment solely because the company is preparing or offering a WHOA plan. This protection ensures the multinational entity can maintain critical global operations, supply chains, and licensing agreements while negotiating its debt.

Common Strategic Mistakes by Foreign Creditors and Holding Companies

Foreign stakeholders often jeopardize their financial positions in Dutch restructurings by acting too late, misunderstanding class formations, or ignoring local valuation standards. Navigating the WHOA requires precise tactical execution early in the distress cycle.

- Delaying Engagement: Creditors who wait until the voting phase to voice objections lose their leverage. The most critical phase is the valuation and class formation stage. If creditors do not challenge how they are categorized early on, they risk being grouped with a class that forces a cramdown against their interests.

- Misjudging Liquidation Value: The cornerstone of any WHOA plan is the reorganization value versus the liquidation value. Holding companies sometimes use overly optimistic reorganization values, while foreign creditors fail to hire local Dutch financial advisors to properly challenge these complex, localized valuation models in court.

- Ignoring the Cooling-Off Period: Debtors often fail to request a court-ordered cooling-off period at the start of the process. Without this protection, aggressive foreign creditors can still seize assets or initiate local insolvency proceedings in other jurisdictions, unraveling the entire multinational restructuring strategy.

Alternatives to Formal Bankruptcy in the Netherlands

Beyond the WHOA, multinational companies can avoid formal bankruptcy through consensual private debt agreements, strategic asset spin-offs, or a traditional suspension of payments. The right alternative depends on the level of creditor consensus and the operational health of the underlying subsidiaries.

- Consensual Private Debt Agreements: Before utilizing the statutory force of the WHOA, companies can negotiate purely consensual out-of-court agreements. These require 100 percent approval from affected creditors. They are entirely confidential and cheaper to execute but are highly vulnerable to holdout creditors demanding premium payouts.

- Asset Spin-Offs (Pre-Packaged Sales): A distressed holding company can execute a strategic spin-off by selling its viable international subsidiaries to a newly incorporated entity or a third party. The proceeds are then used to satisfy creditors in the distressed entity. This requires careful navigation of Dutch fraudulent conveyance laws (Actio Pauliana) to ensure assets are sold at fair market value.

- Suspension of Payments (Surseance van betaling): This is a formal, court-supervised procedure intended to provide temporary relief to companies facing short-term liquidity issues. However, it only halts claims from unsecured creditors and rarely succeeds in practice, often serving merely as a precursor to formal bankruptcy.

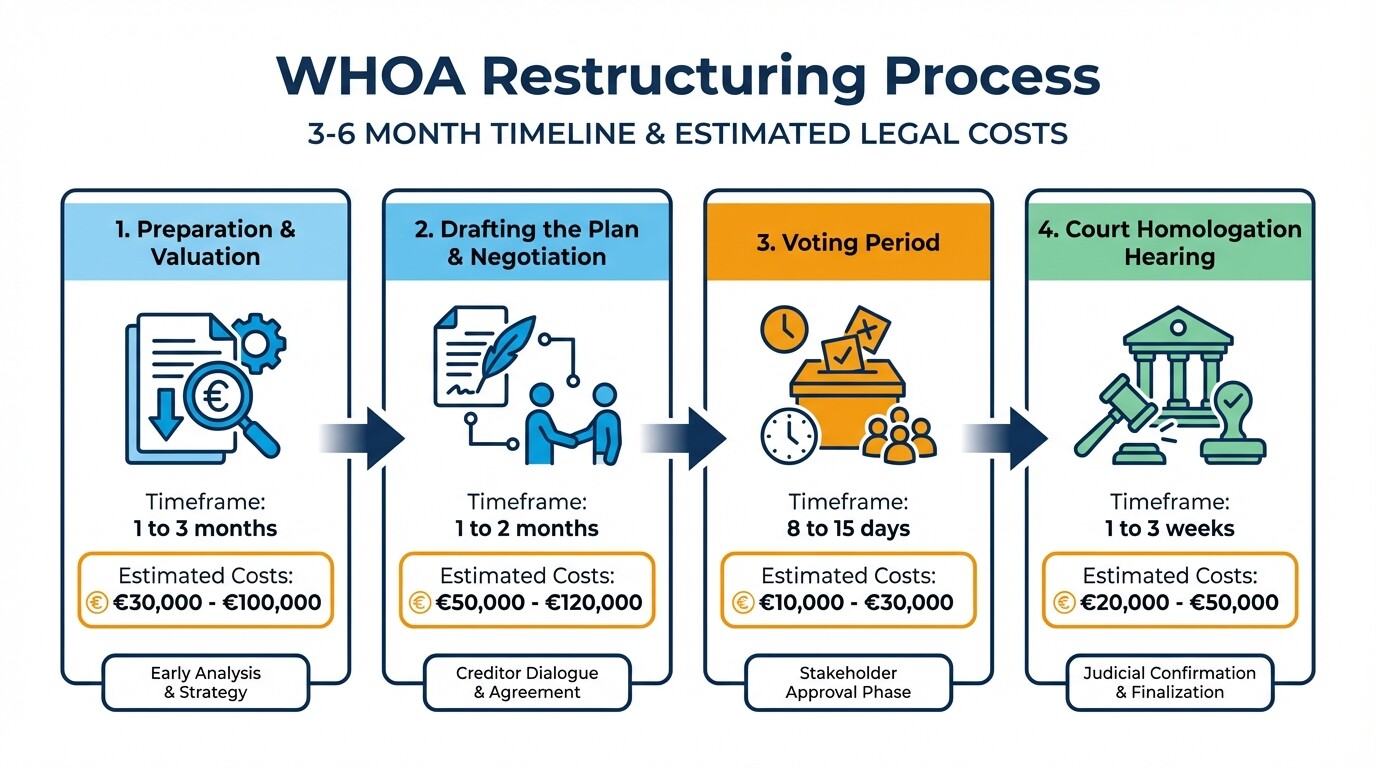

Timelines and Legal Costs for WHOA Restructuring Plans

A WHOA restructuring typically takes three to six months to complete and costs between €50,000 and €250,000, depending heavily on the complexity of the cross-border operations and the level of creditor litigation.

The process moves rapidly once initiated, demanding intense preparation before any court filing occurs. The timeline and cost structure break down into distinct phases.

| Restructuring Phase | Estimated Timeline | Estimated Costs (EUR) |

|---|---|---|

| Preparation & Valuation | 1 to 3 months | €30,000 - €100,000 |

| Drafting the Plan & Negotiation | 1 to 2 months | €15,000 - €75,000 |

| Voting Period | 8 to 15 days | €5,000 - €25,000 |

| Court Homologation Hearing | 1 to 3 weeks | €10,000 - €50,000 |

Court filing fees for the WHOA are nominal, currently set at €676 for corporate petitions. The bulk of the expense stems from specialized legal counsel, financial advisors conducting valuation models, and the potential appointment of a court-appointed restructuring expert or observer.

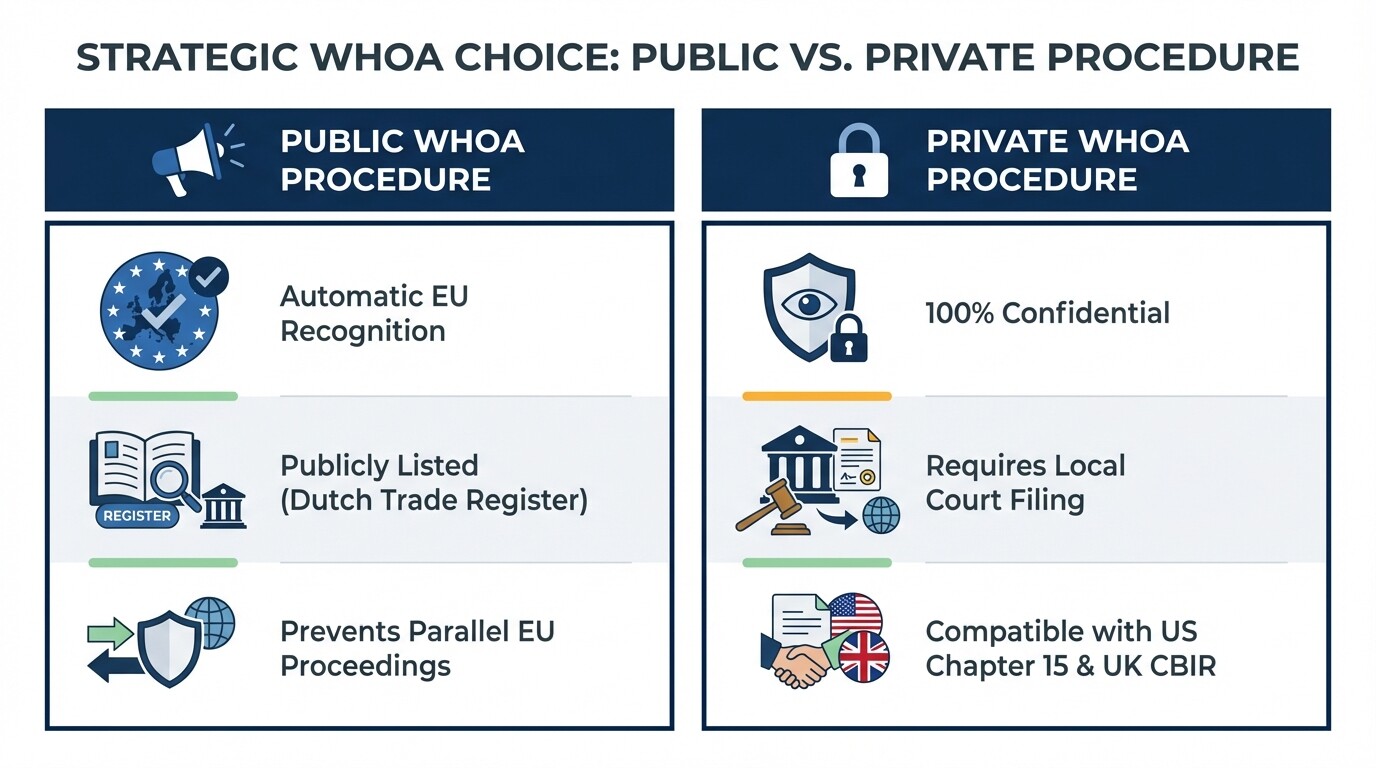

Navigating Cross-Border Recognition of Dutch Restructuring Judgments

Dutch WHOA judgments achieve varying levels of cross-border recognition depending on whether the company opts for a public or private procedure. Securing international recognition is vital to prevent foreign creditors from seizing assets located outside the Netherlands.

If a company selects the Public WHOA Procedure, the judgment is automatically recognized across all European Union member states under the EU Insolvency Regulation (Recast). This prevents creditors from initiating parallel insolvency proceedings in other EU countries. However, the trade-off is that the public procedure is registered in the Dutch Trade Register, making the company's distressed status public knowledge.

If a company selects the Private WHOA Procedure, the process remains completely confidential. While it is not automatically recognized under the EU Insolvency Regulation, companies can still achieve cross-border effect by applying for recognition in specific foreign courts. For US-based assets, a private WHOA plan can be recognized under Chapter 15 of the US Bankruptcy Code. In the UK, recognition is typically sought under the Cross-Border Insolvency Regulations (implementing the UNCITRAL Model Law).

When to Hire a Restructuring Lawyer

Engage a Dutch restructuring lawyer the moment your multinational group anticipates a cash flow crisis that could breach financial covenants within the next six months. Early legal intervention is critical to establish the groundwork for a WHOA procedure, properly value the business, and prevent aggressive creditors from seizing strategic assets.

You will need specialized counsel to negotiate with debt syndicates, defend corporate valuations, and draft the restructuring plan. To find qualified professionals who understand cross-border frameworks, you can consult restructuring and insolvency lawyers in the Netherlands.

Next Steps for Multinational Entities

- Conduct a Financial Stress Test: Model your global cash flow to pinpoint exactly when liquidity will run out and which specific corporate entities hold the most critical debt.

- Assess Jurisdictional Ties: Work with legal counsel to determine if your foreign subsidiaries have a sufficient nexus to the Netherlands to be included in a centralized WHOA plan.

- Initiate Confidential Dialogue: Begin quiet discussions with your largest secured creditors or key shareholders to gauge their appetite for a consensual restructuring before drafting a formal WHOA plan.

- Draft the Valuation Model: Hire local Dutch financial advisors to establish the enterprise's reorganization value versus its liquidation value, which will dictate how you categorize and compensate different creditor classes.