- The Netherlands remains the primary "Gateway to Europe" for UK-based firms due to the Article 23 VAT deferment license, which eliminates the need to pay import VAT upfront.

- Compliance with "Rules of Origin" is mandatory for re-exporting goods into the EU to avoid double taxation under the EU-UK Trade and Cooperation Agreement (TCA).

- By 2026, all Dutch customs declarations must be fully digitalized through the Automated Export System (AES) and the New Computerized Transit System (NCTS Phase 5/6).

- Including a choice-of-forum clause for the Netherlands Commercial Court (NCC) allows international businesses to litigate complex trade disputes in English under Dutch law.

- Bonded warehousing (Type E) offers a strategic legal advantage by delaying duties and VAT until the final moment of sale or distribution.

2026 Customs Readiness Checklist for International Traders

To maintain a seamless supply chain through the Netherlands in 2026, international firms must move beyond transitional arrangements and implement permanent digital and legal structures. This checklist outlines the essential steps for compliance with the latest Dutch customs protocols.

- EORI Number Verification: Ensure your Economic Operator Registration and Identification (EORI) number is valid and linked to your Dutch fiscal representative.

- Article 23 License Application: Secure a VAT deferment license through a local tax representative to avoid immediate cash-flow drainage at the border.

- REX System Registration: If you are an exporter, ensure you are registered in the Registered Exporter (REX) system to certify the origin of goods.

- DMS 4.1 Transition: Confirm your customs software or brokerage is fully integrated with the Declaration Management System (DMS) 4.1, which replaces older manual filing systems.

- CBAM Reporting: For high-carbon goods (steel, aluminum, fertilizers), ensure your 2026 carbon emissions reporting is compliant with the EU's Carbon Border Adjustment Mechanism.

- AEO Status Audit: Evaluate if your business qualifies for Authorized Economic Operator (AEO) status to receive "Green Lane" priority during Dutch customs inspections.

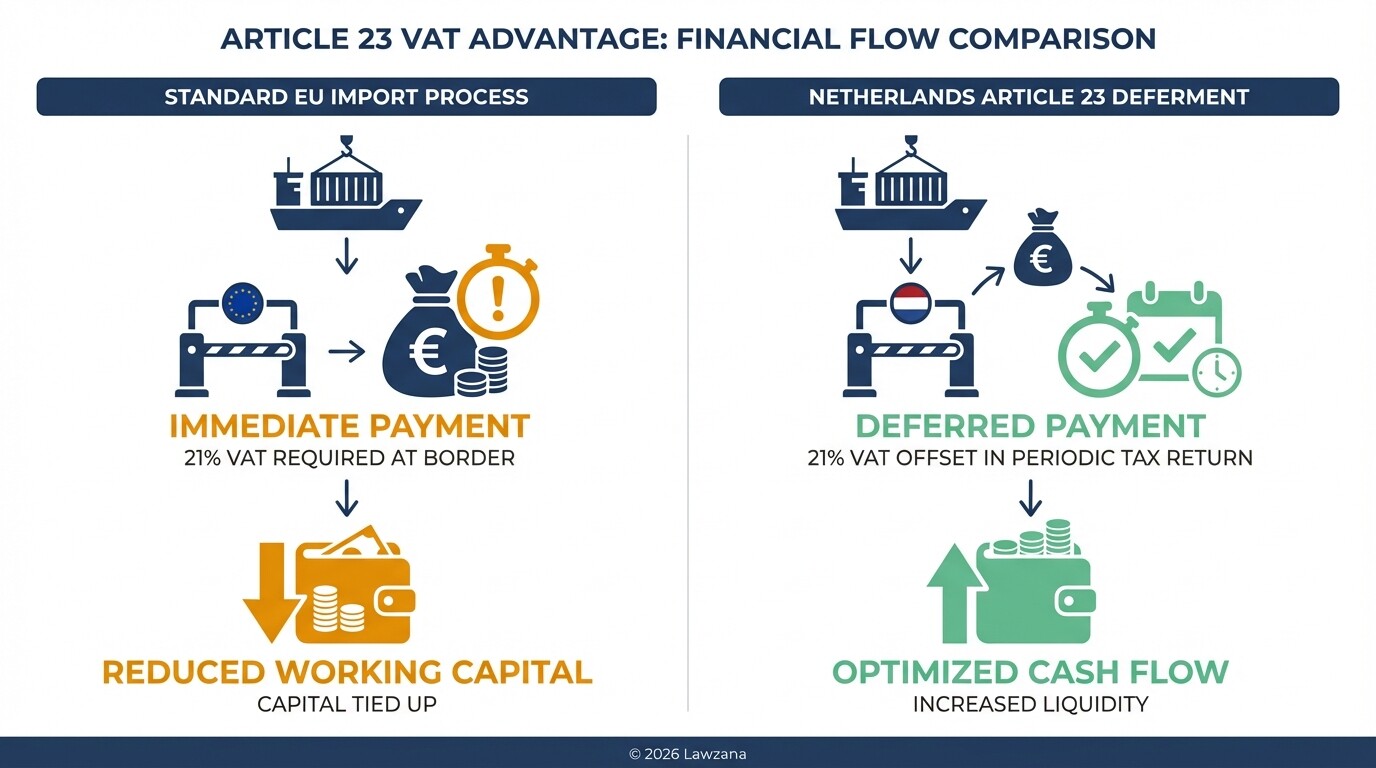

Navigating the VAT Reverse Charge (Article 23)

The Netherlands offers a significant liquidity advantage through Article 23 of the Dutch VAT Act, which allows for the "reverse charge" of import VAT. Instead of paying 21% VAT at the moment goods enter the Port of Rotterdam or Schiphol Airport, the liability is shifted to the periodic VAT return, where it is simultaneously declared and deducted.

To utilize this mechanism, foreign entities typically appoint a General Fiscal Representative (GFR). The representative handles the administrative obligations with the Belastingdienst (Dutch Tax Authority), ensuring the foreign firm does not need to establish a full legal subsidiary in the Netherlands to benefit from the deferment. This is particularly vital for high-value goods where upfront VAT payments would cripple operational cash flow.

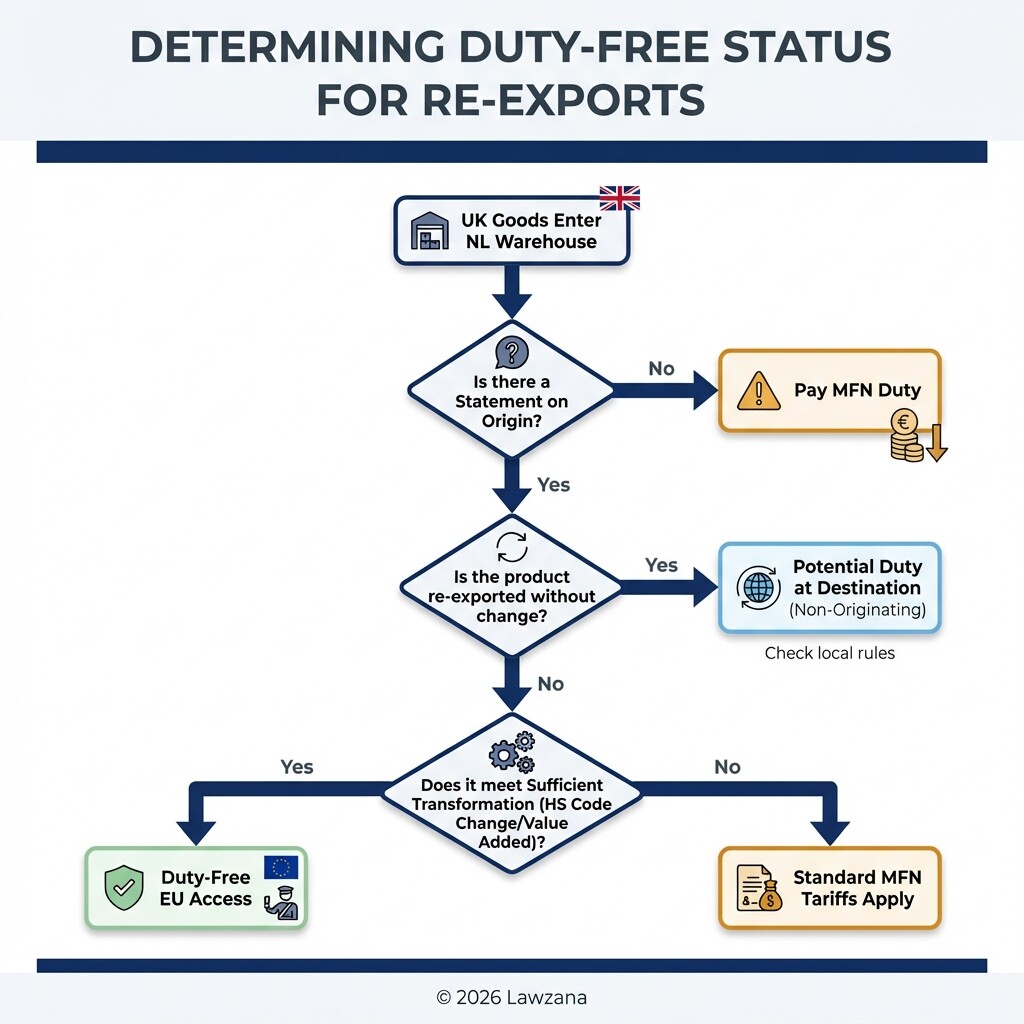

Rules of Origin and Re-Exporting Goods

Under the EU-UK Trade and Cooperation Agreement (TCA), goods originating in the UK can enter the EU duty-free. However, a common legal pitfall occurs when those goods are stored in a Dutch warehouse and then re-exported to another EU member state or a third country without "sufficient transformation."

To maintain tariff-free status, the goods must satisfy specific Rules of Origin. If a product is simply stored and repackaged in the Netherlands, it may lose its "originating" status, triggering standard Most Favored Nation (MFN) tariffs when it crosses another border. International firms must maintain a "Proof of Origin" or a "Statement on Origin" provided by the exporter to claim preferential treatment.

Common "Sufficient Transformation" Criteria

| Method | Description | Legal Requirement |

|---|---|---|

| Change of Tariff Heading | The final product has a different HS Code than the raw materials. | Significant industrial processing required. |

| Value-Added Rule | A specific percentage of the product's value must be created in the EU/UK. | Detailed cost-breakdown documentation. |

| Specific Processing | The product undergoes a specific chemical or mechanical process. | Defined by the specific product Annex in the TCA. |

Digital Customs Documentation Requirements for 2026

The Dutch Customs Authority (Douane) has transitioned to a fully paperless environment, requiring all traders to use the Declaration Management System (DMS). By 2026, the focus shifts to the Automated Export System (AES) and NCTS Phase 6, which demand real-time data accuracy for goods in transit.

These updates require "data-at-the-source," meaning the legal responsibility for the accuracy of HS codes (Customs Tariffs) and valuation rests heavily on the importer of record. Failure to synchronize digital filings with the physical movement of goods can result in immediate "Blocks" at the port, leading to significant demurrage fees. Digital certificates of origin and e-Invoicing are no longer optional; they are the baseline for entry into the Dutch logistics corridor.

Managing Dispute Resolution in Dutch Commercial Contracts

When drafting trade agreements involving Dutch hubs, parties must decide how to resolve conflicts regarding delivery, quality, or payments. The Netherlands is a favored jurisdiction because Dutch commercial law is highly flexible and aligns with the United Nations Convention on Contracts for the International Sale of Goods (CISG).

A major advantage for international firms is the Netherlands Commercial Court (NCC) in Amsterdam. The NCC allows parties to litigate entirely in English, and judgments are enforceable across the EU. This eliminates the "home court advantage" and the language barrier often found in other European jurisdictions.

Sample Choice of Forum and Law Clause

"All disputes arising out of or in connection with this Agreement shall be finally settled in accordance with the [Arbitration Rules of the Netherlands Arbitration Institute / Rules of the Netherlands Commercial Court]. The proceedings shall be conducted in the English language. This Agreement shall be governed by and construed in accordance with the laws of the Netherlands, including the CISG."

Legal Considerations for Bonded Warehousing

A bonded warehouse (or douane-entrepot) is a legally designated area where goods can be stored without paying import duties or VAT. This is a critical strategic tool for companies using the Netherlands as a regional distribution center (RDC).

There are two primary legal structures for this:

- Public Customs Warehouse: Managed by a logistics provider where multiple companies store goods.

- Private Customs Warehouse (Type E): Managed by the company itself, allowing for greater control over inventory but requiring a formal permit from the Dutch Customs Authority.

Legally, goods in a bonded warehouse are considered to be in "suspension." The tax point is only triggered when the goods are "released for free circulation" within the EU. If the goods are re-exported to a non-EU country directly from the warehouse, no EU import duties are ever paid.

Common Misconceptions in Dutch Trade Law

Myth: UK goods are automatically "cleared" for the EU once they land in Rotterdam.

Fact: Landing in the Netherlands does not mean the goods are in "free circulation." They must undergo formal customs clearance and VAT declaration. Without a REX statement or proof of origin, they may still be subject to third-country tariffs despite the Brexit deal.

Myth: You must have a physical office in the Netherlands to import goods.

Fact: You can act as a "non-resident importer" by appointing a Dutch fiscal representative. This allows you to hold an Article 23 license and manage your EU distribution without the overhead of a local office or permanent establishment.

FAQ

What is an Article 23 license?

An Article 23 license is a permit issued by the Dutch Tax Authorities that allows importers to defer the payment of import VAT from the moment of import to their periodic VAT return. This significantly improves cash flow for international businesses.

Do I need a Dutch lawyer to set up a distribution center?

While not strictly required for the physical setup, a lawyer is essential for drafting the warehouse management agreements, ensuring compliance with Dutch labor law for staff, and navigating the complex "Type E" customs permits.

Can I use English in Dutch courts for trade disputes?

Yes, the Netherlands Commercial Court (NCC) is specifically designed for international trade and allows the entire proceeding, including the judgment, to be in English.

What happens if my goods don't meet the "Rules of Origin"?

If your goods do not meet the origin criteria, they will be subject to the EU's Common Customs Tariff. This means you will pay the same duty rate as goods coming from any other non-EU country, such as China or the USA.

When to Hire a Lawyer

International trade involves overlapping layers of EU regulations and Dutch national law. You should consult a legal professional if:

- You are transitioning from a UK-based distribution model to a Dutch-based hub and need to restructure your commercial contracts.

- You are facing a "Customs Audit" or a dispute regarding HS Code classification or valuation.

- You need to draft complex "Triangulation" contracts involving parties in the UK, the Netherlands, and a third EU country.

- You are applying for AEO status or a private bonded warehouse permit and need to ensure your internal compliance manuals meet Dutch legal standards.

Next Steps

- Audit your HS Codes: Ensure your product classifications are up to date with the 2026 Integrated Tariff of the European Union (TARIC).

- Appoint a Fiscal Representative: If you do not have a Dutch entity, vet and appoint a representative to secure your Article 23 VAT deferment.

- Review Logistics Contracts: Update your "Incoterms" (e.g., DDP vs. DAP) to ensure they reflect the current post-Brexit reality of who is responsible for Dutch customs clearance.

- Consult the Official Customs Portal: Review the latest technical specifications for digital filings at Douane.nl.