Navigating Dutch Customs for EU Importers: 2026 Compliance FAQ

- The 2026 EU customs framework requires stricter digital reporting and updated tariff classifications through the incoming EU Customs Data Hub.

- Non-EU entities must secure an EORI number (typically processed in one week) and use a fiscal representative to obtain an Article 23 license to defer import VAT.

- Commercial contracts must specify Incoterms (like DAP vs. DDP) to define whether the buyer or seller is responsible for Dutch customs clearance and import taxes.

- Customs disputes, including tariff misclassification or valuation disagreements, require filing a formal objection with Dutch Customs within a strict six-week deadline.

- Appointing a Dutch fiscal representative allows foreign businesses to import goods without establishing a local corporate entity while legally optimizing cash flow.

2026 EU Customs Valuations and Tariff Classifications

The 2026 EU customs framework introduces strict digital reporting, revised tariff classifications, and valuation audits to prevent undervaluation. Importers must align their master data with the new EU Customs Data Hub and fully integrate Carbon Border Adjustment Mechanism (CBAM) reporting into their compliance workflows.

Customs Valuation Changes

Customs valuations face intensified scrutiny under new digital reporting mandates. Dutch authorities increasingly use predictive analytics to spot discrepancies between the declared transaction value and market benchmarks. Importers must maintain robust audit trails proving that intercompany transfer pricing aligns with arm's-length principles and that no dutiable assists or royalties have been omitted from the customs value.

Binding Tariff Information (BTI)

A Binding Tariff Information (BTI) decision provides absolute legal certainty on the correct classification of your goods across the EU for three years. Non-EU businesses should apply for a BTI through the Dutch Customs Administration well before importing complex or novel products to prevent border delays and retroactive tariff assessments.

Carbon Border Adjustment Mechanism (CBAM)

By 2026, the transitional phase of CBAM ends, and full financial obligations begin. Importers of carbon-intensive goods (such as steel, aluminum, and certain chemicals) must purchase and surrender CBAM certificates. These certificates reflect the emissions embedded in the imported products. Accurate tariff classification is essential, as the HS code determines whether a product falls under CBAM regulations.

Timelines for EORI Numbers and Article 23 Licenses

Securing an Economic Operators Registration and Identification (EORI) number takes approximately one week. Setting up an Article 23 license through a fiscal representative requires four to eight weeks. These are mandatory prerequisites for non-EU entities importing goods into the Netherlands to clear customs and manage taxes efficiently.

| Compliance Requirement | Processing Timeline | Validity | Action Required |

|---|---|---|---|

| EORI Number | 3 to 7 business days | Permanent | Register via the Dutch Tax and Customs Administration (Belastingdienst). |

| VAT Registration | 2 to 4 weeks | Permanent | Apply through a local tax advisor or fiscal representative. |

| Article 23 License | 4 to 8 weeks | Permanent | Requires appointment of a Dutch fiscal representative for non-EU businesses. |

| BTI Decision | Up to 120 days | 3 years | Submit technical specifications and samples to Dutch Customs. |

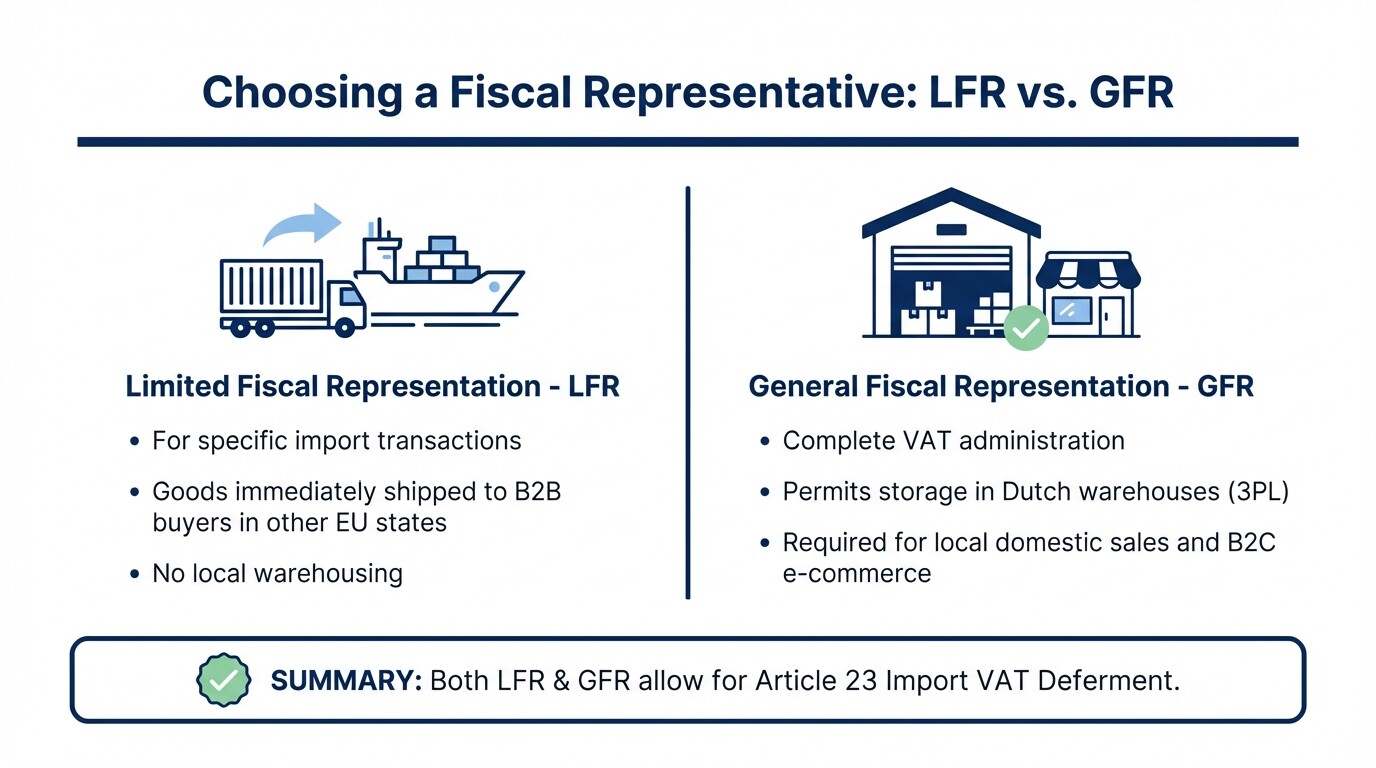

Mitigating Import VAT Through Fiscal Representation

Foreign businesses can defer paying the standard 21% import VAT at the Dutch border by appointing a fiscal representative. This shifts the VAT liability from the moment of import to the periodic VAT return, improving cash flow by eliminating the need to pre-fund import taxes.

To use the Netherlands' Article 23 reverse-charge mechanism, a non-EU business must use either:

- Limited Fiscal Representation (LFR): The representative acts on your behalf solely for specific import transactions. This suits businesses that clear goods into the EU through the Netherlands and immediately ship them to B2B customers in other EU member states.

- General Fiscal Representation (GFR): The representative manages your complete VAT administration in the Netherlands. This is required to store goods in a Dutch warehouse (like a 3PL) and fulfill B2C e-commerce orders or local domestic sales.

Supply Chain Contracts and Incoterms

Cross-border supply chain contracts must explicitly state the applicable Incoterms (2020 rules) to determine which party bears customs clearance responsibilities, risk of loss, and import taxes. Misaligned Incoterms frequently lead to stranded goods and unexpected tax liabilities at the Port of Rotterdam or Schiphol Airport.

For non-EU sellers shipping to the EU, DDP (Delivered Duty Paid) places the maximum burden on the seller. The seller must act as the importer of record, hold an EORI number, and pay all duties. Conversely, DAP (Delivered at Place) shifts the import clearance and duty obligations to the buyer.

Sample Customs Responsibility Clause

To avoid border disputes, commercial agreements should clearly allocate customs responsibilities. Below is a sample clause for a B2B contract using DAP terms:

Delivery and Customs Clearance "All goods shall be delivered DAP (Delivered at Place) to the Buyer's designated facility in the Netherlands, in accordance with Incoterms 2020. The Seller shall be responsible for all export clearance procedures, export duties, and transport costs to the named place of destination. The Buyer shall act as the Importer of Record and shall be solely responsible for obtaining necessary import licenses, completing Dutch customs clearance, and paying all applicable EU import duties, import VAT, and related levies upon the goods' arrival."

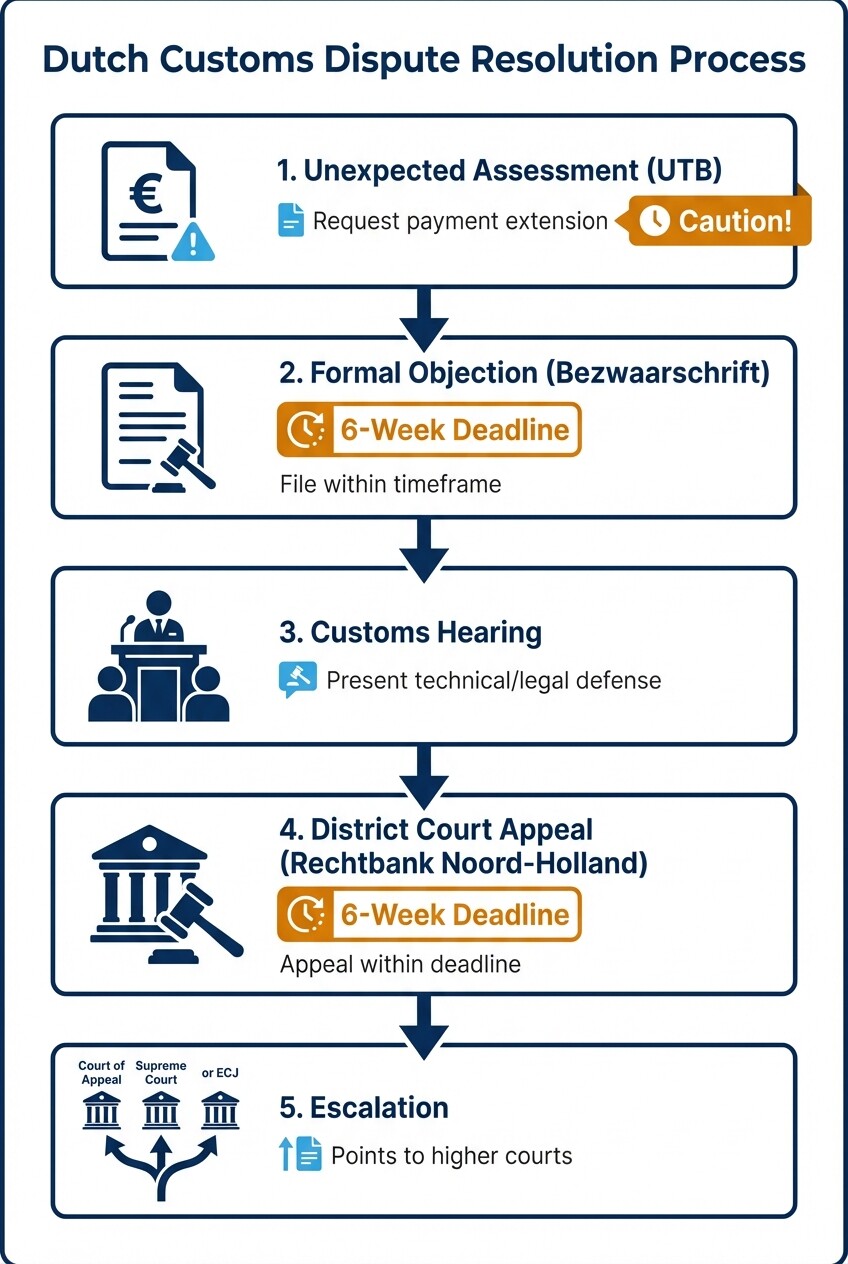

Resolving Disputes with Dutch Customs Authorities

Customs disputes in the Netherlands typically begin with a formal objection (bezwaar) filed with the Dutch Customs Administration within a strict six-week window. If Customs rejects the objection, the importer has the right to appeal the decision in the Dutch judicial system.

- Request payment extension: Immediately upon receiving an unexpected customs assessment (Uitnodiging tot betaling or UTB), formally request a deferment of payment. Payment is not automatically suspended when you file an objection.

- File a formal objection: You must submit a written objection (Bezwaarschrift) to Dutch Customs within six weeks of the date on the assessment notice. Include your EORI number, the reference number of the UTB, and the technical legal grounds for your disagreement (e.g., incorrect tariff code, valuation error).

- Engage in the hearing: You have the right to request a hearing to verbally explain your objection to a customs official. Bring technical experts or legal counsel if the dispute involves complex chemical classifications or transfer pricing data.

- File an appeal: If Customs rejects your objection, you have six weeks to file an appeal (Beroep) with the District Court of North Holland (Rechtbank Noord-Holland), which handles customs matters.

- Escalate to higher courts: If the District Court rules against you, further appeals can be made to the Court of Appeal in Amsterdam, and ultimately, on matters of law, to the Dutch Supreme Court or the European Court of Justice.

Common Misconceptions About Dutch Import Compliance

- Local VAT numbers: Many foreign businesses assume a Dutch VAT number is all they need to import. In reality, non-EU businesses must also have an EORI number and cannot defer import VAT without a local fiscal representative holding an Article 23 license.

- Title transfer: Incoterms determine risk, transport costs, and customs responsibilities, but they do not define when the legal ownership of the goods transfers from seller to buyer. Title transfer must be separately defined in your sales contract.

- Customs broker liability: Importers often believe their customs broker is legally responsible for declaration errors. Unless the broker acts as an "indirect representative" (which is rare and restrictive), the importer of record bears full financial and legal liability for misclassifications or under-declarations.

Frequently Asked Questions

Can I use an EORI number from another EU country in the Netherlands?

Yes. An EORI number issued by any EU member state is valid throughout the entire European Union, including the Netherlands. You do not need a separate Dutch EORI if you already possess a valid German or French one.

How much does it cost to hire a fiscal representative?

Costs vary based on shipping volume and complexity. Businesses typically pay between €1,500 and €5,000 annually for General Fiscal Representation, plus one-time setup fees. Brokers may also require a bank guarantee to cover potential VAT liabilities.

What happens if I misclassify a product's HS code?

Misclassifying goods can result in the retroactive collection of underpaid duties for up to three years, administrative fines ranging from hundreds to thousands of euros, and delayed shipments. In cases of deliberate fraud, criminal prosecution is possible.

Do I need a Dutch corporate entity to import into the Netherlands?

No. Non-EU businesses can import goods into the Netherlands without establishing a local B.V. (Besloten Vennootschap) by utilizing a local customs broker and a fiscal representative.

When to Hire a Customs Trade Lawyer

While customs brokers handle routine declarations, you should engage an international trade lawyer when facing serious regulatory hurdles. You need legal counsel if Dutch Customs issues a large retroactive duty assessment, if your goods are seized due to alleged intellectual property infringements or sanctions violations, or if you need to appeal an unfavorable BTI decision. A lawyer is also vital to ensure your transfer pricing agreements align with customs valuation rules to survive an audit.

If you are facing an audit or need help structuring your EU supply chain, consult international trade lawyers in the Netherlands to protect your business interests.

Next Steps for Importers

To prepare for 2026 compliance, take the following actions:

- Audit your product catalog to ensure all HS codes are accurate and assess whether any products fall under the expanding CBAM requirements.

- Review commercial contracts to verify that Incoterms are clearly defined and appropriately shift customs risk.

- Initiate discussions with a Dutch fiscal representative to secure an Article 23 license and optimize your European cash flow, especially if you currently pre-fund import VAT.