- Tax and operations: Regular corporations have geographic flexibility. PEZA corporations receive tax holidays but must operate within designated economic zones.

- Capital requirements: Foreign-owned businesses targeting the local market need at least USD 200,000 in capital. Export enterprises are exempt from this threshold.

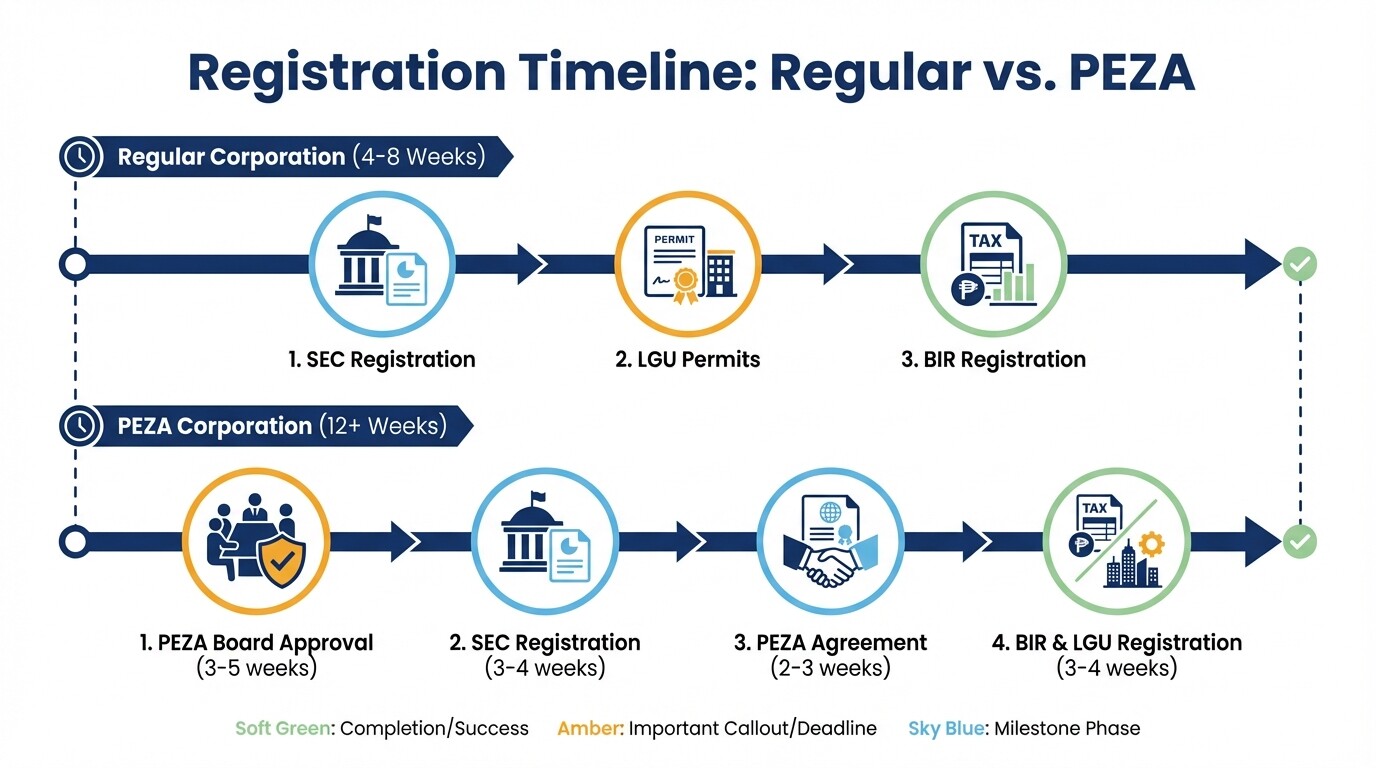

- Processing timelines: SEC registration for regular corporations takes 4 to 8 weeks. PEZA registration processes take 12 weeks or more.

- Corporate structure: Articles of Incorporation must align strictly with the Foreign Investment Negative List to pass SEC review.

Corporate Tax and VAT Comparison

Choosing between a regular corporation and a PEZA-registered entity determines your tax obligations. Regular corporations pay standard corporate income tax. PEZA-registered entities receive Income Tax Holidays (ITH) and special tax rates. PEZA entities also receive zero-rated VAT on local purchases and import tax exemptions.

| Feature | Regular Corporation | PEZA-Registered Corporation |

|---|---|---|

| Corporate income tax | 20% to 25% based on net taxable income and total assets. | 4 to 7 years Income Tax Holiday (ITH), followed by a 5% tax on gross income. |

| Value-Added Tax | 12% standard VAT on domestic sales and imports. | Zero-rated VAT on local purchases and exemption on imported capital equipment. |

| Local taxes | Subject to standard local business taxes and permit fees. | Exempt from local government taxes once the 5% gross income tax phase begins. |

| Customs duties | Standard tariffs apply to imported equipment and raw materials. | Tax and duty-free importation of raw materials, capital equipment, and spare parts. |

Eligibility for PEZA Registration

To qualify for PEZA registration, a business must operate in a designated special economic zone and engage in specific export activities. The Philippine Economic Zone Authority limits these incentives to sectors such as IT/BPO, electronics, and manufacturing.

Foreign investors must meet specific thresholds to maintain these incentives:

- Zone location: The business must place its principal office and operations inside a PEZA-proclaimed IT Park, IT Building, or industrial economic zone.

- Export volume: The enterprise must export at least 70% of its total output. IT and BPO companies meet this requirement by serving clients based entirely outside the Philippines.

- Permitted industries: Eligible activities include export manufacturing, IT service export, tourism, medical tourism, and logistics directly supporting export enterprises.

- Project brief: Applicants must submit a feasibility study proving the business will create local jobs and introduce new technology to the Philippines.

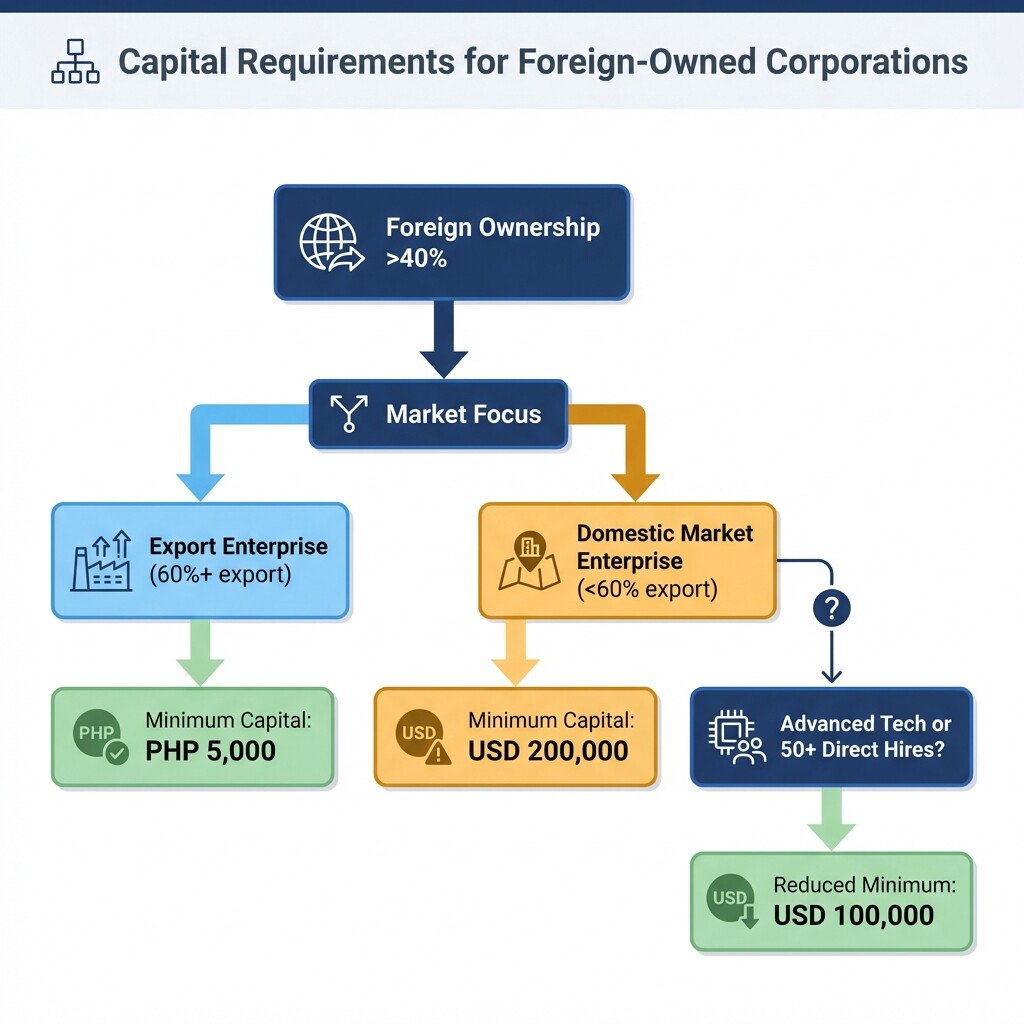

Capital Requirements by Market Focus

Capital requirements depend on whether the business targets the domestic market or exports its goods and services. Export enterprises need less minimum capital than foreign-owned domestic market enterprises.

If your corporation is more than 40% foreign-owned, the Philippine government categorizes it based on its target market:

- Domestic Market Enterprise: Foreign entities selling primarily to the Philippine market (less than 60% export) must capitalize the company with a minimum of USD 200,000. This drops to USD 100,000 if the business uses advanced technology or employs at least 50 direct hires.

- Export Enterprise: A business exporting 60% or more of its output is exempt from the USD 200,000 threshold. The legal minimum paid-up capital is PHP 5,000, though practical operating costs require a higher initial investment.

SEC vs. PEZA Registration Timelines

Registering a regular corporation with the SEC takes 4 to 8 weeks. PEZA registration takes 12 weeks or more because the agency heavily evaluates project feasibility studies and requires board approval.

The standard Regular Corporation process (4 to 8 weeks) involves:

- Reserving the corporate name and submitting the Articles of Incorporation to the Securities and Exchange Commission (SEC).

- Obtaining the Barangay Clearance and Mayor's Business Permit from the local government unit.

- Registering with the Bureau of Internal Revenue (BIR) for taxation and employee benefit accounts (SSS, PhilHealth, Pag-IBIG).

The PEZA Corporation process (12+ weeks) is sequential:

- PEZA Board approval: Submission of the project brief, financial projections, and anti-graft certifications to the PEZA board (3 to 5 weeks).

- SEC registration: Registering the entity with the SEC after PEZA issues a pre-approval resolution (3 to 4 weeks).

- PEZA agreement: Signing the formal agreement with PEZA and paying registration fees (2 to 3 weeks).

- BIR and LGU registration: Securing the specific PEZA-aligned BIR Certificate of Registration and local zone permits (3 to 4 weeks).

Common Drafting Errors in Articles of Incorporation

Foreign investors often draft broad purpose clauses or misalign their authorized capital stock with foreign ownership laws. These errors cause SEC rejections and delay incorporation.

When drafting your Articles of Incorporation (AoI), avoid these specific errors:

- Vague primary purpose: The SEC requires the primary purpose to be highly specific. For PEZA applicants, the primary purpose in the AoI must match the exact activity approved in the PEZA Board Resolution.

- Violating the negative list: Including secondary purposes that involve restricted industries (like mass media or specific retail categories) causes an automatic SEC rejection for companies with foreign equity.

- Incorrect capital structure: Documents must state the exact USD to PHP exchange rate used at the time of incorporation. Domestic market enterprises must also document the exact routing of the USD 200,000 capital injection.

Operational and Compliance Rules

Many foreign investors misunderstand PEZA boundaries and the rules around foreign ownership. Following these rules prevents compliance penalties and forced shutdowns.

- Geographic limits: A PEZA-registered IT or manufacturing company cannot lease a standard commercial office space. Operations must remain strictly within PEZA-accredited buildings or ecozones. Moving equipment out of the zone without a permit violates customs laws.

- Foreign ownership maximums: The Philippines allows 100% foreign ownership for most business types. Restrictions apply only to specific industries listed in the Foreign Investment Negative List (FINL) and domestic enterprises that fail to meet the USD 200,000 capital minimum.

- Domestic sales allowance: PEZA allows export enterprises to sell up to 30% of their production to the domestic market. However, any sales made to the domestic market are subject to regular corporate income tax and standard VAT.

- Converting regular entities: An existing regular corporation can apply for PEZA registration. The company must set up a distinct facility within a PEZA economic zone and maintain separate accounting books for its PEZA-registered activities.

- BIR registration: Every PEZA-registered enterprise must register with the Bureau of Internal Revenue (BIR). The BIR issues a specific Certificate of Registration recognizing the company's tax-exempt status under PEZA laws.

Legal Structuring and Next Steps

Structuring a foreign-owned corporation in the Philippines requires adherence to capitalization laws, the FINL, and tax regulations. A business registration lawyer in the Philippines can organize your corporate structure to secure incentives and pass SEC or PEZA review.

Before filing, complete these steps:

- Determine your primary market to calculate if you will export more than 60% of your output.

- Secure the USD 200,000 capital requirement if establishing a domestic market enterprise.

- Identify PEZA-accredited IT buildings or industrial parks if pursuing PEZA incentives.

- Draft your project brief and Articles of Incorporation to align with your chosen registration path.