Corporate Restructuring and Insolvency in Singapore: Foreign Parent Guide

- Singapore's Insolvency, Restructuring and Dissolution Act (IRDA) is a debtor-friendly framework supporting cross-border restructuring.

- Parent companies are generally protected from a Singapore subsidiary's debts unless corporate guarantees exist or the corporate veil is pierced for fraud.

- Alternatives to liquidation like Schemes of Arrangement and Judicial Management let distressed subsidiaries restructure debt while operating.

- Singapore adopted the UNCITRAL Model Law on Cross-Border Insolvency. This enables local courts to recognize foreign proceedings.

- Engaging local legal counsel early helps secure moratoriums against creditor actions and negotiate super-priority rescue financing.

Navigating Singapore's Insolvency Framework

Singapore offers a restructuring framework governed by the Insolvency, Restructuring and Dissolution Act 2018 (IRDA). Foreign parent companies can use local courts to manage a subsidiary's financial distress. They can also restructure cross-border debt or orderly wind down operations.

The statutory framework balances creditor rights with debtor rehabilitation. Singapore is a strategic jurisdiction for multinational restructuring. It has specialized commercial courts and operates under the UNCITRAL Model Law on Cross-Border Insolvency. Under this law, Singapore courts recognize foreign insolvency proceedings and cooperate with foreign judges. This lets a global parent company synchronize restructuring efforts internationally. The legal infrastructure encourages corporate rescue over liquidation. It offers automatic moratoriums and cross-class cramdowns to bind dissenting creditors to a restructuring plan.

For exact statutory definitions and procedural rules, foreign counsel should refer directly to the Insolvency, Restructuring and Dissolution Act 2018 published by the Singapore Attorney-General's Chambers.

Alternatives to Formal Insolvency

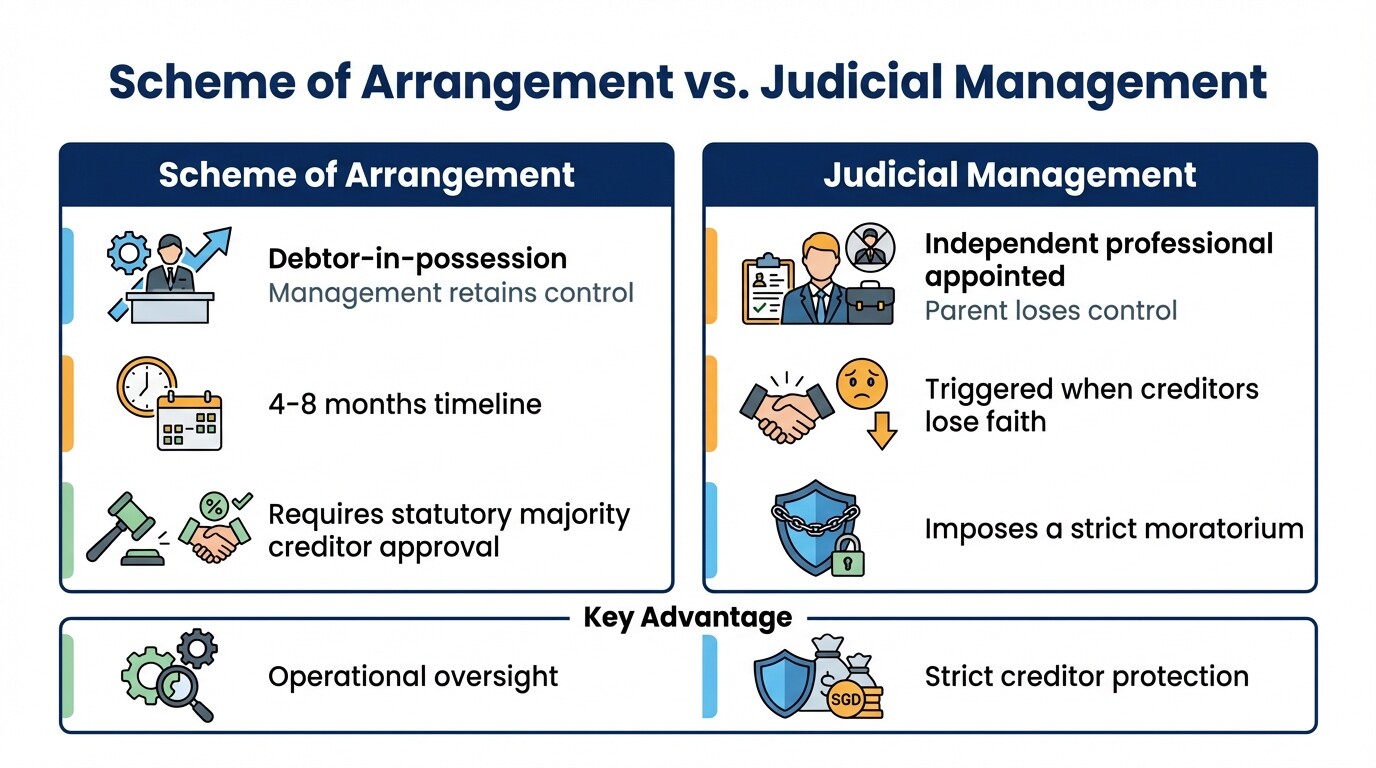

Rather than liquidating a subsidiary, foreign parents can use a Scheme of Arrangement or Judicial Management to rehabilitate the business. These tools offer moratoriums to block creditor actions while the company negotiates a rescue plan.

A Scheme of Arrangement is a court-approved agreement between a company and its creditors to restructure obligations. It is a debtor-in-possession regime. The existing management retains control of the company during the restructuring. This helps foreign parent companies maintain operational oversight of their subsidiary. The company can secure super-priority status for rescue financing and cram down a restructuring plan on dissenting creditor classes if the statutory majority approves. A Scheme generally takes four to eight months from the initial court application to final approval. The timeline depends on asset valuation and creditor resistance.

Judicial Management applies when the court appoints an independent insolvency professional to control the distressed subsidiary. This option usually triggers when creditors lose faith in the existing management. The Judicial Manager must rehabilitate the company or achieve a better realization of assets than a standard winding-up. The parent company loses direct control. However, Judicial Management imposes a strict moratorium on creditor claims to buy time to stabilize the business.

Protecting Foreign Parent Company Assets

Singapore law recognizes the separate legal personality of a subsidiary. Parent company assets are shielded from a subsidiary's debts. This protection fails if the parent provided corporate guarantees, commingled funds, or engaged in fraudulent trading.

To isolate financial risk, foreign parent companies must ensure their Singaporean subsidiaries operate independently. Creditors of an insolvent subsidiary cannot access the parent company's assets unless they pierce the corporate veil. Courts in Singapore lift this veil under exceptional circumstances, such as when the subsidiary is a sham designed to evade legal obligations.

Parent companies expose themselves to liability through everyday commercial practices. If the parent issued letters of comfort or corporate guarantees to secure bank loans for the subsidiary, those obligations remain enforceable regardless of the subsidiary's insolvency. Also, if parent company executives act as shadow directors for the subsidiary and allow the entity to incur debt while knowing it is insolvent, they are personally liable for reckless or fraudulent trading under Singapore law. Directors are not automatically personally liable for corporate debts unless they breach fiduciary duties. Allowing new debt when insolvency is inevitable leads to wrongful trading charges.

Parent Company Risk Management Checklist

Evaluate your parent company's exposure to a distressed Singaporean subsidiary. Proactive separation of assets and operational boundaries maintains the corporate veil and limits cross-border liability.

- Review corporate guarantees: Audit financial agreements, leases, and supplier contracts to identify any formal guarantees or legally binding letters of comfort issued by the parent.

- Assess intercompany loans: Document all loans between the parent and subsidiary. Secure and negotiate them on arm's-length terms to prevent subordination during insolvency. In liquidation, secured creditors are paid first. Unsecured parent company claims rank equally with other unsecured trade creditors.

- Verify operational independence: Confirm the subsidiary maintains its own bank accounts, separate financial records, and distinct board meetings without commingling funds.

- Evaluate director overlap: Identify executives holding dual directorships in both the parent and the subsidiary. Ensure they strictly observe fiduciary duties to the Singapore entity when it approaches insolvency.

- Audit IP ownership: Confirm that the parent or a separate holding company owns core intellectual property used by the subsidiary. License it to the subsidiary under clear contractual terms that terminate upon insolvency.

Estimated Legal Costs for Corporate Restructuring

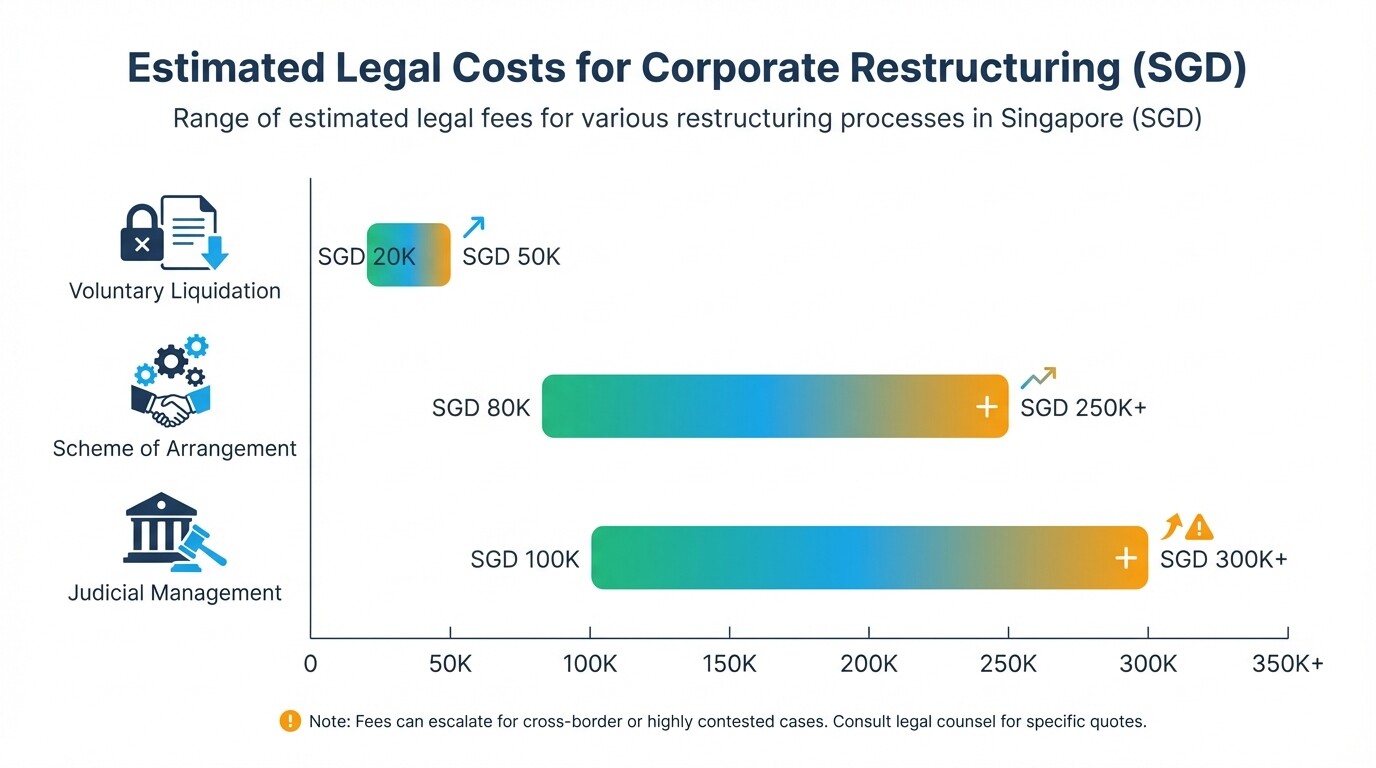

Restructuring costs in Singapore vary based on the complexity of the debt, the number of creditor classes, and whether the proceedings are contested. Baseline legal fees start around SGD 50,000 for straightforward restructurings and escalate into six figures for cross-border cases.

When budgeting, multinational companies must account for legal fees and the fees of appointed insolvency practitioners.

- Scheme of Arrangement: Legal fees typically range from SGD 80,000 to SGD 250,000 or more. The debtor-in-possession nature means the company avoids paying an independent manager, but court applications and creditor negotiations require intensive legal work.

- Judicial Management: Costs range from SGD 100,000 to over SGD 300,000. Besides legal fees for the court application, the company pays the hourly rates of the appointed Judicial Manager, which accrue rapidly over a multi-month process.

- Voluntary Liquidation: A straightforward Creditors' Voluntary Winding Up costs between SGD 20,000 and SGD 50,000 in legal and liquidator fees. This assumes there are no asset recovery actions or cross-border disputes.

Common Misconceptions About Singapore Insolvency

Multinational executives often hold inaccurate assumptions about how Singapore handles corporate distress. Understanding the legal reality prevents strategic errors and protects parent company interests.

Mandatory liquidation: Many executives assume an insolvent subsidiary must immediately cease operations and liquidate. Singapore actively promotes restructuring. Filing for a moratorium under a Scheme of Arrangement lets the business operate while management negotiates a viable debt repayment plan.

Ignoring foreign proceedings: Some parent companies believe restructuring must happen entirely in parallel jurisdictions. Because Singapore adopted the UNCITRAL Model Law, local courts can recognize foreign main proceedings, stay local creditor actions, and coordinate a unified global restructuring effort. A Singapore moratorium has an extraterritorial effect on creditors subject to Singapore jurisdiction. Enforcing that stay on overseas assets requires the foreign jurisdiction to recognize the Singapore court's order.

Non-binding letters of comfort: Parent companies often issue letters of comfort to support a subsidiary's credit lines, assuming they hold no legal weight. Singapore courts evaluate the exact wording of these documents. If the language shows clear promissory intent, the court enforces it as a binding guarantee. This exposes the parent to the subsidiary's debt.

When to Hire Counsel and Next Steps

Engage Singapore counsel the moment a subsidiary shows signs of cash flow insolvency, breaches financial covenants, or faces statutory demands from creditors. Early intervention preserves business value, protects the parent company from inadvertent liability, and opens doors to debtor-in-possession rescue financing.

If your multinational corporation is navigating subsidiary distress, immediately gather all intercompany financial documents, corporate guarantees, and subsidiary debt agreements. Do not transfer assets out of the subsidiary or repay intercompany loans without legal advice. Courts challenge these actions as unfair preferences. Reach out to experienced restructuring and insolvency lawyers in Singapore to evaluate whether a Scheme of Arrangement, Judicial Management, or orderly winding down is the most strategic path forward.