- The UK recognizes foreign insolvency proceedings primarily through the UNCITRAL Model Law, requiring a formal application to the UK courts to protect local assets.

- Post-Brexit, automatic recognition of UK insolvency proceedings within the EU has ceased, making parallel proceedings or local recognition strategies necessary for pan-European businesses.

- The Restructuring Plan (Part 26A) allows distressed companies to implement a cross-class cram down, forcing dissenting creditors to accept a restructuring agreement if specific legal conditions are met.

- Directors of distressed UK subsidiaries face strict personal liability risks for wrongful trading if they fail to prioritize creditor interests the moment insolvency becomes unavoidable.

- Foreign creditors must actively register their claims and ensure their security interests are properly filed with Companies House to maintain priority in a UK distribution.

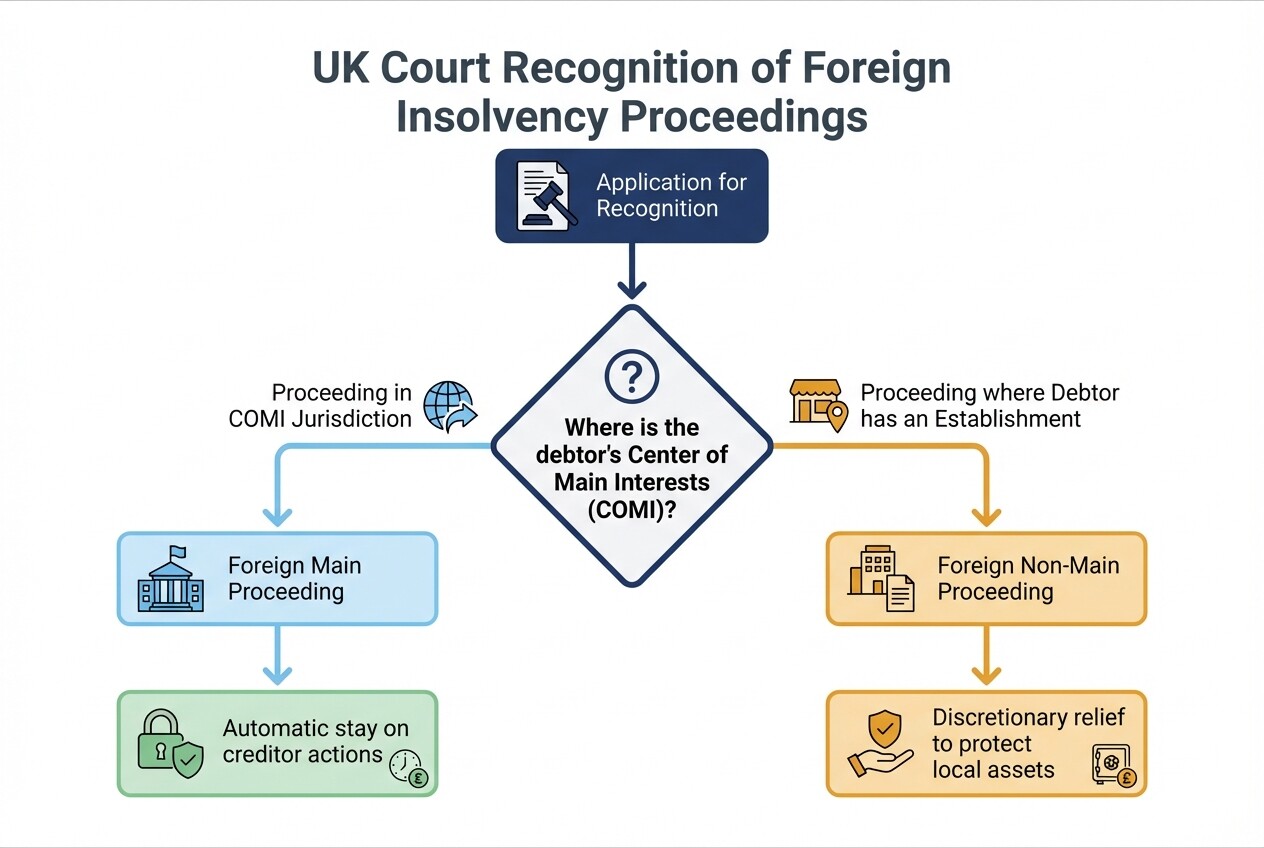

How Does the UK Recognize Foreign Insolvency Proceedings?

The UK recognizes foreign insolvency proceedings primarily through the Cross-Border Insolvency Regulations 2006, which implements the UNCITRAL Model Law into domestic law. This framework allows foreign insolvency practitioners to apply to UK courts for recognition of their proceedings, enabling them to stay creditor actions against the debtor's UK-based assets.

When a foreign representative applies for recognition, the UK court must determine the debtor's Center of Main Interests (COMI). If the foreign proceeding is taking place where the debtor has its COMI, the UK court will recognize it as a "Foreign Main Proceeding." This grants an automatic stay on individual creditor actions and executions against the debtor's assets in the UK, similar to the moratorium provided in a domestic insolvency.

If the foreign proceeding is located in a jurisdiction where the debtor merely has an establishment rather than its COMI, the court may recognize it as a "Foreign Non-Main Proceeding." In this scenario, relief is not automatic and is granted at the discretion of the UK court to protect local assets or the interests of creditors.

You can review the precise statutory framework for this recognition process in the Cross-Border Insolvency Regulations 2006.

Restructuring Alternatives in the UK

Companies facing distress can utilize three primary statutory restructuring mechanisms under UK law: Restructuring Plans, Company Voluntary Arrangements (CVAs), and Administration. Each offers different levels of debtor control, creditor compromise, and court involvement, making the choice of procedure highly dependent on the group's specific financial architecture.

Below is a comparison of the primary restructuring vehicles available to multinational groups with UK operations:

| Restructuring Mechanism | Debtor-in-Possession? | Cross-Class Cram Down? | Primary Use Case |

|---|---|---|---|

| Restructuring Plan (Part 26A) | Yes (Directors remain in control) | Yes (Can bind dissenting creditor classes) | Complex capital structures requiring debt write-downs across multiple layers of secured and unsecured debt. |

| Company Voluntary Arrangement (CVA) | Yes (Directors remain in control) | No (Cannot bind secured or preferential creditors without consent) | Operational restructuring, specifically widely used for compromising landlord lease claims and unsecured trade debt. |

| Administration | No (Licensed Insolvency Practitioner takes over) | N/A (Statutory distribution waterfall applies) | Halting immediate creditor action (via a powerful moratorium) to facilitate a going-concern business sale or structured wind-down. |

The Restructuring Plan was introduced by the Corporate Insolvency and Governance Act 2020 and has become the premium tool for large cross-border restructurings because it allows a court to sanction a plan even if an entire class of creditors votes against it, provided they are no worse off than in the relevant alternative scenario.

Cross-Border Creditor Claim and Security Registration Checklist

Foreign creditors must submit specific documentation to UK officeholders, such as administrators or liquidators, to formally register their claims and enforce security interests. Failing to properly register security at Companies House within 21 days of creation renders it void against a liquidator or administrator, turning a secured lender into an unsecured creditor.

International creditors must compile and submit the following documentation to protect their financial position:

- Proof of Debt Document: A formal statutory form detailing the exact amount owed at the date the company entered the insolvency procedure.

- Contractual Evidence: Executed copies of the underlying commercial contracts, facility agreements, or master service agreements establishing the liability.

- Statement of Account: Detailed ledgers, unpaid invoices, and a breakdown of any interest or late fees accrued up to the date of insolvency.

- Evidence of Security: Copies of fixed or floating charge instruments, alongside the official registration certificates issued by UK Companies House.

- Retention of Title Clauses: For suppliers of physical goods, specific contract terms proving ownership of goods supplied but not yet paid for, paired with an immediate request to inspect the debtor's premises.

- Certified Translations: If the original agreements governing the debt are not in English, certified translations must be provided to the UK insolvency practitioner.

How to Protect Intellectual Property and Foreign Subsidiaries

Safeguarding intellectual property and foreign subsidiaries during a UK parent company's insolvency requires ring-fencing critical assets and reviewing licensing agreements for insolvency termination clauses. UK insolvency law restricts certain "ipso facto" clauses that automatically terminate supplier contracts upon insolvency, but careful structuring is still vital to prevent enterprise value destruction.

When a UK parent company enters administration or liquidation, its shares in foreign subsidiaries become assets of the insolvency estate. The UK officeholder will typically seek to sell these shares to generate returns for creditors. To protect the wider global group, multinational businesses should ensure intercompany debt is properly documented and subordinated where necessary. Additionally, cross-guarantees between the UK parent and foreign subsidiaries must be quantified, as a UK default could trigger immediate acceleration of debt in foreign jurisdictions.

Intellectual property should ideally be held in a solvent, bankruptcy-remote entity within the group. If the distressed UK company holds the IP and licenses it to foreign subsidiaries, the foreign entities must ensure their licensing agreements are robust. Under UK law, an administrator cannot simply disclaim an IP license to extract higher fees, but they can sell the underlying IP subject to existing licenses, which may introduce hostile new owners to the group's technology stack.

What Are the Duties of Directors Managing a Distressed UK Subsidiary?

Directors of a distressed UK subsidiary must shift their fiduciary duties from acting in the best interests of shareholders to protecting the interests of the company's creditors. Continuing to trade without a reasonable prospect of avoiding insolvent liquidation exposes directors to personal liability for wrongful trading under the Insolvency Act 1986.

In a multinational group, subsidiary directors often face a conflict between instructions from the foreign parent company and their strict duties under UK law. If the UK subsidiary is insolvent or bordering on insolvency, the directors must take every step a reasonably diligent person would take to minimize potential losses to the subsidiary's creditors. This duty applies independently of the parent company's global strategy.

Failure to observe these duties can result in wrongful trading claims, where directors are ordered by a court to personally contribute to the company's assets. Furthermore, directors can face disqualification from acting as a director of any UK company for up to 15 years. Directors must hold frequent, minuted board meetings to document their decision-making process and prove they are actively monitoring cash flow and seeking professional restructuring advice.

Common Misconceptions About UK Cross-Border Insolvency

Multinational groups often misunderstand the jurisdictional reach and post-Brexit landscape of UK insolvency law. These errors can lead to missed restructuring opportunities or unexpected director liabilities.

- Chapter 11 automatically protects UK assets: A US Chapter 11 bankruptcy filing does not automatically stop creditor actions in the UK. The US debtor must make a separate application to the UK courts under the Cross-Border Insolvency Regulations 2006 to have the Chapter 11 proceedings recognized and secure a local stay on enforcement.

- EU insolvency recognition remains automatic: Prior to Brexit, the EU Insolvency Regulation provided automatic recognition of UK insolvency proceedings across member states. This is no longer the case. UK practitioners must now rely on the domestic laws of individual European countries or the UNCITRAL Model Law where enacted, significantly increasing the complexity and cost of pan-European restructurings.

- Parent companies are strictly liable for subsidiary debts: Under English law, the principle of separate corporate personality applies. A foreign parent company is not automatically liable for the debts of its insolvent UK subsidiary unless it has provided explicit corporate guarantees or has operated the subsidiary in a way that pierces the corporate veil.

Frequently Asked Questions

What is the Center of Main Interests (COMI) in UK insolvency?

COMI is the location where a debtor conducts the administration of its interests on a regular basis and is ascertainable by third parties. By default, this is presumed to be the jurisdiction of the company's registered office, but this presumption can be rebutted if head office functions and creditor relations are managed elsewhere.

How much does a UK Restructuring Plan cost?

Due to the requirement for dual court hearings and extensive financial modeling, a UK Restructuring Plan (Part 26A) typically costs upwards of £500,000 for mid-market companies and can reach several million pounds for complex, multinational capital structures.

Can foreign creditors vote in a UK Company Voluntary Arrangement?

Yes. Foreign unsecured creditors have the same rights as domestic unsecured creditors to vote on a CVA proposal. A CVA requires the approval of 75 percent by value of the voting unsecured creditors to become legally binding on all unsecured creditors, regardless of their location.

What is a pre-pack administration?

A pre-pack administration is a procedure where the sale of the distressed company's business and assets is fully negotiated before the company enters administration. Immediately upon the administrator's appointment, the sale is executed, preserving enterprise value and minimizing business interruption.

When to Hire a Restructuring Lawyer

You should engage a specialized UK restructuring lawyer the moment a multinational group anticipates breaching financial covenants or faces liquidity shortages affecting its UK operations. Early intervention provides access to a wider range of rescue mechanisms and provides a critical defense against director liability claims.

Complex capital stacks involving varied jurisdictions require coordinated legal strategy before any formal default occurs. For assistance navigating these frameworks, you can consult experienced restructuring and insolvency lawyers in the United Kingdom to evaluate your immediate obligations.

Next Steps for Multinational Companies

Taking decisive, documented action is critical when managing cross-border financial distress. Follow a structured approach to assess exposure and stabilize operations to ensure compliance with UK legal standards.

- Assess Cash Flow: Generate a rolling 13-week cash flow forecast specifically for the UK subsidiary to identify immediate liquidity shortfalls.

- Review Intercompany Agreements: Map out all cross-guarantees, intercompany loans, and IP licenses between the UK entity and the global group to isolate contagion risks.

- Convene the Board: Hold a formal board meeting for the UK subsidiary to acknowledge the financial position and formally document the shift in duties toward creditor protection.

- Instruct Counsel: Retain UK-qualified restructuring counsel and financial advisors to explore statutory alternatives like a CVA or Restructuring Plan before value erodes.