Key Takeaways

South African exchange controls strictly regulate how funds, including intellectual property (IP) royalties, leave the country. Foreign licensors must secure formal government approval before they can legally receive royalty payments from a South African entity.

- Mandatory approvals: Cross-border IP agreements require authorization from the Department of Trade, Industry and Competition (DTIC) and the South African Reserve Bank (SARB).

- Rate limits: The DTIC restricts royalty rates to between 2% and 6% of net sales, depending on the IP type.

- Compliance delays: Regulatory review takes three to six months. Companies must plan cash flows accordingly.

- Tax implications: A standard 15% withholding tax applies to royalties, though Double Taxation Agreements (DTAs) often reduce this.

- Penalty risks: Remitting royalties before securing SARB approval is illegal and leads to blocked funds and financial penalties.

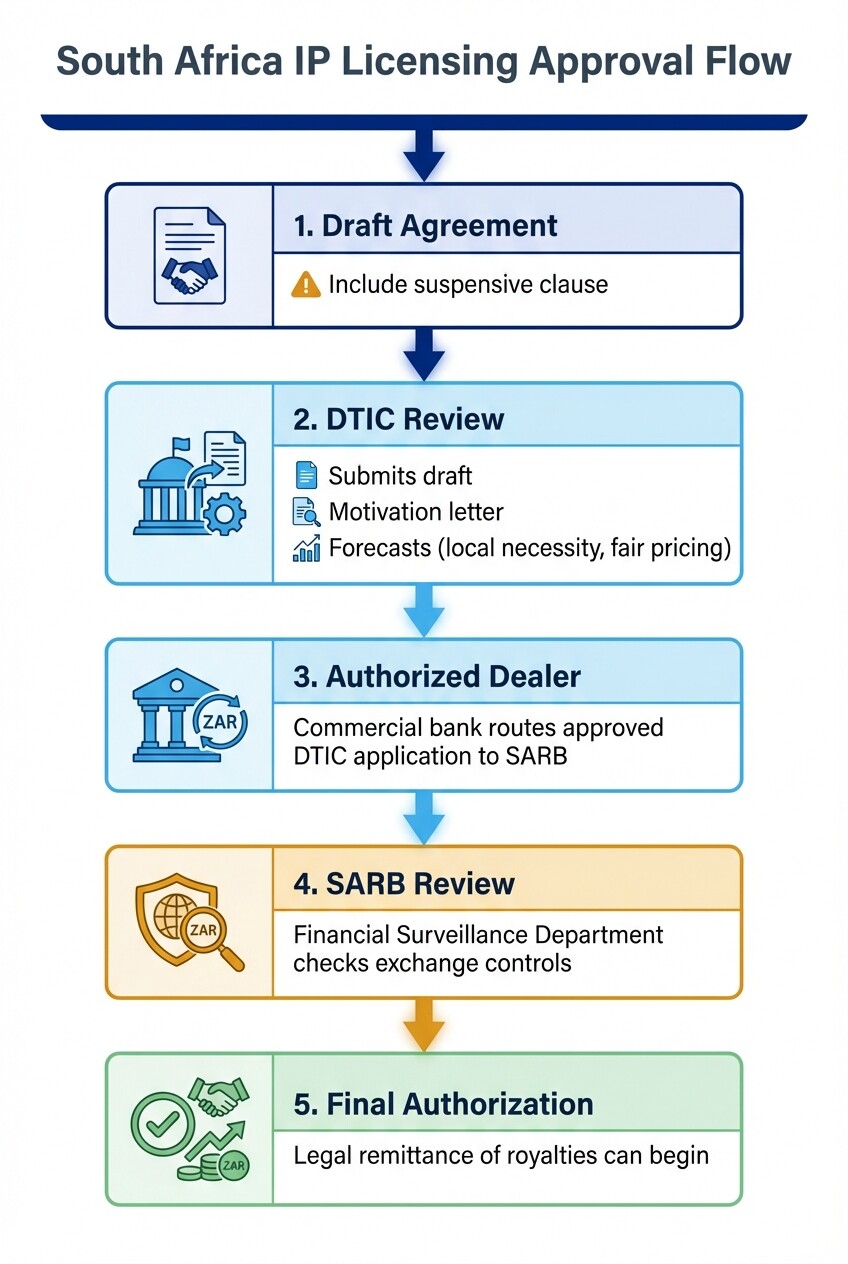

The Mandatory SARB and DTIC Approval Process

Any cross-border agreement licensing intellectual property to a South African entity requires prior approval from the South African Reserve Bank (SARB) and the Department of Trade, Industry and Competition (DTIC). Without these authorizations, a local subsidiary cannot legally transfer royalty payments out of the country.

The approval process is a dual-layered regulatory review. First, the DTIC evaluates the licensing agreement to confirm the IP is necessary for the local company, unavailable locally, and priced fairly. Once the DTIC recommends approval, the application moves to the SARB Financial Surveillance Department. SARB handles the exchange control authorization. This dictates how and when the local currency (ZAR) can be converted and remitted offshore.

Companies do not apply to SARB directly. All exchange control applications must go through an Authorized Dealer. This is a commercial bank in South Africa licensed by SARB to handle foreign exchange transactions. You can review the official exchange control guidelines through the SARB Financial Surveillance framework.

IP Licensing Compliance Checklist

Securing approval for cross-border IP royalties requires coordination between legal, tax, and financial teams. Use this compliance checklist to meet all regulatory requirements before executing the agreement and transferring funds.

- Determine IP valuation: Prepare documentation proving the economic benefit the IP brings to the South African entity. Include financial projections and market analysis.

- Draft suspensive contracts: Structure the IP licensing agreement with a suspensive clause. (e.g., "This Agreement, and the obligations hereunder, are subject to the Licensee obtaining written approval from the South African Reserve Bank.")

- Justify the royalty rate: Ensure the proposed rate aligns with DTIC thresholds. Gather independent transfer pricing documentation to support the valuation.

- Appoint an Authorized Dealer: Select a South African commercial bank for all SARB submissions and future currency conversions.

- Submit to the DTIC: Route the draft agreement, a motivation letter, and financial forecasts to the DTIC for preliminary appraisal.

- Finalize SARB application: Once DTIC approves, submit the final application packet through your Authorized Dealer to SARB for formal authorization.

- Apply for tax directives: If relying on a Double Taxation Agreement (DTA) to reduce withholding taxes, submit the declaration forms to the South African Revenue Service.

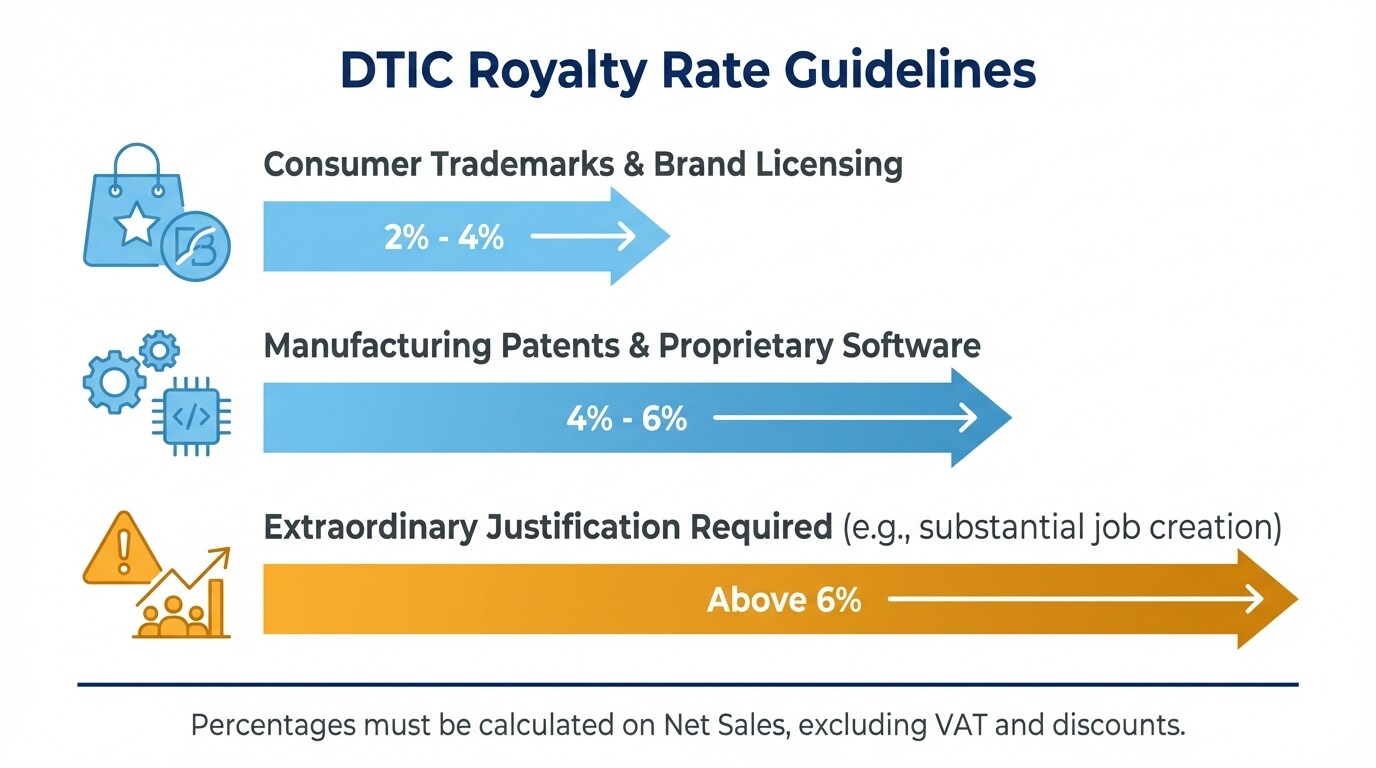

Structuring Acceptable Royalty Rates

The DTIC restricts how much capital can leave South Africa through IP royalties. Acceptable royalty rates fall between 2% and 6% of the licensed product's net sales or manufacturing cost. This depends heavily on the nature of the intellectual property.

Consumer trademarks and brand licensing command lower rates. The DTIC often caps them between 2% and 4%. Manufacturing patents, proprietary software, and complex technological processes can push toward the 4% to 6% range. If a foreign licensor attempts to charge a rate higher than 6%, the DTIC requires extraordinary justification. Acceptable justification includes proof of substantial job creation or specialized technology transfer that impacts the local market.

The DTIC evaluates royalties based on net sales and prohibits calculations based on gross revenue. You must deduct items like value-added tax (VAT), trade discounts, and packaging costs before applying the approved royalty percentage.

Expected Timelines for Regulatory Review

Regulatory approval for foreign IP licensing in South Africa takes three to six months. Multinational companies must factor this delay into their cash flow projections. Initial royalties cannot be remitted until formal authorization is officially granted.

| Review Phase | Estimated Timeline | Typical Activities |

|---|---|---|

| DTIC Review | 4 to 8 weeks | Application compilation, economic justification, preliminary appraisal |

| SARB Review | 4 to 6 weeks | Exchange control authorization via the Authorized Dealer |

Errors in the application, missing transfer pricing documents, or aggressive royalty structures trigger requests for clarification. This resets the review clock and extends the timeline.

Withholding Tax and Double Taxation Agreements

South Africa imposes a standard 15% withholding tax on all royalty payments made to non-residents. Foreign licensors can legally reduce or eliminate this tax burden by using Double Taxation Agreements (DTAs) between South Africa and their home jurisdiction.

Before an Authorized Dealer releases funds, the South African licensee must withhold the required tax and pay it directly to the South African Revenue Service (SARS). If the foreign licensor is based in a country with a favorable DTA with South Africa (such as the United States, the United Kingdom, or the Netherlands), the withholding tax rate can drop to 10%, 5%, or 0%.

To apply this reduced rate, the foreign licensor must complete a declaration form confirming their tax residency and entitlement to DTA benefits. The licensee must keep this declaration on file and submit it to SARS to justify the reduced withholding amount. Detailed requirements are outlined in the SARS Withholding Tax on Royalties guide.

Common Compliance Pitfalls

Foreign corporations often misjudge South Africa's financial surveillance framework. Mistakes here lead to trapped capital, financial penalties, and voided commercial contracts.

- Premature payments: The most common mistake is a local subsidiary attempting to pay royalties prior to formal SARB authorization. This violates the Exchange Control Regulations. It immediately results in blocked funds, audits, and financial penalties for the South African entity.

- Over-reliance on OECD guidelines: Multinational companies assume a royalty rate complying with global transfer pricing guidelines is automatically approved. The DTIC evaluates rates based on local economic benefit and internal caps. Globally standard rates are rejected if they exceed local thresholds.

- Assuming SaaS is exempt: Pure, off-the-shelf Software-as-a-Service (SaaS) subscriptions fall under standard import of services and require less scrutiny. However, licensing software source code or granting rights to commercialize software locally triggers full IP exchange control requirements.

Advanced Compliance Scenarios

Strict exchange controls generate specific challenges for multinational corporations entering the South African market.

Consequences of Unauthorized Payments Unauthorized royalty payments violate the Exchange Control Regulations, rendering the transaction illegal. The commercial bank will block the international transfer. The South African entity faces audits from the Reserve Bank and criminal liability for its directors.

Management Fees vs. Royalties SARB heavily scrutinizes management fees to prevent disguised capital extraction. Management fees must be proportional to documented services rendered. Companies cannot use them as a backdoor mechanism to extract IP licensing revenue without DTIC approval.

Duration of Approvals SARB approvals for royalty agreements are granted for a specific duration. This typically matches the term of the underlying contract, often three to five years. Once the approved period expires, the parties must submit a renewal application to the DTIC and SARB to continue remitting funds.

Trademarks vs. Patents The DTIC applies stricter royalty caps to consumer trademarks and branding licenses, rarely approving rates above 4%. Patents, proprietary manufacturing processes, and deep technology transfers are viewed as adding tangible value to the economy. These can occasionally secure rates up to 6%.

When to Hire a Lawyer

Engage local counsel before drafting the IP licensing agreement or transferring any intellectual property rights into South Africa. A lawyer specializing in South African corporate and financial law will properly structure your contracts with the necessary suspensive conditions required by SARB.

Legal counsel manages the submission process with the DTIC, liaises with your Authorized Dealer, and ensures royalty rates align with current regulatory thresholds. Attempting to manage this process from abroad without local representation routinely leads to rejected applications. Consult with experienced contract lawyers in South Africa who understand the Financial Surveillance Department.

Next Steps

Initiating an IP licensing arrangement in South Africa requires proactive regulatory planning.

First, conduct an internal valuation of the IP you intend to license and determine a defensible royalty rate between 2% and 6%. Next, draft the licensing agreement with explicit conditions stating that the contract's validity requires final SARB and DTIC approval. Finally, partner with a South African Authorized Dealer and local legal counsel to compile your economic justification packet and begin the formal application.