- Mandatory notification is required for any merger meeting the intermediate or large financial thresholds under South African law.

- South Africa assesses mergers on both competitive impact and rigid public interest criteria, specifically employment and historically disadvantaged ownership.

- Implementing any part of a global merger in South Africa before official clearance is illegal and risks administrative penalties of up to 10% of annual turnover.

- Foreign acquirers must proactively structure Broad-Based Black Economic Empowerment commitments and job preservation strategies early in the deal timeline.

- Cross-border deals often trigger parallel filings in other African regional blocs, requiring careful timeline synchronization to avoid closing delays.

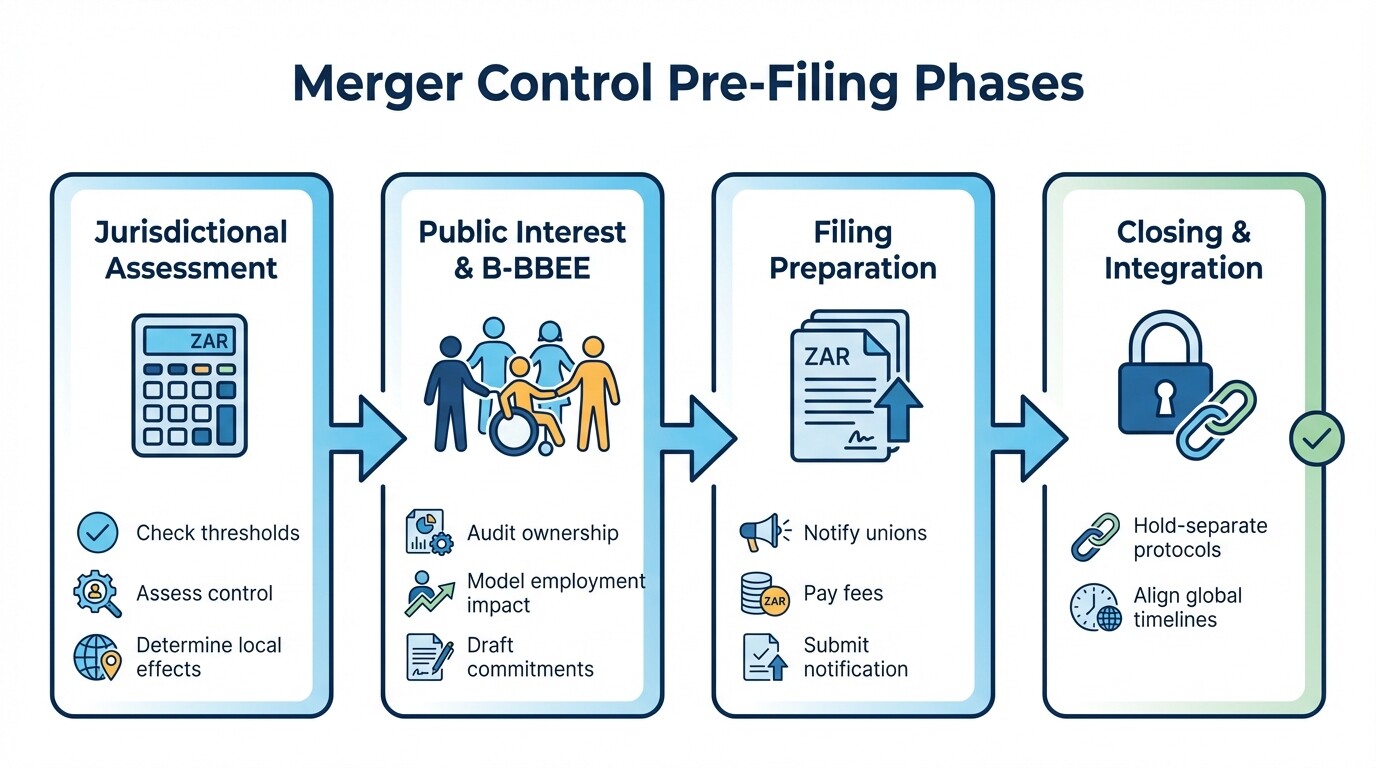

South Africa Merger Control Pre-Filing Checklist

Foreign acquiring firms must evaluate multiple financial, regulatory, and social metrics before executing a transaction in South Africa. Use this comprehensive checklist to ensure your merger complies with local regulations and avoids costly procedural delays.

Phase 1: Jurisdictional and Threshold Assessment

- Verify if the transaction constitutes a merger by assessing the transfer of direct or indirect control over the target firm.

- Calculate the combined annual turnover and asset values of the acquiring and target firms in South Africa.

- Determine if the transaction meets the "intermediate" or "large" merger thresholds requiring mandatory notification.

- Identify if the transaction has any "effect" within South Africa, even if the acquiring firm lacks a physical local presence.

Phase 2: Public Interest and B-BBEE Strategy

- Audit the target firm's current Broad-Based Black Economic Empowerment status and ownership structures.

- Model the post-merger impact on the target firm's employment numbers, specifically identifying any potential duplications or job losses.

- Draft binding commitments to protect domestic employment, such as moratoriums on retrenchments for a specific period.

- Develop a strategy to promote ownership by historically disadvantaged persons or workers, often through an employee share ownership plan.

Phase 3: Filing Preparation and Submission

- Prepare the primary filing documents, including the competitive analysis and comprehensive public interest justifications.

- Notify recognized trade unions or employee representatives of the target firm, as legally required before filing.

- Pay the prescribed filing fee to the Competition Commission in South African Rand.

- Submit the formal notification to the Competition Commission and, if a large merger, prepare for Competition Tribunal hearings.

Phase 4: Closing and Integration Protocol

- Implement strict "hold-separate" protocols to ensure no operational integration occurs before the official clearance certificate is issued.

- Align the South African clearance timeline with other global or African regional antitrust filings.

- Execute the global closing only after securing explicit regulatory approval or finalizing an approved carve-out arrangement for the local entity.

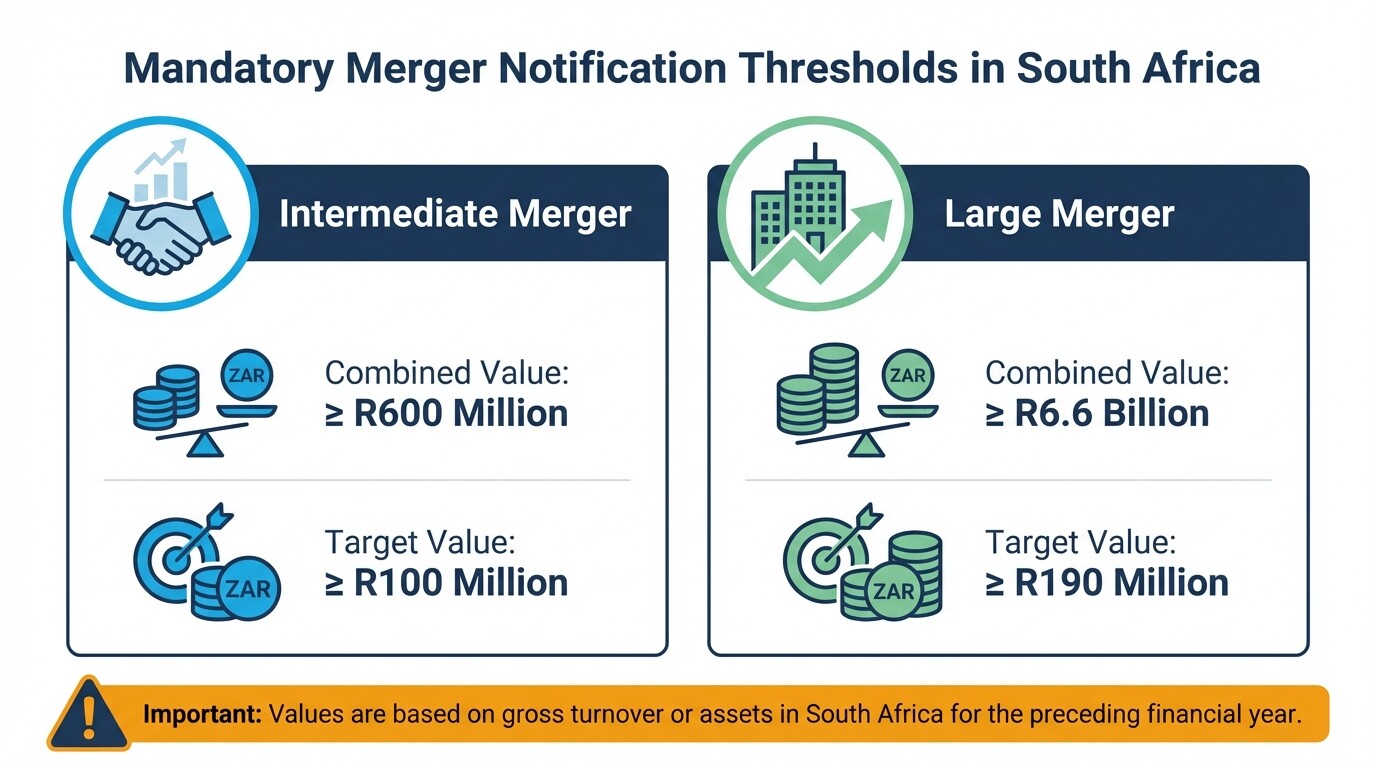

How to Calculate Combined Financial Thresholds for Mandatory Notification

Mergers in South Africa require mandatory notification if the transaction involves a change of control and meets specific financial thresholds based on turnover and asset value. You must calculate these figures using the firms' gross values in South Africa for the preceding financial year.

The Competition Commission of South Africa categorizes notifiable transactions into intermediate and large mergers. An intermediate merger occurs when the combined turnover or asset value of both firms in South Africa equals or exceeds R600 million, provided the target firm's value is at least R100 million. A large merger is triggered when the combined value reaches or exceeds R6.6 billion, with the target firm contributing at least R190 million.

If your transaction falls into either category, you are legally prohibited from implementing the merger until you receive formal approval. Small mergers falling below these thresholds generally do not require notification unless specifically requested by the Commission within six months of implementation. Foreign acquirers must carefully account for all South African-derived revenues, including export sales into the country, when determining their aggregate values.

Assessing the Impact on Employment and B-BBEE

South African competition law mandates that every merger is scrutinized for its impact on employment and the economic inclusion of historically disadvantaged persons. A transaction that is perfectly sound from a market competition standpoint can still be prohibited if it fails to satisfy these distinct public interest criteria.

Foreign acquirers must present a detailed analysis of how the transaction will affect local jobs. If the merger will result in duplicated roles and subsequent retrenchments, the acquiring firm must justify these losses economically and offer mitigation strategies, such as retraining programs or severance packages that exceed statutory minimums. The Commission routinely imposes conditions capping the number of job losses or enforcing strict moratoriums on retrenchments for two to three years post-merger.

Equally critical is the transaction's effect on Broad-Based Black Economic Empowerment (B-BBEE). The acquiring firm must demonstrate how the merger promotes a greater spread of ownership among historically disadvantaged persons and workers. Foreign companies often achieve this by establishing Employee Share Ownership Programs or partnering with local empowerment consortiums to ensure the post-merger entity maintains or improves its transformation profile.

Public Interest Considerations Under the Competition Act

Regulators in South Africa now treat public interest provisions not merely as a secondary check, but as an equal pillar alongside traditional competition metrics. Foreign acquirers must prepare robust, proactive defenses showing tangible benefits to the local economy to secure approval under evolving enforcement standards.

Recent updates and aggressive enforcement trends surrounding the Competition Act signal a zero-tolerance approach to deals that dilute domestic ownership or harm local industries. The authorities increasingly mandate that foreign acquirers introduce specific, binding conditions to support local supply chains and small businesses. You cannot simply promise not to harm the local economy; you must demonstrate how the transaction actively advances industrialization and economic inclusion in South Africa.

When preparing your filing, draft a comprehensive public interest prospectus. This document should outline guaranteed capital investments in local facilities, commitments to source materials from local small-to-medium enterprises, and clear mechanisms for worker ownership. Structuring these conditions voluntarily before the Commission demands them significantly accelerates the review process and reduces adversarial negotiations.

Why You Must Avoid Implementing the Merger Prior to Clearance

Implementing any aspect of a merger before receiving official regulatory clearance is a serious statutory violation known as "gun-jumping." The South African competition authorities strictly penalize firms that prematurely integrate operations, share competitively sensitive information, or assume control over a target's strategic decisions.

The administrative penalties for gun-jumping are severe, reaching up to 10% of the merging firms' combined annual global turnover. Beyond financial fines, the Commission can order the unwinding of the transaction, voiding the deal entirely. Foreign acquirers run into this trap most frequently during global acquisitions when they close the parent-level deal worldwide without realizing the South African subsidiary has not yet been legally cleared.

To avoid this, merging parties must establish clean teams and ring-fence sensitive data during the due diligence and pre-closing phases. If the global timeline demands immediate closing, you must negotiate a formal "hold-separate" arrangement. This legally binding carve-out ensures the South African business continues to operate completely independently from the global acquirer until the local Competition Tribunal grants the final clearance certificate.

Coordinating Timelines With Parallel African Antitrust Reviews

Cross-border acquisitions involving South African entities frequently trigger simultaneous merger control requirements in neighboring countries and regional trading blocs. Acquirers must map out all mandatory filing jurisdictions across the continent early to prevent one delayed regulatory review from derailing the global closing schedule.

South Africa is not a member of the COMESA (Common Market for Eastern and Southern Africa) Competition Commission, meaning a COMESA filing does not cover South Africa, and vice versa. If the target firm operates in South Africa as well as COMESA member states like Kenya or Zambia, you must submit separate notifications to both authorities. Furthermore, neighboring countries such as Namibia, Botswana, and Eswatini have their own active, independent competition regulators with unique financial thresholds and review periods.

Managing these parallel reviews requires strategic timeline synchronization. The South African review process for large mergers can take several months due to public interest evaluations and required Tribunal hearings. Acquirers should draft a master regulatory timeline that accounts for the longest statutory review period among the triggered African jurisdictions, ensuring no local implementation occurs anywhere before the respective national authority gives the green light.

Common Misconceptions About South African Merger Control

A lack of physical presence exempts foreign firms from filing. Many foreign acquirers mistakenly believe that because they do not have offices or incorporated entities in South Africa, local merger control does not apply. South African competition law operates on an "effects" basis. If the foreign acquiring firm generates sales by exporting into South Africa and meets the financial thresholds, mandatory notification is required.

Public interest conditions are only recommendations. Foreign dealmakers sometimes assume that employment and empowerment commitments are negotiable formalities. In reality, public interest conditions are legally binding constraints. The Competition Tribunal actively monitors compliance post-merger, and failing to uphold a job preservation commitment or empowerment quota can result in immediate fines or the revocation of the merger approval.

Global integration can begin as long as the local entity is left alone. Some companies believe they can merge global IT systems, rebrand, or change regional leadership structures prior to local clearance, provided they do not touch the South African operations. Regulators often view these overarching integration steps as premature changes in control. Strict hold-separate protocols must be formalized and observed to avoid gun-jumping allegations.

Frequently Asked Questions

What are the filing fees for a merger in South Africa?

Merger filing fees are tiered based on the size of the transaction. Currently, the fee for an intermediate merger is R165,000, while the fee for a large merger is R550,000. These fees must be paid directly to the Competition Commission upon submission of the filing.

How long does the merger review process take?

The initial review period for an intermediate merger is 20 business days, which the Commission can extend by an additional 40 days. Large mergers require a recommendation from the Commission followed by a hearing at the Competition Tribunal, a process that frequently takes between three to six months to conclude.

Do we have to notify trade unions before filing for a merger?

Yes, the Competition Act strictly requires merging parties to serve a non-confidential version of the merger notification on recognized trade unions or employee representatives. This must be done before the formal filing is submitted to the Commission, ensuring workers have the opportunity to participate in the public interest assessment.

Can the Competition Tribunal block a deal solely over job losses?

Yes. The Tribunal has the authority to prohibit a transaction entirely if it determines the merger will result in unjustifiable, substantial job losses, even if the deal raises no competitive or antitrust concerns.

When to Hire an Antitrust Lawyer

Engaging specialized local legal counsel is vital the moment a foreign acquiring firm begins evaluating a target with operations, sales, or assets in South Africa. Because local merger control requires complex calculations of domestic turnover and delicate negotiations regarding broad-based empowerment, standard international M&A counsel cannot navigate these local nuances alone. You should retain a lawyer immediately to handle trade union notifications, draft public interest commitments, and ensure strict compliance with anti-gun-jumping protocols during the global due diligence phase.

Next Steps for Foreign Acquirers

Your first step is to execute a comprehensive jurisdictional assessment to determine if your global transaction triggers South African notification thresholds. Next, audit the target company's current employment statistics and empowerment rating to build the foundation of your public interest strategy. Finally, work with specialized antitrust litigation lawyers in South Africa to draft your formal notification and design a legally compliant hold-separate agreement to protect your global closing timeline.