Florida Real Estate Contracts: 2026 Dispute Prevention Guide

Key Takeaways

Navigating Florida real estate as a foreign buyer requires strict attention to contract deadlines, tax withholding rules, and fund transfer logistics to prevent costly legal disputes. Taking proactive, documented steps before signing an agreement ensures your investment and earnest money deposits remain protected.

- Contract Deadlines are Absolute: Missing a financing or inspection deadline by even one day under Florida's "time is of the essence" standard can result in the immediate loss of your deposit.

- FIRPTA Liability Falls on Buyers: If you purchase property from a foreign seller without properly withholding IRS taxes, you can be held financially liable for their tax debt.

- Pre-Litigation Mediation is Mandatory: The standard Florida real estate contract requires parties to attempt mediation before filing any lawsuit over a breached contract.

- Cross-Border Transfers Require Extra Time: International wire transfers and anti-money laundering (AML) compliance checks frequently delay closings, necessitating longer built-in contract timelines.

Common Legal Pitfalls in Standard Florida "As-Is" Contracts

The standard Florida Realtors/Florida Bar "As-Is" Residential Contract places strict, unforgiving deadlines on the buyer for inspections, financing approvals, and closing dates. Missing these specific timelines is the most common way foreign buyers accidentally breach the contract and risk losing their earnest money deposit.

While the "As-Is" contract is the standard in Florida, it heavily favors sellers if buyers do not carefully monitor their contingency periods. To prevent disputes, buyers must pay close attention to three critical clauses:

- The 15-Day Inspection Period: By default, buyers have 15 days to inspect the property and cancel for any reason. If you negotiate repairs or fail to cancel in writing before this period expires, you forfeit your right to walk away with your deposit intact.

- Time is of the Essence Clause: Unlike jurisdictions where closing dates are flexible estimates, Florida contracts treat deadlines as absolute. If international funds fail to clear the title company's escrow account by the closing date, the seller can instantly declare a default.

- Financing Contingencies: Foreign nationals often require specialized cross-border mortgages. If your contract includes a financing contingency, you must obtain formal loan approval within the designated timeframe (usually 30 days) or manually notify the seller in writing to cancel the contract before that deadline passes.

Required Documentation Checklist for Cross-Border Funds and Title Clearance

Clearing title and transferring funds internationally requires verifiable identification, proof of funds tracing, and translated corporate documents if buying through a foreign entity. Preparing these documents well before closing prevents transaction delays, escrow disputes, and anti-money laundering compliance flags.

Title companies and closing attorneys in the United States must comply with strict federal regulations regarding international cash transfers. To prevent your funds from being frozen or rejected, prepare the following documents before executing a contract:

- Certified Identification: Two forms of valid ID, including an unexpired passport with current U.S. entry stamps or visas.

- Translated Proof of Funds: Certified bank statements from your home country, translated into English and converted to U.S. Dollars (USD), proving you have the liquidity to close.

- Wire Transfer Tracing: Documentation showing the exact origin of the funds. Title companies will not accept third-party wire transfers; the money must come from an account bearing the exact name of the buyer listed on the contract.

- Foreign Entity Paperwork: If purchasing the property through a foreign corporation or LLC to mitigate estate taxes, you must provide officially translated articles of incorporation, a certificate of good standing, and a corporate resolution authorizing the specific purchase.

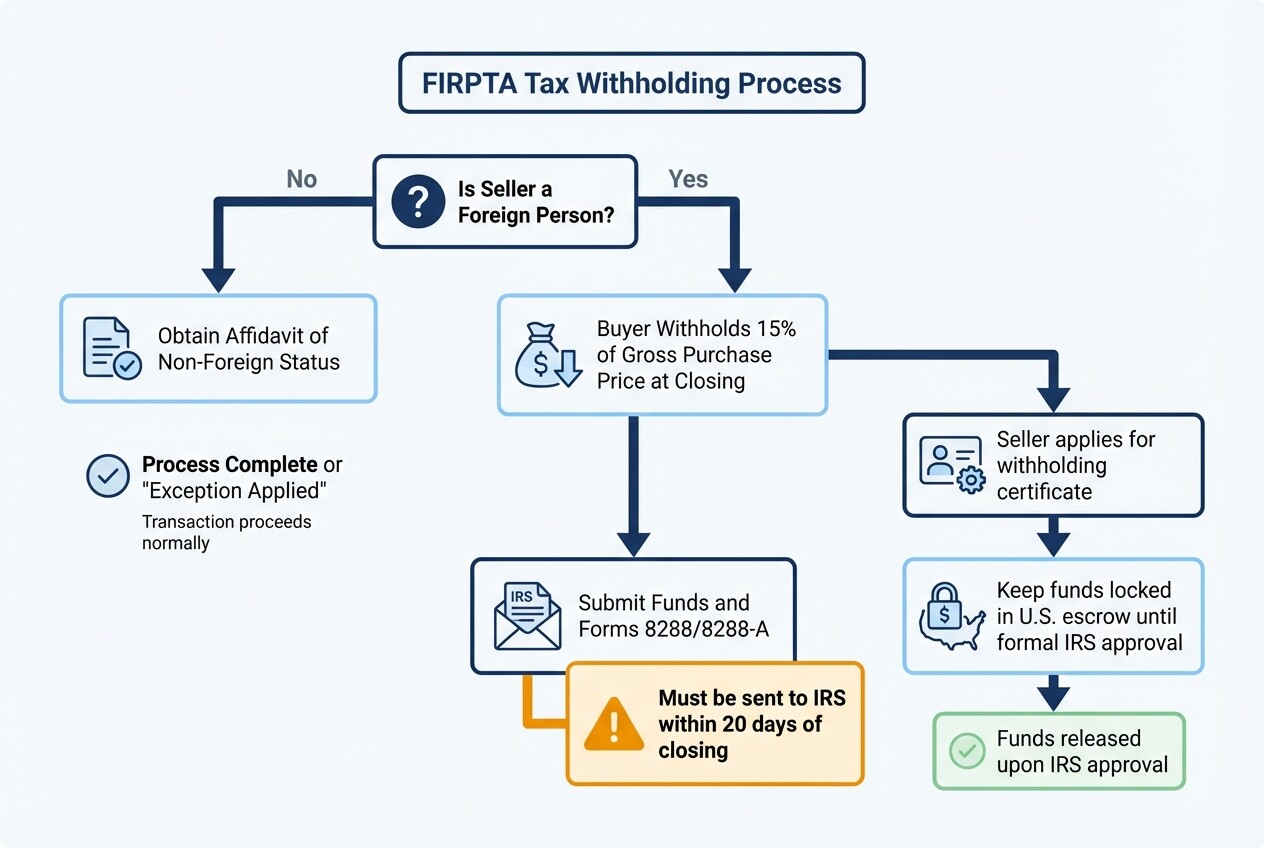

Understanding FIRPTA Tax Withholding Rules

The Foreign Investment in Real Property Tax Act (FIRPTA) requires buyers to withhold up to 15% of the property's gross purchase price when buying from a foreign seller and remit it directly to the IRS. Failure to verify the seller's residency status and handle this withholding properly can make you, the buyer, legally liable for the seller's unpaid taxes.

Many buyers mistakenly believe that FIRPTA only applies if the buyer is foreign. In reality, FIRPTA is entirely dependent on the seller's tax status. To prevent a post-closing dispute with the federal government:

- Require the seller to sign a legally binding Affidavit of Non-Foreign Status confirming they are a U.S. taxpayer.

- If the seller is a foreign person, instruct your closing agent to withhold the 15% from the seller's proceeds at closing.

- Ensure the closing agent remits the funds along with Forms 8288 and 8288-A to the Internal Revenue Service within 20 days of the closing date.

- If the seller applies for a withholding certificate to reduce the 15% penalty, ensure the funds remain locked in a U.S. escrow account until the IRS issues formal approval.

Alternative Dispute Resolution in Florida Real Estate

Florida real estate contracts typically mandate pre-litigation mediation before either party can file a civil lawsuit over a contract breach. This alternative dispute resolution (ADR) method forces buyers and sellers to negotiate a settlement with a neutral third party, frequently resolving issues while saving thousands in legal fees.

Mediation is highly effective in Florida real estate disputes, particularly concerning earnest money disagreements or undisclosed property defects. The process follows a specific pre-litigation protocol:

- The Demand for Mediation: Once a dispute arises, either party can send a formal written demand for mediation. Under the standard contract, the parties then have 10 days to agree on a qualified mediator.

- Shared Costs: The cost of the mediator-typically ranging from $250 to $500 per hour-must be split equally between the buyer and the seller.

- Settlement Leverage: For foreign buyers, invoking mandatory mediation effectively ties up the property. A seller cannot safely sell the home to another buyer while an active mediation demand over the contract is pending, providing strong leverage to secure the return of your deposit.

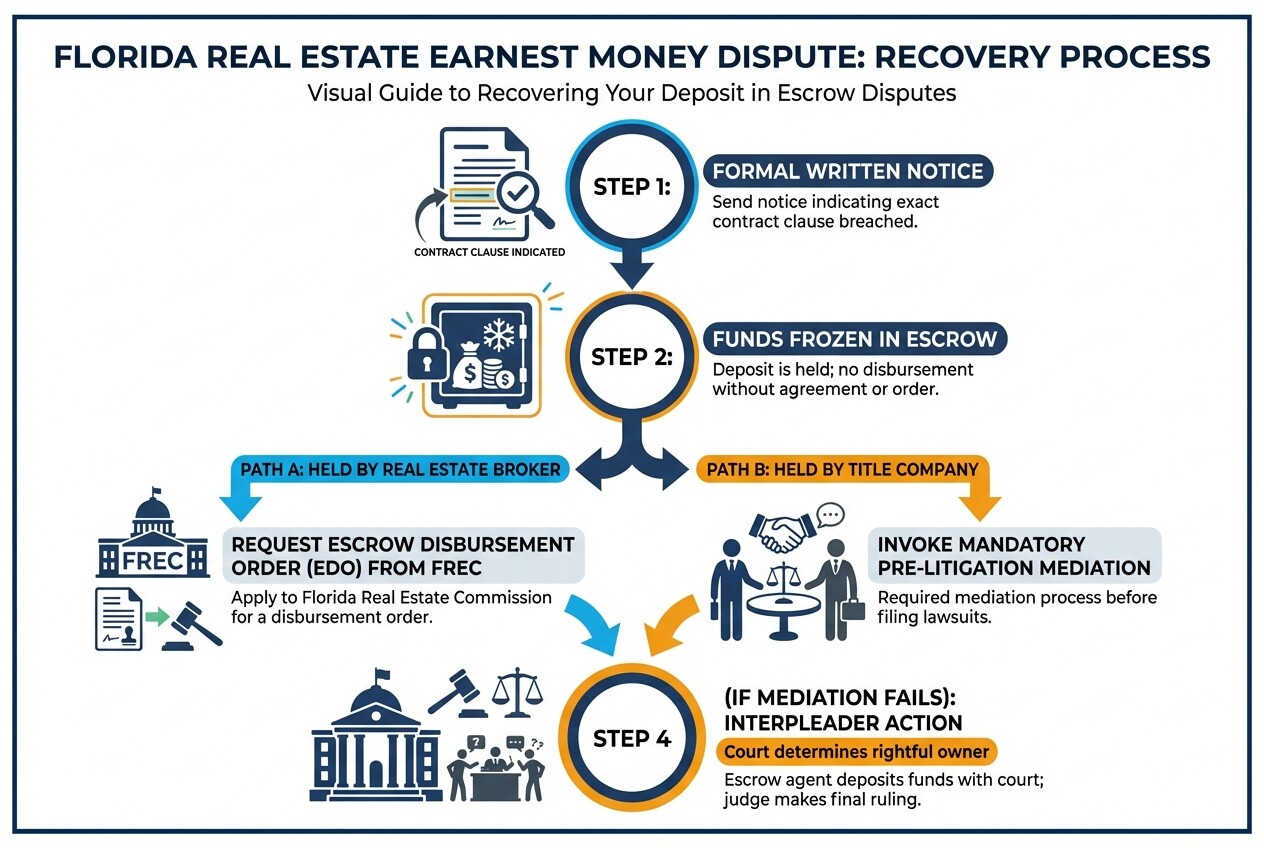

Recovering Earnest Money Deposits During Escrow Disputes

To recover your earnest money deposit when a real estate deal collapses, you must send a formal written notice of cancellation before your specific contract contingency periods expire. If the seller disputes the return of your funds, the title company must hold the money in escrow until both parties sign a mutual release or a legal authority issues a ruling.

Title companies in Florida are neutral third parties and will never release disputed funds simply because one side demands it. If your deposit is trapped in escrow, follow these legal steps to recover it:

- Send Formal Written Notice: Notify the seller and escrow agent in writing of the exact contract clause (e.g., failed inspection, denied financing) that entitles you to a refund.

- Request an Escrow Disbursement Order (EDO): If your funds are held by a licensed Florida real estate brokerage rather than a title company, the broker can request an EDO from the Florida Real Estate Commission (FREC), which will review the contract and direct who gets the funds.

- Invoke Mediation: If a title company holds the funds, immediately invoke the mandatory mediation clause outlined in the standard contract.

- Prepare for an Interpleader Action: If mediation fails, the title company will file an "interpleader" action, depositing your earnest money with the local county court and removing themselves from the dispute. The court will then determine the rightful owner.

Common Misconceptions About Buying Florida Real Estate

Foreign buyers frequently misunderstand Florida's disclosure laws and contract contingencies, leading to entirely preventable pre-litigation disputes. Relying on real estate practices and legal standards from your home country can put your transaction and escrow funds at severe risk.

- Misconception: "As-Is" means the seller does not have to disclose hidden defects. Fact: Under Florida law, sellers of residential property must disclose all known material defects that affect the property's value and are not readily observable, regardless of an "As-Is" clause.

- Misconception: If my international wire transfer is delayed, I can easily extend the closing date. Fact: Due to the "time is of the essence" provision, a seller is under no obligation to grant an extension. If your funds arrive a day late, the seller can cancel the contract and claim your earnest money deposit as liquidated damages.

- Misconception: The title company represents my legal interests. Fact: Title companies and closing agents are strictly neutral parties hired to execute the contract terms. They cannot offer you legal advice, negotiate on your behalf, or advocate for you during an escrow dispute.

Frequently Asked Questions

What makes a real estate contract legally binding in Florida?

A Florida real estate contract becomes fully binding when it is signed by both the buyer and the seller, and the fully executed agreement is delivered back to the buyer. While an earnest money deposit is typically required to demonstrate good faith, it is the signature and delivery that create the legal obligation.

Can a foreign national buy property in Florida without being physically present?

Yes, foreign nationals can complete a real estate purchase from abroad using a Remote Online Notarization (RON) service or by granting a specific Power of Attorney (POA) to a trusted representative in the United States, provided the title company and lender approve the specific method beforehand.

Who pays for mediation in a Florida real estate dispute?

Under the standard Florida Realtors/Florida Bar contract, the buyer and seller must equally split the cost of the mediator and the mediation facility, regardless of who initiated the dispute or who is ultimately found to be at fault.

When to Hire a Lawyer

Retaining a Florida real estate attorney before signing the initial purchase offer is the most effective way to prevent costly pre-litigation disputes. You should immediately engage legal counsel if you face a looming escrow dispute, uncover hidden title defects, or need to navigate complex cross-border tax withholding requirements.

Because standard real estate agents cannot legally modify contract language to protect foreign assets, engaging a legal professional ensures your contingencies are bulletproof. You can browse qualified real estate dispute prevention lawyers in the United States to review your documents before your deposit becomes non-refundable.

Next Steps

Protecting your real estate investment in Florida starts with proactive contract review and assembling your legal and financial team well in advance. Taking decisive action before making an offer minimizes your risk of escrow loss or unexpected closing delays.

- Verify Your Funds: Convert and consolidate your purchase funds into a single, easily traceable account that complies with U.S. anti-money laundering regulations.

- Interview Legal Counsel: Hire a Florida-licensed real estate attorney to draft an addendum protecting you from international wire delays.

- Investigate Seller Status: Ask your real estate agent to verify upfront whether the seller is a foreign national to anticipate potential FIRPTA withholding complications.