- Multinational subsidiaries in India must comply with the Business Responsibility and Sustainability Reporting (BRSR) framework if they meet SEBI's market capitalization thresholds.

- Starting in the 2024-2025 financial year, the "BRSR Core" mandates reasonable assurance for the top 1,000 listed entities and their significant value chain partners.

- Directors of Indian subsidiaries face personal legal liability under Section 166 of the Companies Act, 2013, for failing to consider environmental and social impacts.

- Global ESG reporting standards like GRI or SASB do not automatically satisfy Indian legal requirements; specific mapping to SEBI's nine principles is mandatory.

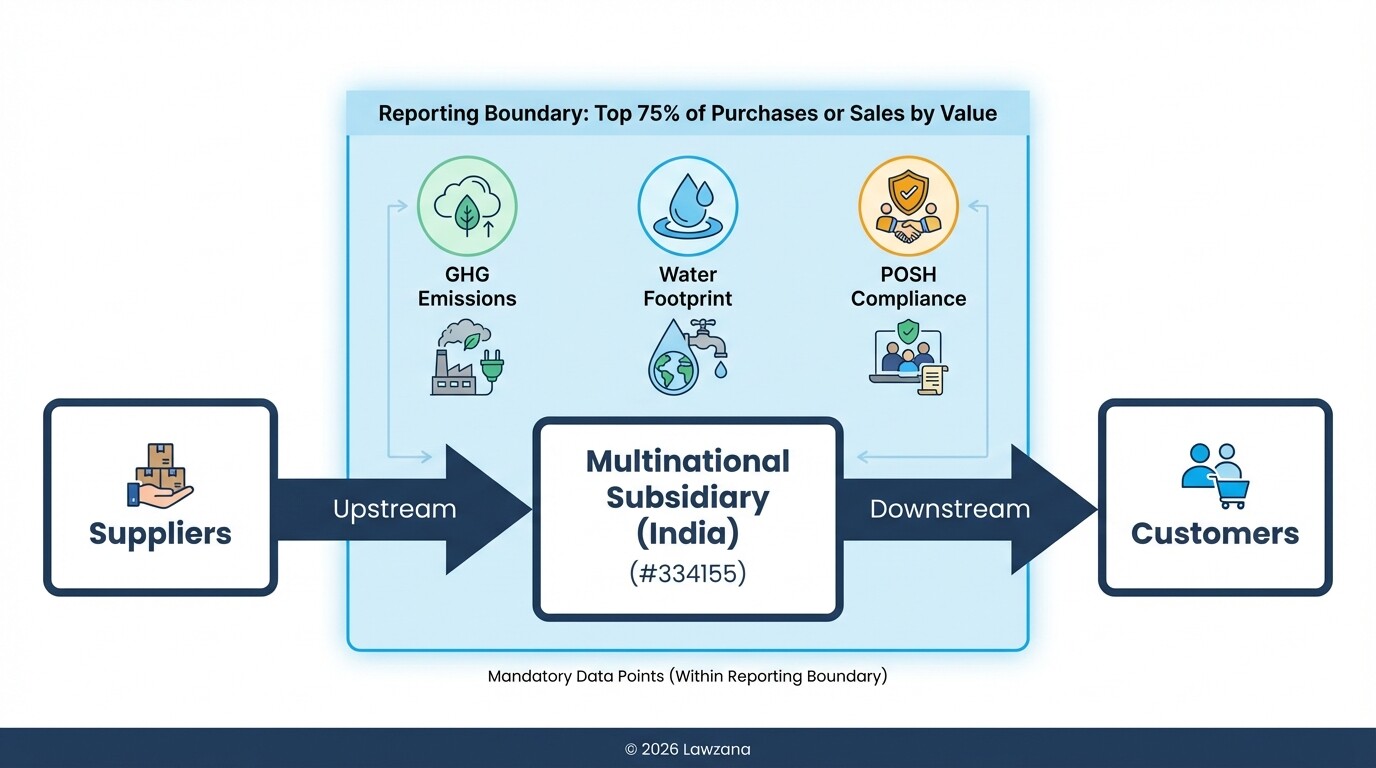

- Effective supply chain transparency now requires documented ESG disclosures from vendors and suppliers representing at least 75% of the subsidiary's purchases or sales.

ESG Compliance Readiness Checklist for 2026

Indian regulatory oversight for ESG is transitioning from voluntary disclosure to mandatory assurance. This checklist helps multinational subsidiaries ensure their internal systems are prepared for the 2026 reporting cycle.

| Compliance Action | Responsibility | Deadline |

|---|---|---|

| Identify Reporting Tier: Determine if the subsidiary or its listed parent falls within the Top 1,000 entities by market cap. | Finance/Legal | Q1 2025 |

| BRSR Core Gap Analysis: Evaluate current data collection against the 9 key performance indicators (KPIs) mandated for "Reasonable Assurance." | Sustainability Lead | Q2 2025 |

| Value Chain Mapping: Identify suppliers and customers constituting the top 75% of transactions by value for ESG screening. | Procurement | Q3 2025 |

| Internal Control Audit: Implement digital tracking for energy consumption, water usage, and waste management to ensure data auditability. | IT/Operations | Q4 2025 |

| Director Sensitization: Conduct board-level training on Section 166 duties and SEBI's ESG disclosure requirements. | Board Secretary | Q1 2026 |

| Third-Party Assurance: Engage a SEBI-recognized assurance provider to verify BRSR Core disclosures. | Audit Committee | Q2 2026 |

Business Responsibility and Sustainability Reporting (BRSR) in India

The Business Responsibility and Sustainability Reporting (BRSR) framework is a mandatory disclosure mechanism regulated by the Securities and Exchange Board of India (SEBI). It requires companies to report their performance against nine principles of the National Guidelines on Responsible Business Conduct (NGRBC), covering ethics, employee well-being, and environmental stewardship.

While the mandate primarily targets the top 1,000 listed companies, many multinational subsidiaries are pulled into the compliance net because they act as material subsidiaries or belong to the "Value Chain" of a listed entity. The BRSR is divided into "Essential Indicators," which are mandatory, and "Leadership Indicators," which remain voluntary but are increasingly expected by institutional investors.

For the 2026 cycle, the "BRSR Core" becomes the focal point. This is a sub-set of the broader BRSR consisting of specific KPIs (such as greenhouse gas emissions, water footprint, and gender diversity) that require "reasonable assurance" by an independent auditor. This move from "comply or explain" to mandatory verification marks a significant shift in India's regulatory landscape.

Documentation Required for Supply Chain Transparency

Supply chain transparency in India is no longer limited to financial audits; it now encompasses the environmental and social footprints of a company's value chain. Multinational subsidiaries must document the ESG performance of their "Value Chain Partners," which include entities upstream and downstream that account for 75% of the company's purchases or sales.

To demonstrate compliance, companies should maintain a comprehensive ESG Evidence File containing:

- Supplier Code of Conduct: Signed agreements where vendors commit to labor laws, anti-corruption, and environmental standards.

- Resource Consumption Logs: Documented data from suppliers regarding energy and water intensity associated with the products provided.

- Social Impact Certificates: Records of "Prevention of Sexual Harassment" (POSH) compliance and Minimum Wage Act adherence within the supplier's workforce.

- Disaster Management Plans: Evidence that key suppliers have climate-resilient operational plans in place.

Under the Securities and Exchange Board of India regulations, subsidiaries must report these metrics specifically for their Indian operations, even if the parent company maintains a global sustainability report.

Aligning Global ESG Standards with Indian Law

Multinational corporations often use Global Reporting Initiative (GRI) or Task Force on Climate-related Financial Disclosures (TCFD) frameworks, but these do not substitute for Indian BRSR filings. While there is significant overlap, Indian law requires data to be formatted according to the Nine Principles of the National Guidelines on Responsible Business Conduct.

The following table illustrates how global standards map to Indian-specific requirements:

| Global Framework (GRI/SASB) | Indian BRSR Equivalent | Key Local Nuance |

|---|---|---|

| GHG Emissions (Scope 1, 2, 3) | Principle 6 (Environment) | Must include specific intensity ratios relative to Indian turnover. |

| Labor Practices & Human Rights | Principle 3 (Employees) & 5 (Human Rights) | Mandatory reporting on POSH (Sexual Harassment) and Differently Abled employees. |

| Community Investment | Principle 8 (Inclusive Growth) | Must align with mandatory Corporate Social Responsibility (CSR) spending (2% of net profit). |

| Anti-Corruption | Principle 1 (Ethics & Transparency) | Requires reporting on "Business Conduct" complaints filed with Indian authorities. |

Subsidiaries should perform a "cross-walk" analysis to ensure that data collected for global headquarters is repurposed and localized to meet the granular requirements of the Ministry of Corporate Affairs.

Legal Risks of Non-Compliance for Board Directors

In India, ESG compliance is not merely a reporting obligation but a matter of fiduciary duty. Section 166 of the Companies Act, 2013, explicitly states that a director must act in good faith to promote the objects of the company for the benefit of its members, the community, and the protection of the environment.

The legal risks for directors of multinational subsidiaries include:

- Personal Liability: Failure to oversee ESG disclosures can be interpreted as a breach of fiduciary duty, leading to fines and potential disqualification.

- Greenwashing Litigation: Providing misleading information in BRSR filings can result in SEBI penalties and "Class Action" suits under Section 245 of the Companies Act.

- Regulatory Penalties: SEBI has the authority to impose significant monetary penalties on the company and its compliance officers for inaccurate or delayed BRSR Core submissions.

- Operational Stoppage: Non-compliance with environmental norms (Principle 6) can lead to the withdrawal of "Consent to Operate" by State Pollution Control Boards.

Steps for Conducting an Internal ESG Audit in 2026

An internal ESG audit is a systematic review of a subsidiary's data collection and reporting processes to ensure they withstand external scrutiny and regulatory assurance.

- Define the Reporting Boundary: Clearly establish which Indian entities, plants, and value chain partners fall within the audit scope.

- Standardize Data Collection: Move from manual spreadsheets to a centralized ESG ERP system to ensure data integrity and a clear audit trail.

- Internal Control Testing: Test the accuracy of meters (energy/water) and the validity of human resources data (diversity/wages) against primary source documents.

- Gap Remediation: Identify areas where the subsidiary falls short of "Reasonable Assurance" standards and implement corrective actions before the final filing.

- Simulated Assurance Review: Engage internal audit teams to perform a "mock audit" using the same criteria that an external SEBI-authorized auditor would apply.

Common Misconceptions About Indian ESG Compliance

Misconception 1: "Our global sustainability report covers our Indian operations." Global reports often aggregate data, which obscures the specific performance of the Indian subsidiary. SEBI requires standalone or consolidated disclosures specifically for the Indian entity, following the BRSR format. Global templates generally lack the "CSR" and "POSH" data required by Indian law.

Misconception 2: "ESG is only for public companies, and we are a private subsidiary." While the BRSR mandate currently targets listed entities, it indirectly impacts private subsidiaries in two ways. First, if the subsidiary is a "material" component of a listed parent, its data must be included. Second, as a value chain partner to other large Indian companies, the subsidiary will be contractually required to provide ESG disclosures.

FAQ

Is BRSR mandatory for unlisted multinational subsidiaries?

It is not mandatory for unlisted subsidiaries to file a standalone BRSR with SEBI. However, they must provide ESG data to their listed parent companies or customers who are within the top 1,000 listed entities, as these entities must report on their value chain.

What is the "BRSR Core"?

The BRSR Core is a specific set of nine ESG themes (such as Greenhouse Gas emissions and Job creation) that require a higher level of verification called "Reasonable Assurance." It is designed to provide investors with high-confidence data.

Who is authorized to provide ESG assurance in India?

Assurance must be provided by an independent third party with expertise in ESG. While many accounting firms provide this service, SEBI ensures that the assurance provider does not have a conflict of interest with the company's statutory auditor.

When to Hire a Lawyer

Navigating India's ESG landscape requires legal intervention when:

- You are drafting "Value Chain Partner" agreements that include ESG indemnity clauses.

- You face a "Greenwashing" investigation or an inquiry from SEBI regarding BRSR disclosures.

- You need to interpret how Section 166 of the Companies Act applies to specific board decisions involving environmental trade-offs.

- You are structuring an acquisition and need to perform ESG legal due diligence on a target's Indian operations.

Next Steps

- Perform a Scoping Exercise: Determine if your subsidiary falls under the mandatory BRSR or Value Chain reporting requirements for the 2025-2026 period.

- Review Supplier Contracts: Update procurement templates to include mandatory ESG data sharing and compliance clauses.

- Appoint an ESG Compliance Officer: Designate a specific individual responsible for bridging the gap between global headquarters' standards and Indian regulatory requirements.

- Schedule a Board Briefing: Ensure the Board of Directors understands their legal liability regarding ESG under the Companies Act.