- Fiduciary duties are local: Foreign directors of Irish subsidiaries owe strict legal duties directly to the Irish entity under the Companies Act 2014, not just to the foreign parent company.

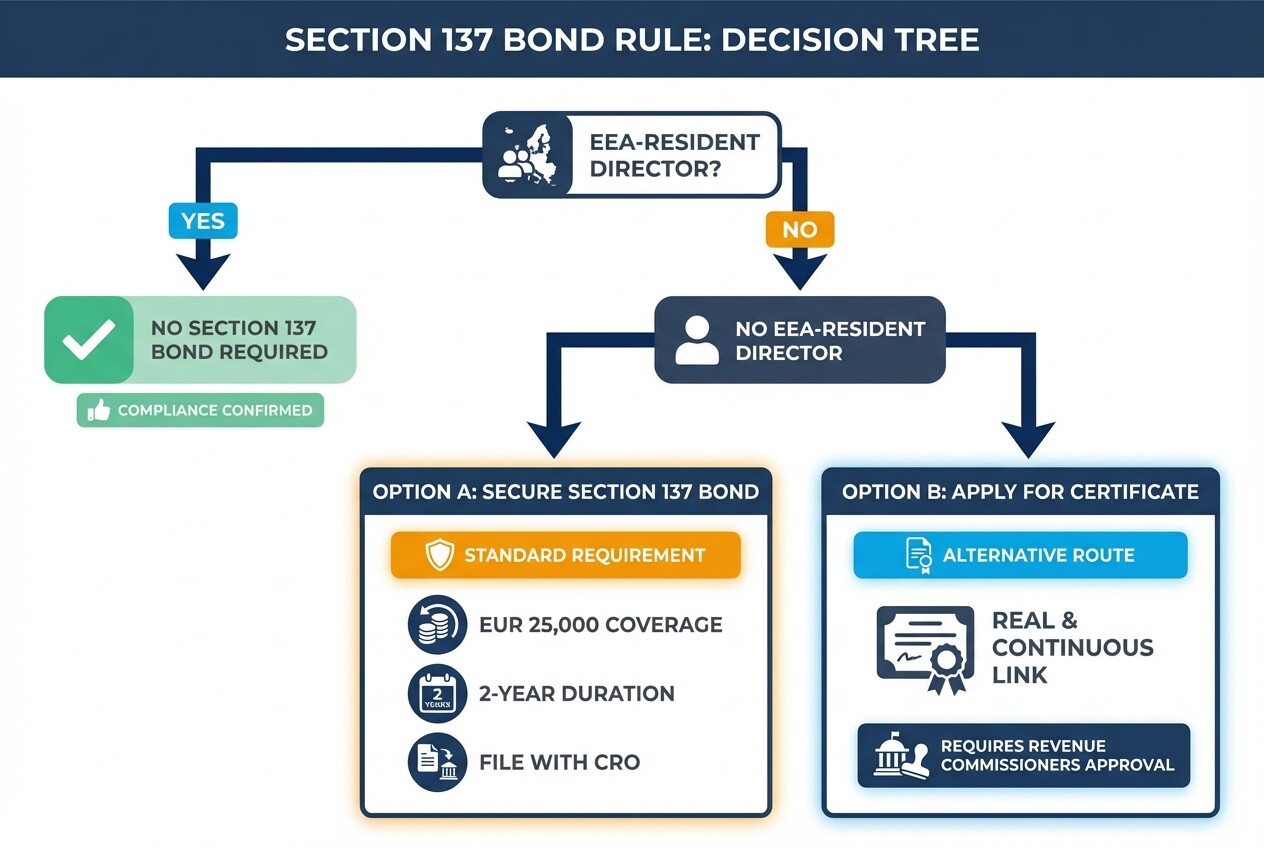

- Non-EEA bonds are mandatory: If your board lacks a resident of the European Economic Area (EEA), you must secure a Section 137 Non-Resident Director's Bond to operate legally.

- Documentation shields liability: Detailed board minutes are your primary defense against personal liability, proving you exercised independent judgment.

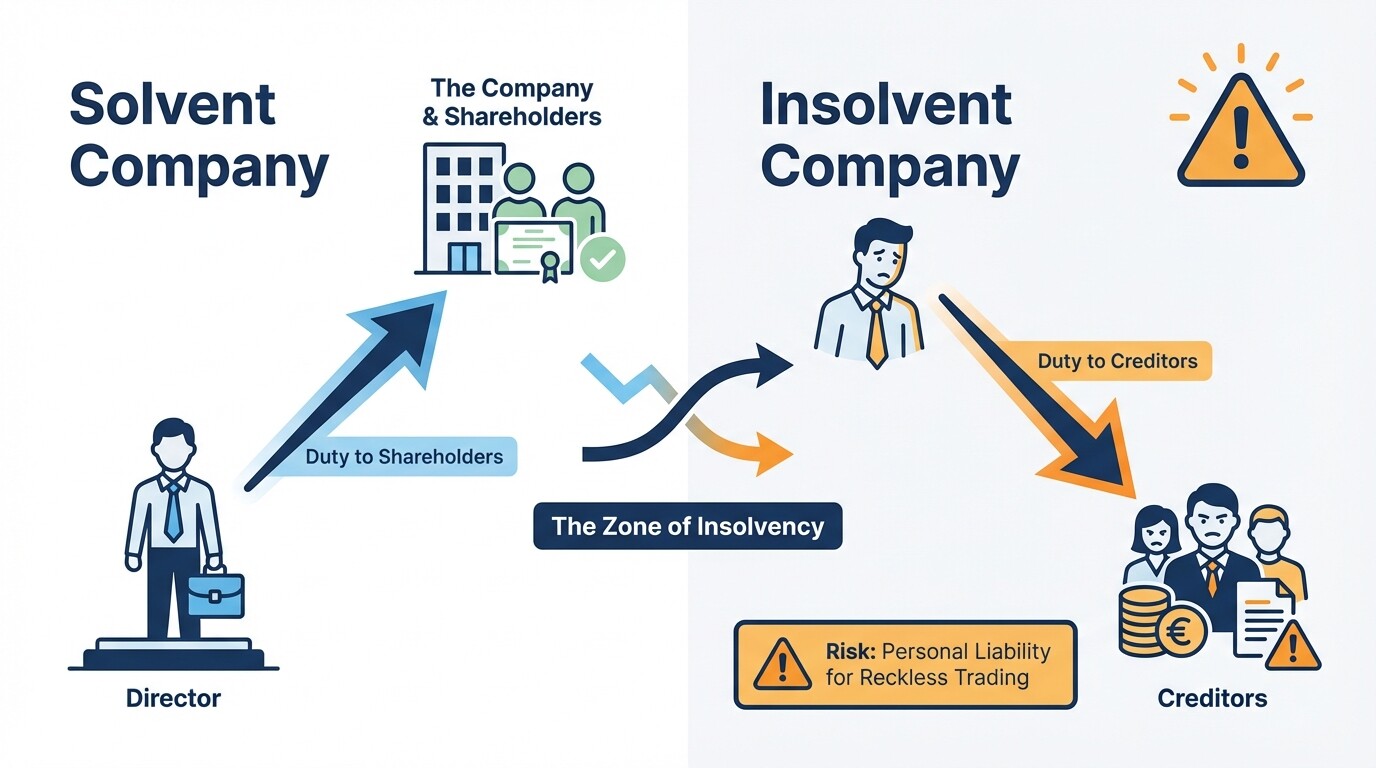

- Insolvency shifts obligations: When an Irish company faces insolvency, directors' duties shift from shareholders to protecting creditors, and failure to act can result in personal liability for corporate debts.

- RBO filings are non-negotiable: Accurate reporting to the Register of Beneficial Ownership is a strict legal requirement, with severe financial penalties for non-compliance.

Fiduciary Duties and Statutory Obligations in Ireland

Under the Irish Companies Act 2014, company directors owe strict fiduciary duties to the company itself, not merely to the shareholders or the parent corporation. These obligations require you to act in good faith, avoid conflicts of interest, and exercise due care, skill, and diligence.

Foreign executives often assume their role on an Irish subsidiary board is a mere formality. However, Irish law makes no distinction between an executive director and a non-executive or "nominee" director. All directors share the same statutory obligations. Section 228 of the Companies Act 2014 explicitly codifies these duties, requiring directors to:

- Act honestly and responsibly in relation to the conduct of the company affairs.

- Act in accordance with the company constitution and exercise powers only for their legally permitted purposes.

- Avoid using company property, information, or opportunities for personal gain.

- Exercise independent judgment rather than blindly following the directives of a foreign parent company.

Failing to uphold these duties can result in restriction orders, disqualification from acting as a director in Ireland, or personal financial liability.

What is the Section 137 Requirement for Non-EEA Directors?

Irish corporate law requires every company to have at least one director resident in the European Economic Area (EEA). If your board consists entirely of non-EEA residents, you must secure a Section 137 Non-Resident Director's Bond to legally incorporate and operate the company.

This requirement ensures that the Irish government has financial recourse if the company fails to pay certain corporate penalties or taxes. The bond must be maintained continuously as long as there is no EEA-resident director on the board. Key details of the Section 137 Bond include:

- Bond Value: The bond provides coverage of EUR 25,000.

- Duration: Bonds are typically issued for a period of two years and must be renewed if the board composition remains unchanged.

- Premium Cost: The actual cost to purchase the bond is usually between EUR 1,000 and EUR 1,500 for the two-year period.

- Filing: The original bond must be filed with the Companies Registration Office (CRO).

An alternative to the bond is obtaining a certificate demonstrating that the company has a "real and continuous link with one or more economic activities" in Ireland, though this requires approval from the Irish Revenue Commissioners and can take months to secure.

Irish Subsidiary Compliance Checklist for Foreign Directors

Managing an Irish subsidiary from abroad requires adherence to strict local timelines and documentation filings. Use this checklist to ensure your foundational corporate governance obligations are met systematically.

| Compliance Task | Timeline | Action Required |

|---|---|---|

| Section 137 Bond | Pre-incorporation or upon EEA director resignation | Secure a EUR 25,000 bond valid for two years if no EEA director is appointed. |

| RBO Filing | Within 5 months of incorporation | Identify and file Ultimate Beneficial Owners with the Central Register. |

| First Annual Return | 6 months post-incorporation | File the first annual return with the CRO (no financial statements required for the first filing). |

| Tax Registration | Immediately post-incorporation | Register for Corporation Tax, VAT, and PAYE/PRSI with Irish Revenue. |

| Statutory Registers | Ongoing | Maintain up-to-date registers of directors, secretaries, and members at the registered office. |

| Board Meetings | At least annually | Hold and document formal board meetings, ensuring minutes reflect independent oversight. |

Shielding Liability Through Proper Board Minutes

Maintaining accurate and timely board minutes is your primary defense against personal liability claims in Ireland. Proper documentation proves that directors exercised independent judgment and engaged in active oversight rather than acting as a rubber stamp for parent company executives.

Irish corporate law mandates that minutes of all board and committee meetings must be entered into the company minute books. For foreign directors, these records are critical during regulatory audits or insolvency proceedings. To properly shield against liability, board minutes should:

- Record dissent: If you disagree with a board decision that you believe is financially risky or legally questionable, explicitly record your dissent in the minutes.

- Demonstrate inquiry: Document the questions asked by directors regarding financial reports, compliance updates, and operational risks.

- Validate parent company directives: Show that the local board independently reviewed and approved directives from the foreign parent company to ensure they were in the best interest of the Irish subsidiary.

- Maintain timely signatures: Ensure the chairperson signs the minutes promptly after the meeting, as unsigned minutes carry little evidentiary weight in Irish courts.

How to Avoid Reckless Trading During Economic Downturns

In Ireland, directors can face unlimited personal liability if they allow a company to continue trading while knowing it cannot pay its debts. This is known as reckless trading, and foreign directors are scrutinized heavily during insolvency proceedings.

When an Irish company becomes insolvent, or is likely to become insolvent, the directors' primary fiduciary duty shifts from the shareholders to the company creditors. Allowing the subsidiary to incur further debt while relying on vague promises of funding from a foreign parent company is a common trap. To avoid reckless trading charges, directors must take immediate action at the first sign of insolvency:

- Hold frequent, minuted board meetings specifically to review cash flow and financial forecasts.

- Seek formal, written assurance from the parent company regarding ongoing financial support.

- Consult immediately with an Irish insolvency practitioner or legal counsel.

- Consider entering SCARP (Small Company Administrative Rescue Process) or examinership to restructure debts legally.

Fulfilling Register of Beneficial Ownership (RBO) Requirements

All Irish companies must identify their ultimate beneficial owners and file this information with the Central Register of Beneficial Ownership (RBO). Failing to complete this filing accurately is a criminal offense that carries severe financial penalties.

A beneficial owner is defined as any natural person who ultimately owns or controls more than 25 percent of the company shares or voting rights, or who exercises control via other means. For complex multinational structures, identifying the individuals at the very top of the corporate chain is mandatory.

- Timeline: Filings must be completed within five months of incorporation.

- Information required: Name, date of birth, nationality, residential address, and a statement of the nature and extent of the interest held.

- PPS Numbers: If a beneficial owner has an Irish Personal Public Service (PPS) number, it must be provided. If not, a Form BEN2 must be completed and notarized.

- Penalties: Non-compliance can result in fines up to EUR 500,000 on indictment and up to 12 months imprisonment.

Common Misconceptions About Irish Corporate Governance

Foreign executives often mistakenly apply their home country legal frameworks to their Irish subsidiaries. Correcting these assumptions early prevents costly regulatory breaches.

- The "Nominee Director" Myth: Many executives believe that acting as a "nominee" for a parent company means they have reduced legal responsibilities. Under Irish law, a director is a director. You owe full fiduciary duties to the Irish company, regardless of who appointed you.

- Tax Residency vs. Corporate Governance: Directors often confuse a company tax residency with its corporate governance requirements. Holding board meetings outside of Ireland may impact the company tax residency status, but it does not diminish your obligations under the Companies Act 2014.

- Parent Company Shields: Assuming the corporate veil of a wealthy foreign parent company protects subsidiary directors from personal liability is a dangerous error. Irish courts can and will hold individual directors personally accountable for reckless trading or severe compliance failures.

Frequently Asked Questions

Does an American director need a work visa to serve on an Irish board?

No. You do not need an Irish work visa or employment permit simply to act as a non-executive director or to attend periodic board meetings in Ireland. However, standard immigration rules apply for entering the country.

Can an Irish subsidiary board hold its meetings outside of Ireland?

Yes, board meetings can legally take place outside of Ireland or via video conference. However, conducting meetings abroad can negatively impact the company ability to prove its "central management and control" is in Ireland, which is crucial for maintaining the 12.5 percent Irish corporation tax rate.

What happens if an Irish company fails to file its annual return?

Failing to file an annual return with the CRO on time results in immediate late filing penalties. Furthermore, the company loses its audit exemption for the next two years, forcing it to pay for a full statutory audit regardless of its size. Continued failure to file can lead to the company being struck off the register.

When to Hire a Lawyer

You should consult local legal counsel before formally accepting a directorship in an Irish subsidiary, especially if the company is navigating complex corporate structures or financial distress. Legal guidance is critical when assessing your personal exposure to risk, drafting parent company support agreements, or initiating insolvency procedures. Do not wait for a regulatory audit or a creditor demand to understand your statutory duties.

Next Steps

To protect yourself and ensure your Irish entity remains compliant, start by reviewing your current board composition to confirm if a Section 137 bond is required. Next, verify that your RBO filings are entirely up to date and accurately reflect the ultimate beneficial owners. Finally, connect with experienced corporate governance lawyers in Ireland to audit your minute books and establish a compliant framework for future board decisions.