- Statutory shield: Examinership provides a court-mandated protection period of up to 100 days (extendable to 150 days) where creditors cannot enforce claims against an Irish company.

- Debtor-in-possession: Unlike UK Administration, the existing board of directors retains control of the subsidiary's day-to-day operations.

- Burden of proof: Entry into the process requires an Independent Expert to state the company has a reasonable prospect of survival as a going concern.

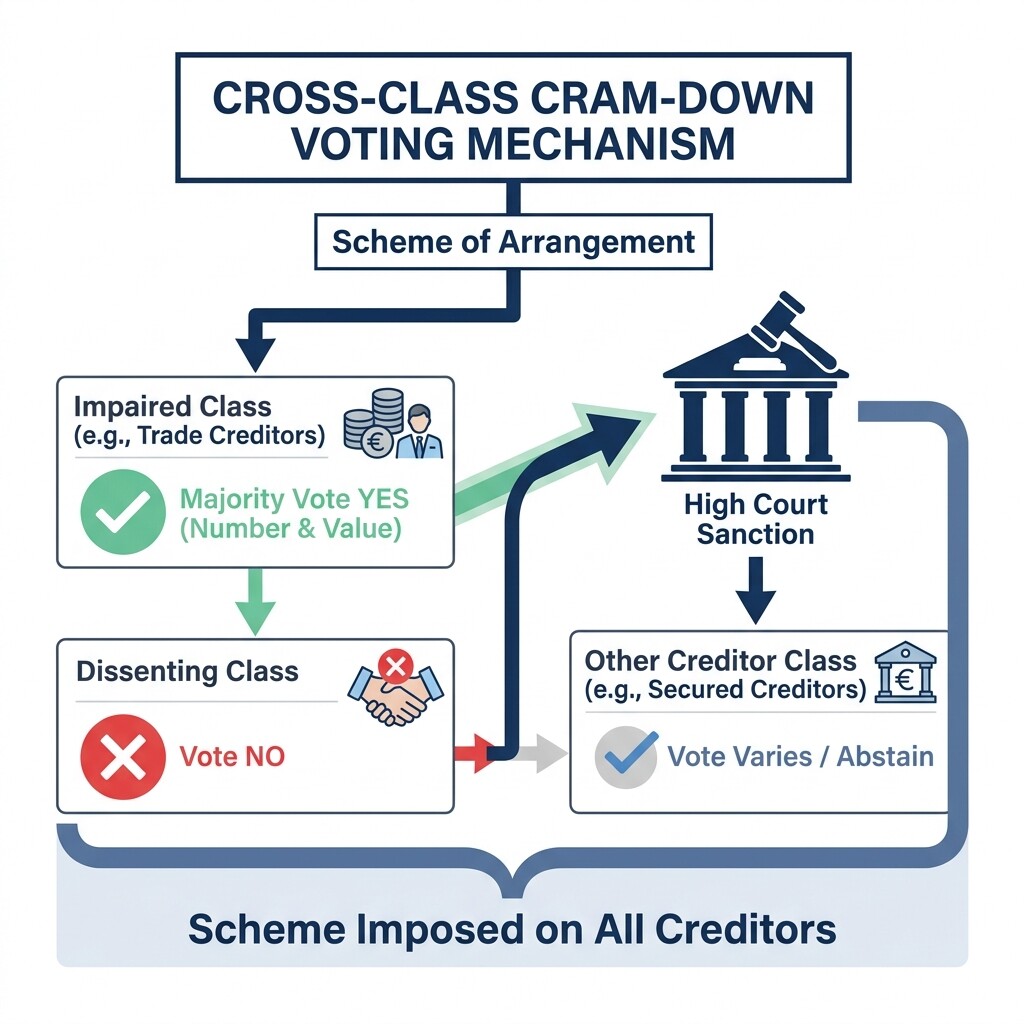

- Cross-class cram-down: The scheme of arrangement can be imposed on dissenting creditors if one impaired class votes in favor of the restructuring plan.

- Ring-fencing risk: Examinership isolates the financial distress of an Irish subsidiary, preventing contagion from spreading to the multinational parent.

The 'Reasonable Prospect of Survival' Legal Test

A company can only enter examinership if the Irish courts are satisfied it has a reasonable prospect of survival as a going concern. This legal threshold prevents insolvent companies from using court protection to delay inevitable liquidation.

To pass this test, the multinational parent must demonstrate that the Irish subsidiary's core business is viable, even if its balance sheet is burdened by legacy debt or temporary cash flow crises. The court requires evidence that a successful restructuring will result in a profitable, self-sustaining enterprise. Restructuring typically involves debt write-downs or fresh investment. The court scrutinizes the reasons for insolvency to ensure the underlying business model is sound.

Appointing an Independent Expert

Before petitioning the court, the company must appoint an Independent Expert to prepare a financial viability report. This report is the foundational evidence to prove the subsidiary can survive.

The Independent Expert is typically an auditor or a senior insolvency practitioner without conflicts of interest from prior engagements. Under the Companies Act 2014, the report must contain specific technical elements:

- Statement of affairs: A breakdown of the company's assets, liabilities, and creditor positions.

- Cash flow forecasts: Projections showing the company has sufficient working capital to survive the examinership period.

- Conditions for survival: Explicit recommendations on what must happen to save the business, such as specific debt haircuts or capital injections.

- Liquidation comparison: A comparative analysis showing creditors receive a better return through examinership than in immediate liquidation.

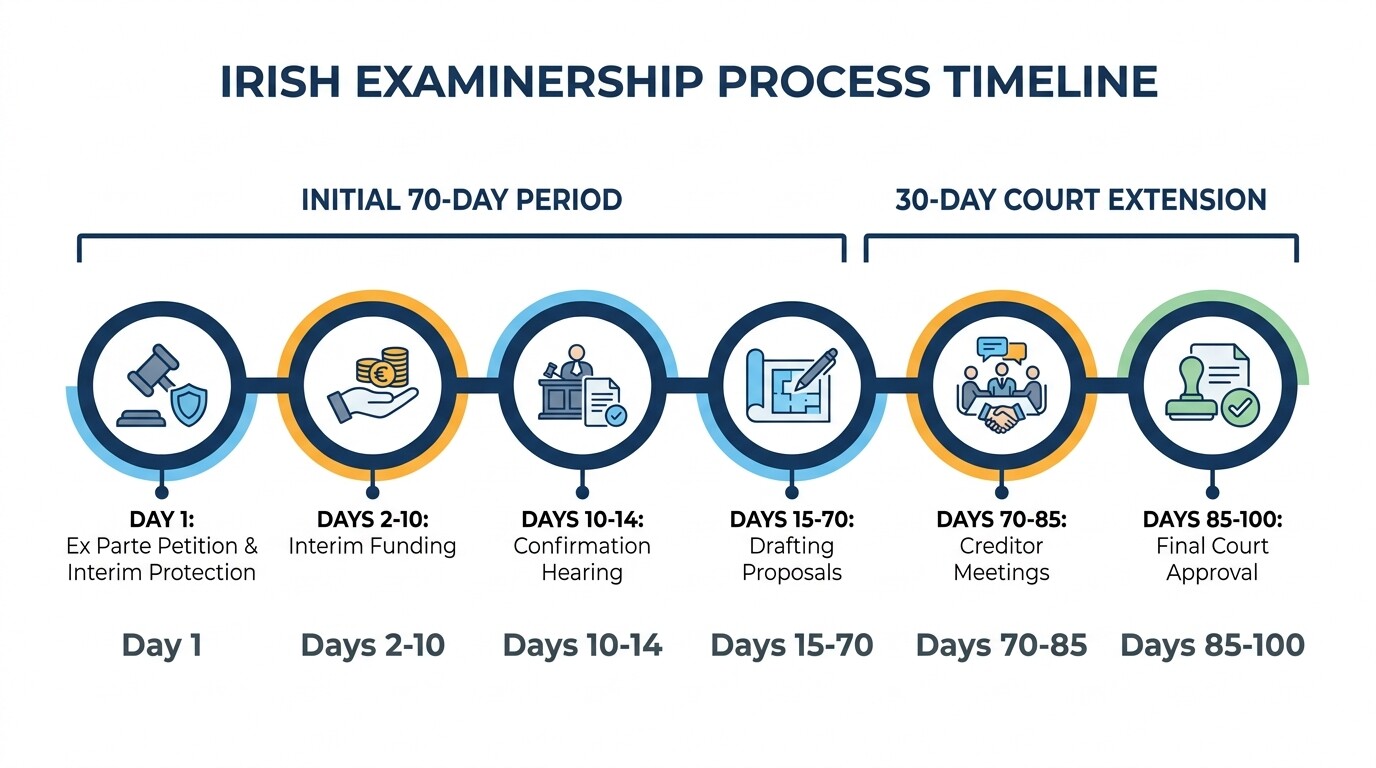

Examinership Timeline

Court protection lasts for a strict 70 days, which the court can extend to a maximum of 100 days (or 150 days under specific extensions). During this period, creditors are barred from appointing receivers, initiating litigation, or executing judgments. Foreign directors must adhere to the following timeline:

| Day | Phase | Description |

|---|---|---|

| 1 | Ex Parte Petition | The company presents the petition and report to the Irish High Court. The court grants interim protection. |

| 2-10 | Interim Funding | The parent ensures the subsidiary has funding to trade. Notices are sent to creditors. |

| 10-14 | Confirmation Hearing | The court holds a full hearing. Creditors can support or object to the appointment. |

| 15-70 | Proposals | The Examiner assesses claims, negotiates with investors, and drafts the scheme. |

| 70-85 | Creditor Meetings | Distinct classes of creditors vote on the restructuring proposals. |

| 85-100 | Court Approval | The Examiner presents the voted scheme for final sanction. It becomes legally binding. |

Drafting the Scheme of Arrangement

The Examiner must formulate a scheme of arrangement that outlines how debts will be restructured across the creditor base. For multinational subsidiaries, this requires balancing intercompany debt owed to the parent, domestic trade creditors, and international lenders.

Drafting the scheme involves grouping creditors into distinct classes based on their legal rights, such as secured lenders and unsecured trade creditors. The scheme usually mandates a significant debt write-down, often referred to as a "dividend," where unsecured creditors might receive a fraction of what they are owed. To pass court scrutiny, the scheme must be fair and equitable. It cannot unfairly prejudice a specific creditor or pay them less than they would receive if the company were liquidated.

The Examiner has statutory powers to repudiate onerous contracts, including commercial property leases, subject to court approval. The landlord's resulting claim for damages is treated as an unsecured claim within the scheme of arrangement.

Creditor Claims and Voting

Creditors vote on the restructuring proposals at statutory meetings convened by the Examiner. The scheme only needs approval from one impaired class of creditors to be presented to the court. An impaired class is any group of creditors whose legal or financial rights are reduced by the plan.

Managing international creditors requires strict adherence to Irish voting mechanics. A class votes in favor of the scheme if a simple majority in both the number of creditors and the value of their claims approve it. The "cross-class cram-down" mechanism allows the court to impose debt write-downs on dissenting creditor classes, provided at least one impaired class accepts the terms.

Secured creditors cannot unilaterally block the appointment of an Examiner if the court believes the company can survive. They can object at the confirmation hearing if they prove the Independent Expert's report is flawed or the process prejudices their security rights. Parent companies often provide fresh equity conditional on the scheme's approval. This incentivizes creditors to vote in favor rather than risk zero return in liquidation.

Common Misconceptions

Foreign executives often approach Irish restructuring with assumptions based on their home jurisdictions. Correcting these misconceptions early prevents strategic errors.

- Management control: Unlike a liquidator or a UK Administrator, the Examiner does not assume executive control. The existing board remains in place to run the daily business, while the Examiner focuses on the financial rescue plan.

- Chapter 11 comparisons: While both are debtor-in-possession models, examinership is faster and less flexible. Irish examinership has a hard statutory deadline, forcing rapid negotiation and resolution.

- Parent company guarantees: Examinership does not automatically extinguish third-party or parent guarantees attached to the subsidiary's written-down debt.

Costs and Cross-Default Risks

Costs vary based on complexity. A High Court examinership for a multinational subsidiary typically exceeds €150,000 in legal and Examiner fees. Smaller subsidiaries may qualify for the Circuit Court, which lowers legal costs, but professional fees remain substantial.

Multinational boards must review their global debt covenants. The insolvency filing of a material subsidiary can trigger technical defaults higher up the corporate chain. This depends entirely on the specific wording of the parent company's global financing agreements.

When to Hire a Lawyer

Parent companies should engage Irish restructuring counsel when a subsidiary projects a cash-flow deficit. The Independent Expert's Report takes several weeks to compile. Waiting for a creditor to issue a winding-up petition jeopardizes the process. Securing restructuring and insolvency lawyers in Ireland early ensures you can control the timeline, select a favorable Independent Expert, and ring-fence the subsidiary's liabilities before value is destroyed.

Next Steps

To initiate a protective restructuring strategy for an Irish subsidiary:

- Conduct a solvency review: Have your general counsel and local directors document the financial shortfall and assess global cross-default risks.

- Secure interim funding: Ensure the multinational parent is prepared to fund the subsidiary's working capital needs for the projected 100-day examinership period.

- Appoint an Independent Expert: Commission the viability report immediately to establish the required legal evidence for court protection.