- A pre-pack administration allows a foreign parent company to swiftly buy back the viable assets of its struggling UK subsidiary, shedding legacy debts in the process.

- A Company Voluntary Arrangement (CVA) focuses on renegotiating terms with existing creditors, allowing the UK subsidiary to keep its current corporate structure and continue trading.

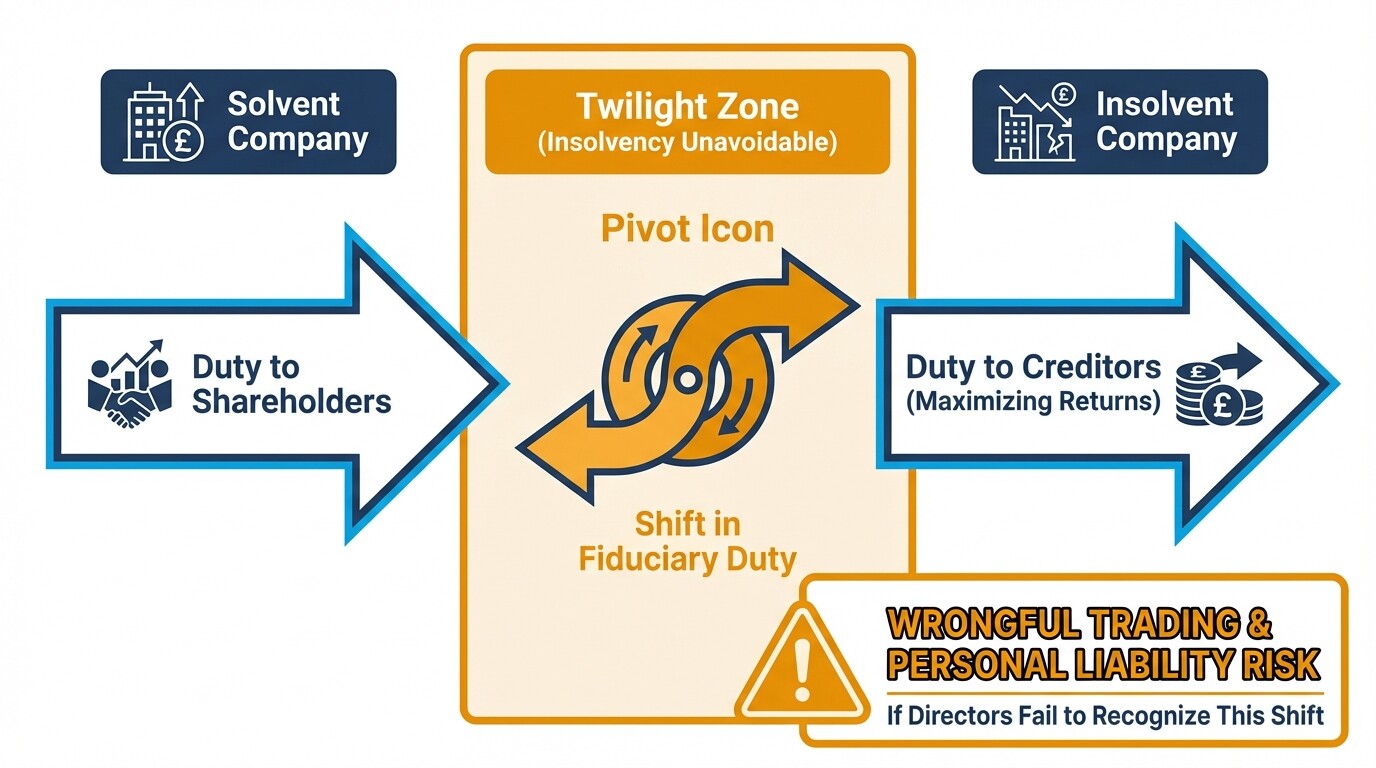

- Foreign directors face strict personal liability risks in the UK if they fail to shift their fiduciary duties toward creditors the moment insolvency becomes unavoidable.

- Protecting parent company intellectual property requires clear licensing agreements that dictate terms upon a subsidiary entering formal insolvency proceedings.

- Recent UK laws prevent suppliers from canceling essential business contracts solely because a subsidiary enters an insolvency process.

Comparing Pre-Pack Administration vs CVA

A pre-pack administration transfers a struggling company's viable assets to a new entity immediately upon an insolvency practitioner's appointment. In contrast, a Company Voluntary Arrangement (CVA) is a legally binding agreement to repay creditors over time while the original company continues trading under existing management.

Choosing the right path depends entirely on the operational viability of the UK subsidiary and the strategic goals of the foreign parent company.

Restructuring Options Comparison Table

| Feature | Pre-Pack Administration | Company Voluntary Arrangement (CVA) |

|---|---|---|

| Primary Goal | Business continuity via a fast asset sale | Debt restructuring and corporate survival |

| Management Control | Transferred to a licensed insolvency practitioner | Retained by existing company directors |

| Execution Timeline | Weeks to negotiate, immediate execution upon filing | 2 to 6 months to draft and approve |

| Creditor Approval | Not required for the asset sale | Requires 75% approval from voting creditors |

| Public Profile | High public scrutiny, requires heavy disclosure | Moderately public, but less disruptive to brand |

| Best Used When | The core business is viable but debt is insurmountable | The company has temporary cash flow issues |

Navigating UK Fiduciary Duties and Wrongful Trading Rules

Under UK law, the moment a director realizes a company cannot avoid insolvent liquidation, their fiduciary duty shifts entirely from protecting shareholders to maximizing returns for creditors. Failing to recognize this shift often leads foreign directors into wrongful trading, resulting in severe personal financial liability.

Foreign executives managing a UK subsidiary often mistakenly operate under the laws of their home country, which can lead to catastrophic regulatory mistakes. The Insolvency Act 1986 strictly governs director conduct during the "twilight zone" of insolvency. If a director continues to trade and incur debt when they should have known the company could not be saved, UK courts can order them to personally contribute to the company's assets.

To avoid wrongful trading and breach of duty claims, foreign directors must:

- Hold frequent, minuted board meetings documenting all financial decisions.

- Continually assess the subsidiary's cash flow and balance sheet solvency.

- Treat all creditors equally, avoiding the prioritization of intercompany debt repayments over third-party suppliers.

- Seek independent professional advice from a UK licensed insolvency practitioner at the first sign of distress.

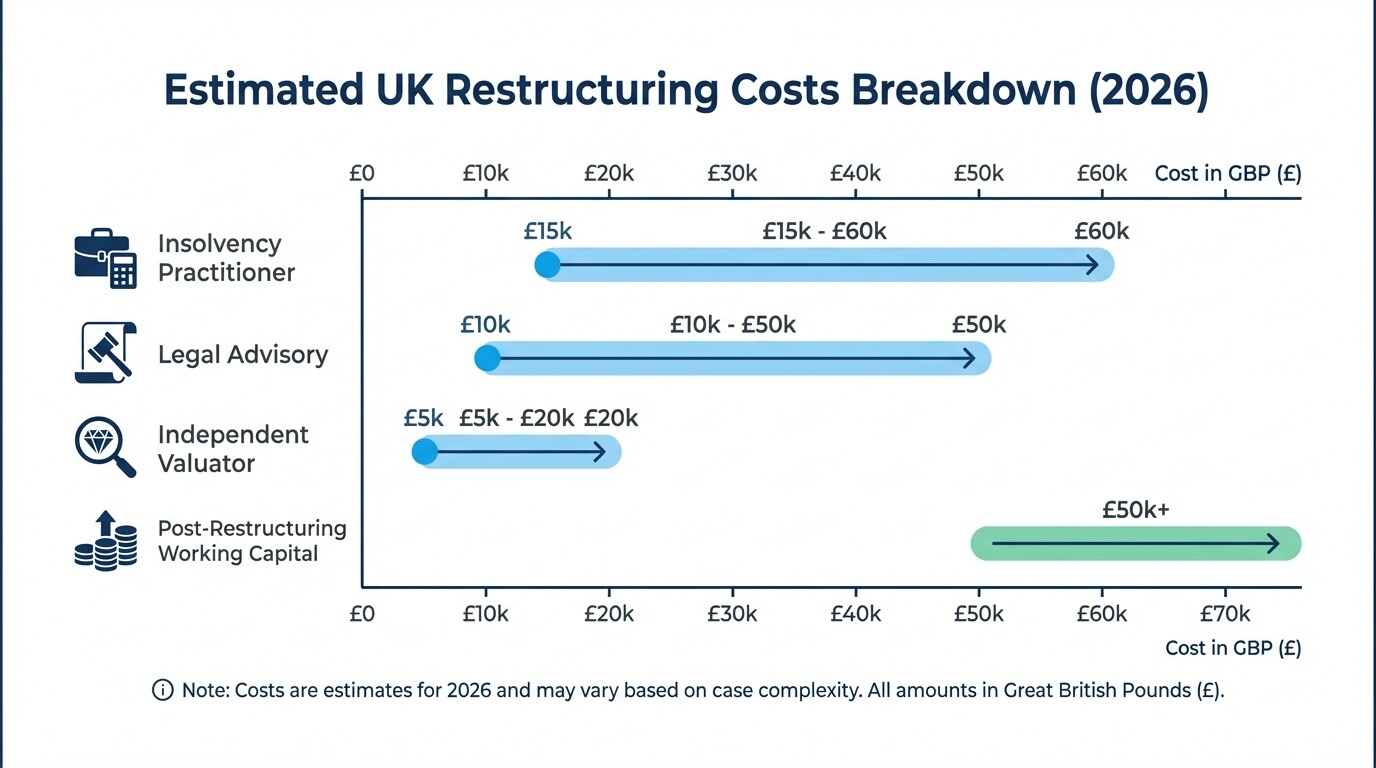

Estimated Restructuring Costs for UK Subsidiaries in 2026

The cost of formally restructuring a UK subsidiary in 2026 ranges from £30,000 to well over £150,000, depending heavily on the complexity of the business, asset valuations, and the chosen legal procedure. Pre-pack administrations generally incur higher upfront fees compared to CVAs due to intensive valuation mandates and complex legal drafting requirements.

When a foreign parent company is budgeting for a UK restructuring, they must account for several distinct professional services. Because the subsidiary is insolvent, the parent company often has to fund these initial costs to secure the desired outcome.

Average Cost Breakdown for 2026:

- Insolvency Practitioner Fees: £15,000 to £60,000 for acting as the administrator or CVA nominee.

- Legal Advisory Fees: £10,000 to £50,000 for drafting sale agreements, reviewing leases, and advising directors on liability.

- Independent Valuator Fees: £5,000 to £20,000. In a pre-pack administration, especially when selling assets back to the parent company, an independent evaluator must verify that the sale price represents the best value for creditors.

- Post-Restructuring Working Capital: £50,000+. If utilizing a pre-pack, the new purchasing entity ("NewCo") must have sufficient operational capital to resume business immediately.

Protecting Cross-Border Assets and Intellectual Property

International parent companies can protect their intellectual property and cross-border assets by structuring them through separate holding companies and utilizing strict licensing agreements. Once a UK subsidiary enters formal insolvency, all assets legally owned by that subsidiary fall under the absolute control of the UK insolvency practitioner.

Foreign parents often make the mistake of leaving patents, trademarks, or critical software code legally domiciled within the UK operating company. To safeguard these assets during a restructuring, parent companies should implement protective measures well before financial distress occurs.

- IP Licensing: Ensure that the parent company owns the core intellectual property and licenses it to the UK subsidiary. The license agreement must include standard clauses that automatically terminate the license upon the subsidiary entering an insolvency procedure.

- Secured Lending: If the parent company provides funding to the subsidiary, it should do so as a secured lender. Registering a debenture with a fixed and floating charge at Companies House ensures the parent company sits higher in the creditor hierarchy if the subsidiary fails.

- Inventory Retention: Supply contracts between the parent and subsidiary should include "Retention of Title" clauses, ensuring physical goods remain the property of the parent until fully paid for.

Managing B2B Contract Terminations and Supplier Disputes

Restructuring often triggers contractual termination clauses, but UK insolvency law restricts suppliers from terminating contracts solely because a company enters an insolvency procedure. This provides a critical breathing space for subsidiaries to maintain essential supplies, software, and utilities while executing a pre-pack or CVA.

Under the Corporate Insolvency and Governance Act 2020, these "ipso facto" clauses hold no legal weight in the UK. Suppliers must continue fulfilling their contracts under existing terms, provided the company in administration or CVA pays for any new supplies going forward. However, managing the commercial reality of these relationships requires careful diplomacy.

To manage supplier disputes during a restructuring:

- Communicate proactively with key vendors to assure them that ongoing post-restructuring orders will be paid.

- Renegotiate critical contracts under the new corporate entity if utilizing a pre-pack administration.

- Understand that while suppliers cannot terminate contracts due to insolvency, they can request permission from the court to terminate if continuing the supply causes them severe financial hardship.

Common Misconceptions About UK Insolvency

Many foreign executives misunderstand UK restructuring frameworks, mistakenly believing that parent companies are automatically liable for subsidiary debts or that they can freely transfer assets out of the UK prior to liquidation.

- Misconception: Pre-packs are a secret way to dump debt. Pre-pack administrations are heavily regulated. When selling assets back to a connected party (like the foreign parent), the administrator must publicly justify the sale through a detailed "SIP 16" report to prove it was the best outcome for creditors.

- Misconception: A CVA protects against foreign creditors. While a CVA binds all unsecured creditors entitled to vote, foreign creditors might attempt to pursue the parent company in their local jurisdiction if cross-border guarantees exist.

- Misconception: You can move cash out right before filing. Transferring funds from the UK subsidiary to the parent company shortly before insolvency is considered a "preference" payment. The UK administrator has the legal power to claw this money back.

Frequently Asked Questions

Can a foreign parent company buy the assets in a UK pre-pack administration?

Yes, a foreign parent company can purchase the business and assets of its insolvent UK subsidiary. However, the transaction must be evaluated by an independent specialist to ensure the purchase price is fair and provides the best possible return for the subsidiary's creditors.

How long does a CVA last in the United Kingdom?

A Company Voluntary Arrangement typically lasts between three and five years. During this period, the company makes scheduled monthly contributions from its trading profits to an insolvency practitioner, who then distributes the funds to creditors.

Does a UK insolvency procedure affect the foreign parent company?

Generally, the parent company is protected by the corporate veil and is not liable for the UK subsidiary's debts. Exceptions apply if the parent company provided corporate guarantees to landlords or lenders, or if the directors engaged in wrongful trading.

When to Hire a UK Restructuring Lawyer

You should hire a UK restructuring lawyer the moment your subsidiary faces chronic cash flow issues, anticipates breaching financial covenants, or struggles to pay its tax obligations. Early intervention expands your strategic options and protects international directors from personal liability claims.

Complex cross-border restructurings require coordinated legal strategy between your home jurisdiction and the UK. To navigate these requirements safely, find a restructuring lawyer in the United Kingdom who specializes in cross-border insolvency and director advisory services.

Next Steps for Foreign Parent Companies

- Conduct a Solvency Review: Immediately instruct your UK financial team to produce a 13-week cash flow forecast to determine the exact date the subsidiary will run out of working capital.

- Halt Preferential Payments: Stop any non-essential transfers of cash or assets from the UK subsidiary back to the parent company to prevent future clawback actions by an administrator.

- Consult a Licensed Professional: Engage a UK insolvency practitioner and legal counsel to confidentially evaluate whether a Pre-Pack Administration or a CVA is the most viable path forward for your corporate group.