- Companies have 21 days to formally acknowledge an audit notice from the Irish Revenue Commissioners.

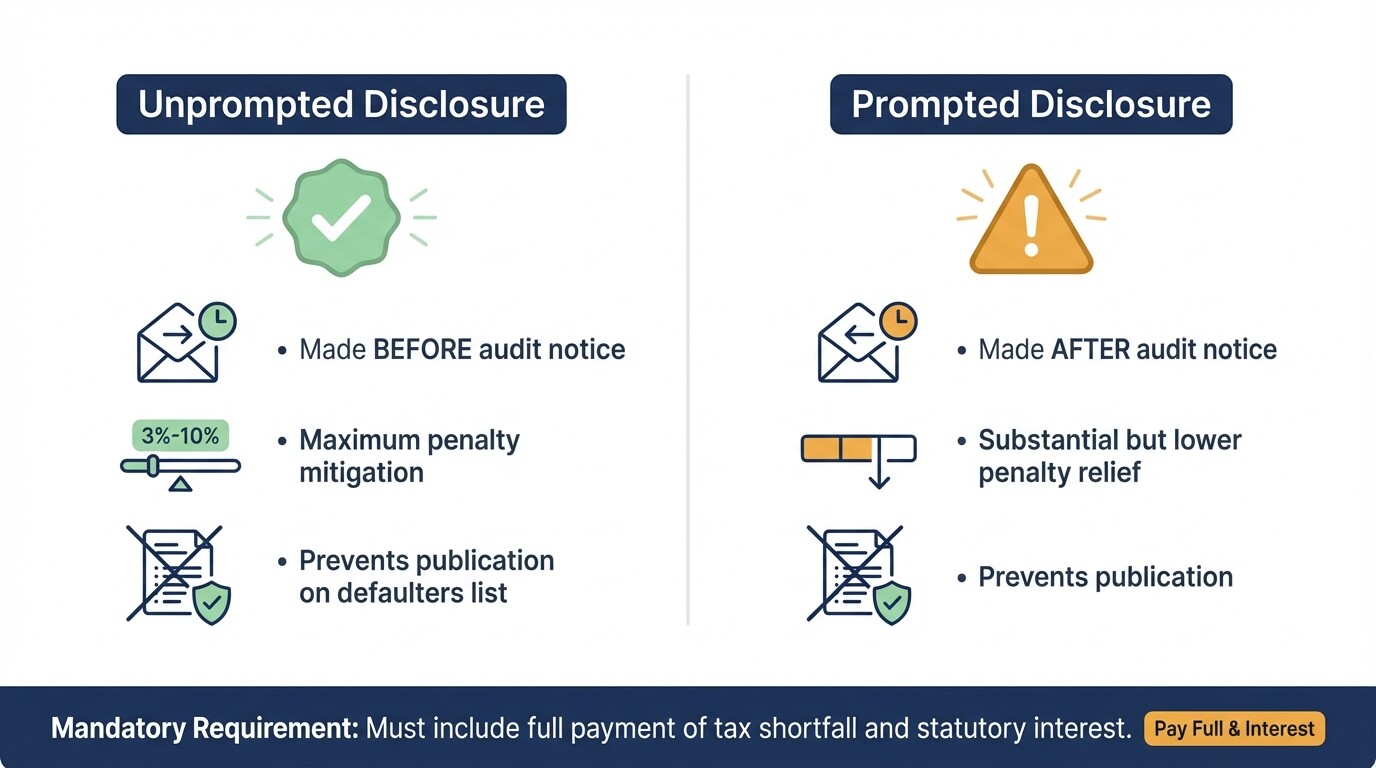

- Submitting a qualifying voluntary disclosure before an audit begins can substantially reduce penalties and prevent publication of the company's name.

- The Mutual Agreement Procedure (MAP) provides a direct, cross-border alternative to domestic tax court litigation.

- Under EU directives, MAP resolutions must be attempted within a strict two-year timeline.

- If domestic litigation is required, appeals to the Tax Appeals Commission (TAC) must be filed within 30 days of a final assessment.

Ireland Corporate Tax Residency Disputes: Pre-Litigation Checklist

When a multinational tech or pharma corporation faces a tax residency or transfer pricing inquiry in Ireland, immediate procedural compliance is vital. Use this pre-litigation checklist to structure your initial response.

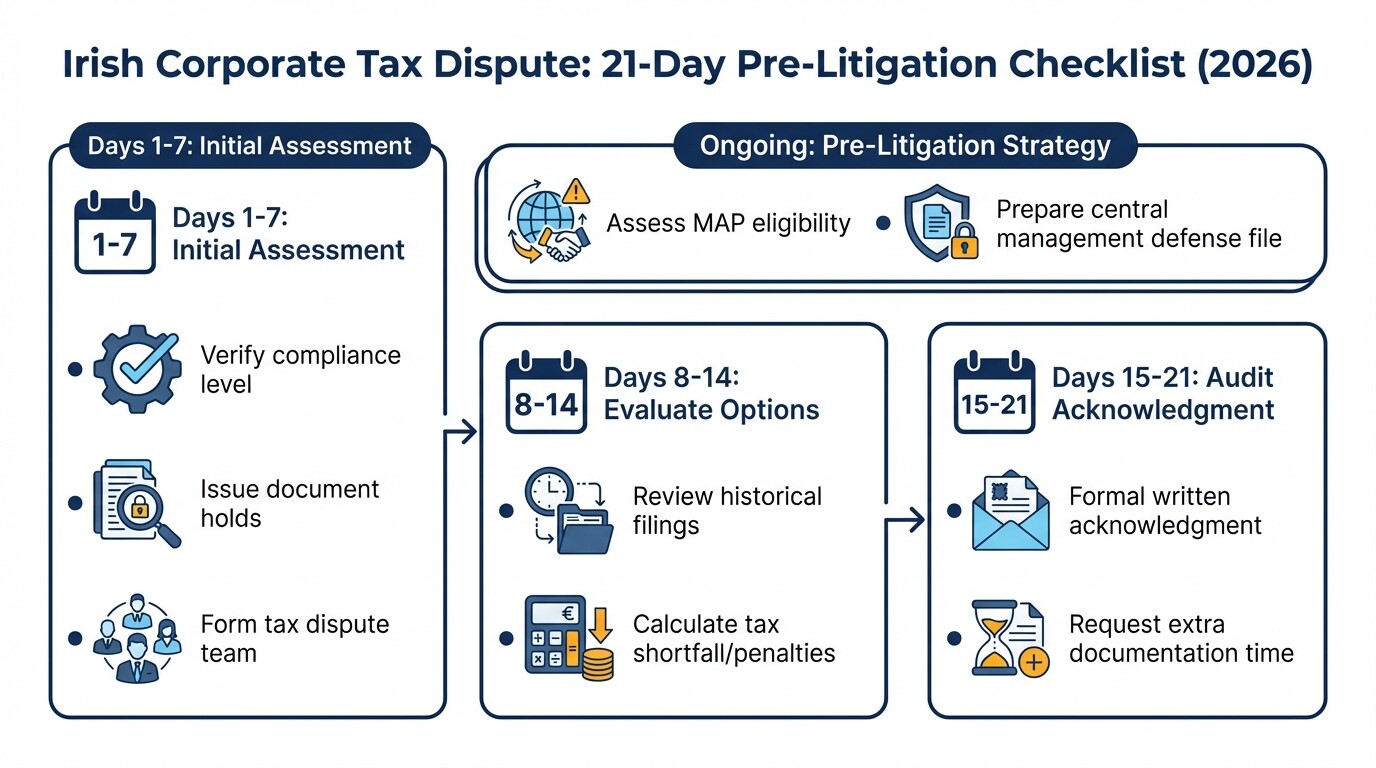

- Day 1-7: Initial Assessment

- Verify the level of compliance intervention initiated by the Revenue Commissioners (e.g., Level 1, Level 2 Audit, or Level 3 Investigation).

- Issue internal document preservation holds across all global financial and executive teams.

- Form a dedicated tax dispute team combining internal financial controllers, external tax advisors, and legal counsel.

- Day 8-14: Evaluate Disclosure Options

- Review historical filings to determine if a "qualifying disclosure" is necessary and advantageous.

- Calculate the potential tax shortfall and unprompted vs. prompted penalty rates.

- Day 15-21: Audit Acknowledgment

- Formally acknowledge the audit notice in writing to the Revenue Commissioners before the 21-day deadline.

- Request additional time to compile requested documentation if the scope is excessively broad.

- Pre-Litigation Strategy (Ongoing)

- Assess if the dispute involves double taxation, making it eligible for the Mutual Agreement Procedure (MAP).

- Prepare a defense file specifically focusing on substance, board meeting locations, and central management and control metrics.

What is the timeline for responding to a Revenue Commissioners audit notice?

Companies typically have 21 days to formally acknowledge a Revenue Commissioners audit notice and outline a response strategy. Missing this initial deadline limits your ability to shape the audit's scope and restricts future mitigation options.

Upon receiving an official notification of a Level 2 compliance intervention (an audit), the clock immediately starts. During this 21-day window, corporate taxpayers must confirm receipt of the notice, inform Revenue of their intent to prepare the requested files, and decide whether to make a prompted qualifying disclosure. Engaging proactively during this period demonstrates cooperation, which is a key metric the Revenue Commissioners use when determining final penalty categories if a tax shortfall is discovered.

Can voluntary disclosures reduce penalties as an alternative to audits?

A qualifying disclosure made before an audit starts can significantly reduce penalties and prevent the company from being published on the quarterly list of tax defaulters. This proactive mechanism is highly encouraged by Irish tax authorities as a way to correct honest errors without costly investigations.

The penalty reduction depends heavily on the timing of the disclosure. An "unprompted" qualifying disclosure-made before the company is notified of an audit-offers the highest penalty mitigation, often reducing standard penalties down to 3% to 10% depending on the category of default. A "prompted" qualifying disclosure, made after the audit notice is received but before the audit formally begins, also provides substantial relief but at less favorable rates than an unprompted submission. In both scenarios, the disclosure must be accompanied by full payment of the tax and statutory interest.

Are there alternatives to formal tax court litigation?

The Mutual Agreement Procedure (MAP) is the primary alternative to domestic tax court litigation for resolving cross-border double taxation disputes. This state-to-state negotiation mechanism bypasses the standard Irish court system to resolve treaty-based corporate tax conflicts.

For multinational corporations, tax residency disputes often trigger double taxation claims across multiple jurisdictions. Instead of fighting the assessment in an Irish court, the company can initiate a MAP request. Under this process, the "competent authority" of Ireland (the Revenue Commissioners) negotiates directly with the competent authority of the other involved state to agree on the company's tax residency or profit allocation. MAP removes the adversarial courtroom element, focusing instead on applying the relevant Double Taxation Agreement (DTA).

How long does the MAP resolution process take?

Under EU dispute resolution directives, competent authorities must attempt to reach a mutual agreement within a two-year timeline. This mandatory timeframe begins only after both relevant tax authorities have accepted the MAP request and received all necessary supporting documentation.

While the standard timeline is two years, authorities can request a one-year extension in highly complex corporate residency or transfer pricing cases. If the states fail to reach an agreement within this binding timeframe, the taxpayer can invoke mandatory binding arbitration under the EU Tax Dispute Resolution Directive. This forces the states to resolve the deadlock, guaranteeing the multinational corporation an eventual end to the double taxation uncertainty without open-ended delays.

What is the timeline to file an appeal with the Tax Appeals Commission (TAC)?

A formal Notice of Appeal must be submitted to the Tax Appeals Commission (TAC) within exactly 30 days of receiving the final assessment from the Revenue Commissioners. Failing to file within this strict 30-day window generally results in the assessment becoming final and legally payable.

The TAC is an independent statutory body that hears appeals against Revenue assessments. To initiate the appeal, the company must clearly state the grounds for the appeal and the specific points of law or fact in dispute. It is also a mandatory prerequisite that the taxpayer pays any uncontested tax liabilities before the TAC will accept the appeal. Due to the inflexible nature of the 30-day deadline, legal and financial teams must draft their appeal strategy concurrently with the closing stages of the Revenue audit.

Common Misconceptions About Irish Corporate Tax Audits

- Negotiation is informal and fluid: Many companies wrongly assume they can negotiate a financial settlement at any time during an audit. In reality, the Revenue Commissioners operate under a strict, codified penalty framework. Disclosures and settlements must follow rigid statutory procedures.

- Starting a MAP stops domestic tax collection: Initiating a MAP does not automatically suspend the requirement to pay the disputed tax in Ireland. Companies must formally request a suspension of tax collection, which Revenue may grant subject to specific conditions, or pay the tax upfront and seek a refund post-resolution.

- Board minutes guarantee tax residency: Multinational firms often believe that holding board meetings in Dublin automatically secures Irish tax residency. Revenue increasingly scrutinizes "substance over form," investigating where the actual strategic central management and control (CMC) takes place on a daily basis.

Frequently Asked Questions

Does receiving an audit notice mean the company is suspected of tax evasion?

No. While audits can be triggered by specific risk indicators, many are routine compliance interventions targeting specific industries, such as tech or pharma, or specific issues like transfer pricing and intellectual property valuations.

Can a company pursue MAP and a TAC appeal at the same time?

Yes, a company can technically file a protective appeal with the TAC while simultaneously initiating a MAP. However, the domestic TAC proceedings will typically be paused (stayed) until the MAP negotiations are concluded to avoid conflicting outcomes.

Are Tax Appeals Commission hearings public?

Most TAC hearings are held in public, but a taxpayer can formally request the hearing be held in camera (in private). The TAC will generally grant this request if public disclosure would cause serious commercial harm or reveal proprietary trade secrets.

When to Hire a Tax Dispute Lawyer

You should engage legal counsel immediately upon receiving an official notification of a Level 2 Audit or a Level 3 Investigation from the Revenue Commissioners. While your internal finance team and external accountants will handle the financial data, a lawyer specializing in tax controversy ensures your rights are protected, prevents self-incrimination, and establishes a defense strategy structured for a potential court appeal.

Firms facing complex cross-border residency challenges should secure pre-litigation lawyers in Ireland to oversee the strategic timing of voluntary disclosures, TAC appeal filings, and MAP requests.

Next Steps

- Secure the Audit Notice: Identify the specific date the Revenue Commissioners issued the notice to accurately track your 21-day response deadline.

- Implement a Document Hold: Instruct all executives and board members to retain all emails, travel records, and minutes relating to strategic decision-making and central management and control.

- Draft the Initial Response: Work with your legal and tax advisory team to draft a formal acknowledgment of the audit, establish communication channels, and outline your approach to the impending compliance intervention.