- CSRD Expansion: Starting in 2026 for the 2025 financial year, the EU Corporate Sustainability Reporting Directive (CSRD) requires large private Italian subsidiaries to publish detailed, audited ESG reports.

- Whistleblower Mandates: Italian Legislative Decree No. 24/2023 requires companies with 50 or more employees to implement secure internal reporting channels.

- Organizational Liability: Integrating ESG into your subsidiary's "Modello 231" framework shields the company from administrative liability related to environmental and corporate crimes.

- Audit Readiness: Subsidiaries must maintain standardized documentation for emissions data and supply chain human rights practices.

How the 2026 EU Corporate Sustainability Reporting Directive Impacts Italian Subsidiaries

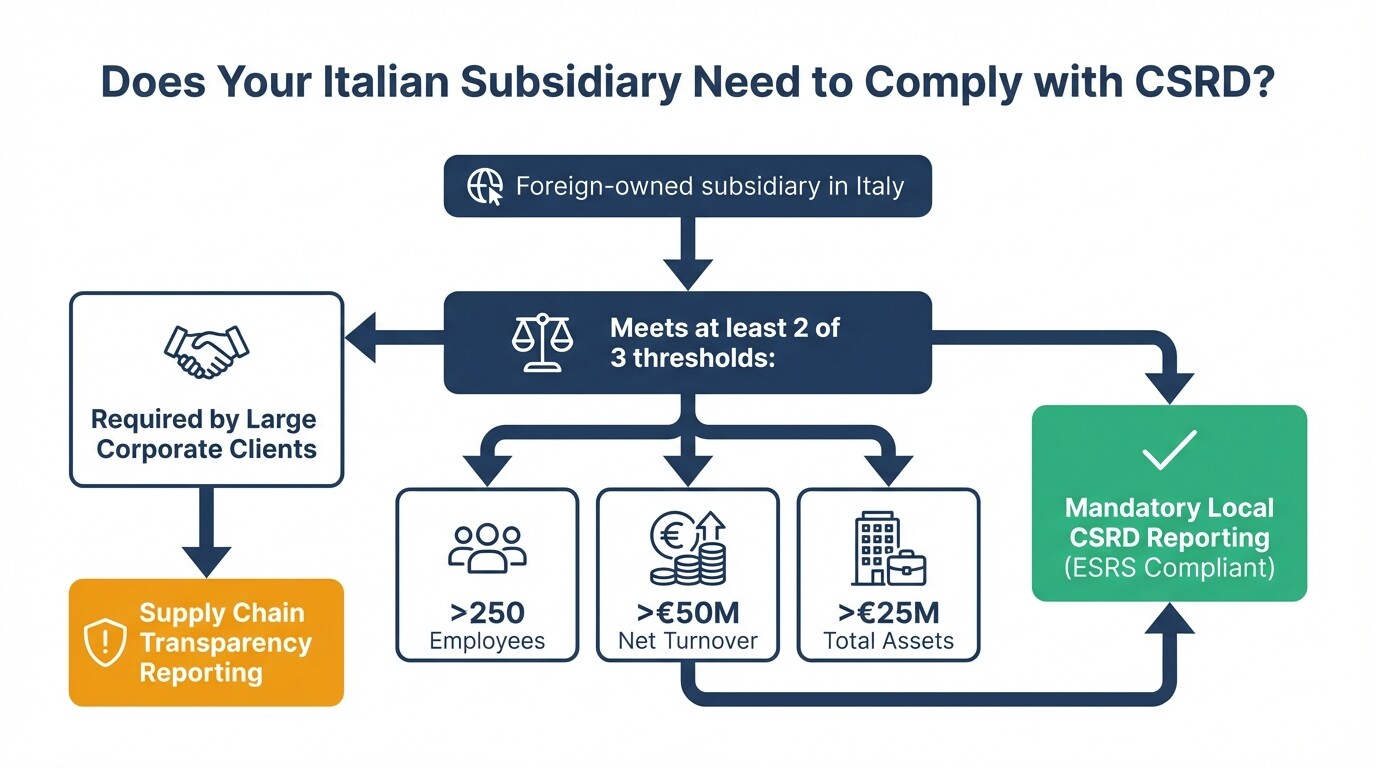

The EU Corporate Sustainability Reporting Directive (CSRD) requires Italian subsidiaries of foreign multinationals to disclose environmental, social, and governance (ESG) metrics starting in 2026. This regulation replaces the Non-Financial Reporting Directive and expands the number of companies obligated to report on their sustainability impact.

Foreign-owned subsidiaries operating in Italy must comply with local CSRD reporting if they meet two of the following thresholds: over 250 employees, a net turnover exceeding €50 million, or total assets exceeding €25 million. Unlisted small and medium-sized enterprises (SMEs) may also need to adopt ESG reporting if their larger corporate clients require supply chain transparency to meet their own CSRD obligations.

The directive mandates "double materiality" reporting. Your Italian subsidiary must disclose how environmental and social issues impact financial health, alongside how business operations impact the environment and local communities. Foreign parent companies cannot submit a generic global report if the Italian subsidiary meets the thresholds independently. The local entity must produce localized data that complies with European Sustainability Reporting Standards (ESRS).

ESG Compliance Checklist for Foreign Subsidiaries in Italy

Managing ESG compliance requires integrating European directives and Italian legislative decrees into local operations. Use this checklist to assess your subsidiary's current standing and identify regulatory gaps before reporting cycles begin.

Governance and Policy Framework

- Update the Modello 231 (Organizational, Management, and Control Model) to include protocols preventing environmental offenses and corporate fraud.

- Appoint an ESG compliance officer or committee within the subsidiary's board of directors.

- Implement an internal whistleblowing system compliant with Italian Legislative Decree 24/2023.

Environmental Documentation

- Establish automated data collection for energy consumption, water usage, waste management, and raw material sourcing at Italian facilities.

- Document Scope 1, Scope 2, and Scope 3 greenhouse gas emissions.

- Align environmental claims with the EU Taxonomy to prevent greenwashing investigations by the Italian Antitrust Authority (AGCM).

Social and Labor Compliance

- Audit the gender pay gap within the Italian workforce to comply with Italy's Equal Opportunities Code.

- Collect human rights and labor compliance certifications from primary suppliers.

- Document occupational health and safety metrics under Italian Legislative Decree 81/2008.

Mandatory Documentation for Supply Chain and Carbon Footprint Audits

Italian authorities and independent auditors require standardized data proving your subsidiary's carbon footprint and supply chain due diligence. You must gather greenhouse gas emission logs, supplier codes of conduct, and human rights impact assessments.

Auditors require primary data sources for carbon footprint verification. These include utility bills from Italian energy providers, fuel consumption logs for company fleets, and localized waste disposal manifests (Formulari di Identificazione dei Rifiuti).

Supply chain transparency requires third-party documentation. Keep signed supplier codes of conduct and records of human rights audits. Under corporate sustainability due diligence rules, your Italian entity is held responsible for violations within its supply chain. Maintain records of supplier screening processes, corrective action plans issued to non-compliant vendors, and contracts containing mandatory ESG compliance clauses.

Internal Timeline for ESG Reporting to Italian Authorities

Developing an internal reporting timeline ensures your Italian subsidiary meets mandatory filing deadlines with the Italian Companies Register (Registro delle Imprese) and regulatory bodies like CONSOB. A standard annual reporting cycle requires several months of preparation and external auditing before the final spring submission. Under Italian implementation of EU directives, statutory auditors (revisori legali) or authorized independent audit firms must provide limited assurance on sustainability reports.

| Month | Compliance Action | Key Stakeholders |

|---|---|---|

| January | Finalize data collection for the previous fiscal year's environmental and social metrics. | ESG Officer, Operations Managers |

| February | Draft the initial sustainability report in accordance with ESRS guidelines. | Sustainability Team, Legal Counsel |

| March | Conduct independent third-party assurance of the drafted ESG report. | External Auditors |

| April | Secure approval from the Board of Directors alongside annual financial statements. | Board of Directors |

| May | File the final audited sustainability report with the Registro delle Imprese. | Corporate Secretary |

Implementing Whistleblower Policies and Governance Frameworks

Italian labor law mandates specific whistleblower protections and corporate governance structures. Under Legislative Decree No. 24/2023, companies with 50 or more employees must establish secure internal reporting channels that protect informants from retaliation.

The reporting channel must use encryption to guarantee the confidentiality of the whistleblower, the person reported, and the content of the report. The policy must outline the procedure for submitting reports, allowing written, voice-recorded, or in-person disclosures. It must also specify that an impartial internal committee or external legal consultant will manage investigations.

ESG governance in Italy involves Legislative Decree 231/2001 (Modello 231). Adopting a Modello 231 framework is practically mandatory for large subsidiaries. It creates an organizational model that shields the company from direct liability if an employee commits an environmental crime, bribes an official, or violates labor rights, provided the company actively enforced compliance protocols.

Preparing for ESG Regulatory Inspections

Passing an ESG inspection by Italian authorities requires maintaining an organized repository of environmental and social impact records. Inspectors look for discrepancies between public sustainability claims and internal operational data to uncover greenwashing or regulatory negligence.

Failing to file mandatory sustainability reports or publishing fraudulent ESG data can result in administrative fines ranging from tens of thousands to millions of euros. Directors may face personal liability, and greenwashing can trigger separate antitrust fines of up to €5 million from the AGCM.

When the Italian Antitrust Authority (AGCM) or environmental protection agencies (such as ISPRA or ARPA) conduct inspections, they expect immediate access to raw data. Every sustainability claim in marketing materials or annual reports must map directly to an underlying audit trail. If the subsidiary claims to be "carbon neutral" or "zero waste," localized, third-party verified certificates must be available in the compliance data room. Train local site managers to respond to unannounced environmental audits and establish a clear protocol for legal escalation.

Common Misconceptions About ESG Compliance in Italy

Foreign parent companies often assume global parent-level compliance satisfies Italian regulations. This leads to local administrative penalties, reputational damage, and operational delays.

- Global ESG reports cover Italian subsidiaries. While consolidated reporting is sometimes permitted, an Italian subsidiary meeting the CSRD thresholds independently must prepare its own localized data. Even if exempted from a separate report, the Italian entity must supply ESRS-compliant data to the parent company.

- Modello 231 is entirely separate from ESG. Corporate leadership often treats Modello 231 as an outdated anti-bribery tool. Italian courts increasingly view a robust Modello 231 as the foundational governance structure required for the "G" in ESG. It protects the company from liability for environmental disasters or labor exploitation.

- Greenwashing is only a marketing issue. Foreign companies sometimes view exaggerated sustainability claims as a low-risk marketing tactic. In Italy, the AGCM aggressively prosecutes greenwashing as an unfair commercial practice, resulting in heavy fines and mandatory public retractions.

When to Hire a Corporate Governance Lawyer

Engaging local legal counsel is necessary when structuring your subsidiary's governance framework or approaching the financial and employee thresholds that trigger mandatory ESG reporting. A local lawyer ensures internal policies align with EU directives and Italian legislative decrees.

Partnering with corporate governance lawyers in Italy is useful when drafting or updating your Modello 231 to include environmental and labor safeguards. Legal experts can set up compliant whistleblower channels, review supplier contracts for mandatory ESG clauses, and represent the subsidiary during regulatory inspections or audits by Italian authorities.

Next Steps

Map your current data collection capabilities against local requirements to understand your exposure before new reporting cycles begin.

- Conduct a gap analysis: Compare the subsidiary's current environmental and social data tracking against the European Sustainability Reporting Standards (ESRS).

- Update governance policies: Draft an internal whistleblowing policy compliant with Italian Decree 24/2023 and revise your Modello 231.

- Appoint local leadership: Designate an internal ESG officer within the Italian subsidiary to manage the transition and serve as the point of contact for external auditors and legal counsel.