Key Takeaways

Corporate restructuring for foreign entities in Malaysia requires following local statutes, particularly the Companies Act 2016. Early intervention and understanding the regulatory framework help preserve asset value and maintain business operations.

- Executing a scheme of arrangement typically takes six to nine months, depending on court dockets and creditor consensus.

- Judicial Management and Corporate Voluntary Arrangement are statutory alternatives to liquidation that offer protective moratoriums.

- Transferring assets between foreign subsidiaries requires multi-agency clearance, including approvals from Bank Negara Malaysia and the Inland Revenue Board.

- Intellectual property must be ring-fenced early in the distress cycle to prevent involuntary sale during insolvency proceedings.

- Foreign creditors hold the same statutory rights as domestic creditors in Malaysian insolvency proceedings.

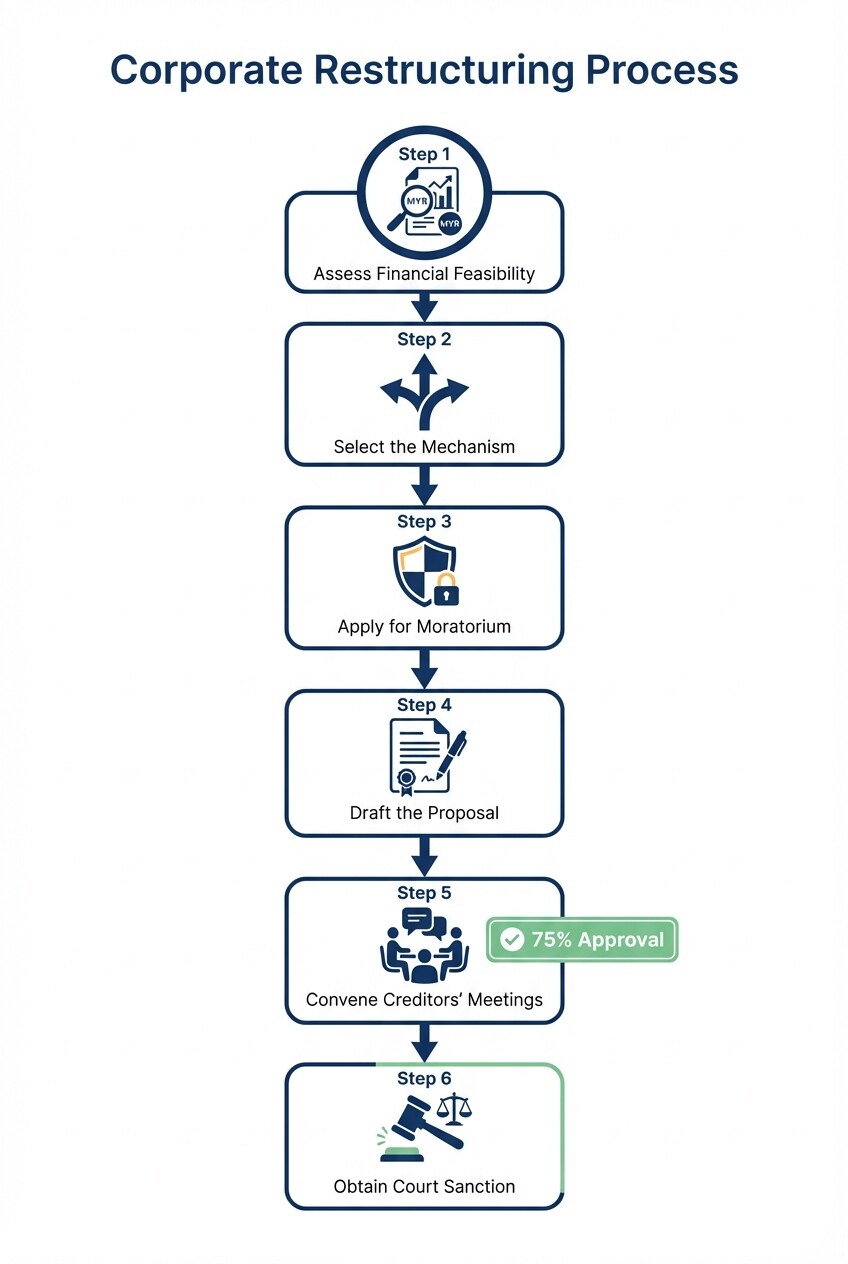

Step-by-Step Guide to Corporate Restructuring

Restructuring a foreign-owned entity in Malaysia follows procedures governed by the Companies Act 2016. The process demands accurate financial assessment and strict court compliance.

- Assess financial feasibility: Conduct an independent business review to determine if the Malaysian subsidiary is viable. Establish whether the entity faces temporary cash flow issues or structural insolvency.

- Select the mechanism: Choose a statutory tool based on creditor dynamics. Options include a Scheme of Arrangement, Judicial Management, or a Corporate Voluntary Arrangement (CVA).

- Apply for moratorium: File an application with the High Court of Malaya to secure a restraining order. This statutory moratorium prevents creditors from initiating legal proceedings, winding-up petitions, or asset seizures while you formulate the restructuring plan.

- Draft the proposal: Prepare an explanatory statement detailing the compromise offered to creditors. This document must categorize creditors into classes (e.g., secured, unsecured) and offer a higher return than liquidation.

- Convene creditors' meetings: Hold court-convened meetings for each creditor class to vote on the proposal. A successful vote requires approval from a majority in number representing 75% of the total value of the creditors present and voting.

- Obtain court sanction: Return to the High Court to have the approved scheme sanctioned. Once sanctioned by the court and lodged with the Companies Commission of Malaysia (SSM), the plan legally binds all creditors, including those who voted against it.

Timeline for a Scheme of Arrangement

A scheme of arrangement generally takes six to nine months to execute, depending on corporate complexity and creditor resistance. Mandatory court procedures and statutory notice periods under the Companies Act 2016 dictate this timeline.

- Months 1-2 (Preparation): The company drafts the proposed scheme and applies to the High Court to convene creditors' meetings. Concurrently, the company applies for a restraining order (moratorium) to freeze creditor actions, initially granted for up to three months.

- Months 3-5 (Voting): The company distributes court-approved explanatory statements to creditors, providing at least 14 days statutory notice before meetings. Creditors convene, debate the terms, and vote on the plan.

- Months 6-9 (Sanction): If the 75% value threshold is met across all classes, the company applies for the final court sanction. The scheme takes effect on the date the court order is lodged with the Companies Commission of Malaysia.

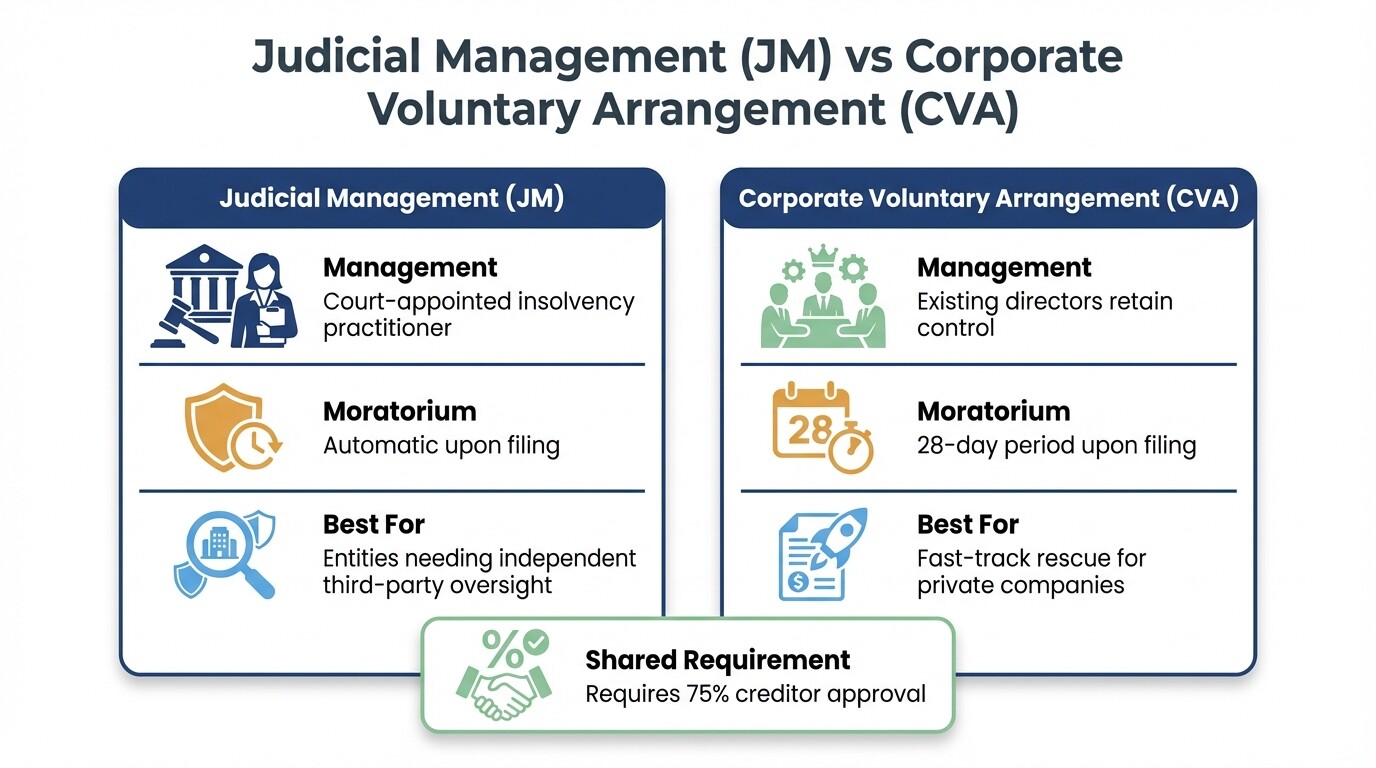

Alternatives to Liquidation: Judicial Management and Corporate Rescue

Judicial Management and Corporate Voluntary Arrangement (CVA) are statutory alternatives to liquidation in Malaysia. These mechanisms give distressed companies time to rehabilitate operations under professional supervision.

Judicial Management (JM)

Judicial Management places the distressed company under an independent, court-appointed insolvency practitioner. Filing a JM application automatically triggers a moratorium that stops legal proceedings and winding-up actions. The judicial manager has 60 days to present a restructuring proposal to creditors, requiring a 75% majority vote by value to pass. This tool is effective for foreign subsidiaries that need an independent third party to restore creditor confidence.

Corporate Voluntary Arrangement (CVA)

A CVA is a fast-track rescue mechanism suited for private companies without extensive secured debt. The company's directors draft a debt restructuring proposal with an insolvency practitioner acting as a nominee. Once filed with the court, a 28-day moratorium automatically begins. The proposal requires a 75% approval vote from unsecured creditors. Unlike JM, the existing directors retain control of the company throughout the process.

Regulatory Approvals for Asset Transfers

Transferring assets between foreign subsidiaries during restructuring requires clearance from specific Malaysian regulatory bodies. Multinational entities must plan these transfers carefully to avoid triggering tax liabilities or regulatory breaches.

- Bank Negara Malaysia: Any cross-border transfer of funds, assumption of foreign debt, or repatriation of liquidation proceeds must comply with BNM's Foreign Exchange Policy. Restructuring intra-group loans often requires notification or approval from the central bank.

- Inland Revenue Board: Asset transfers trigger stamp duty and Real Property Gains Tax (RPGT) for real estate. While intra-group transfer reliefs exist under Section 15A of the Stamp Act 1949, applying for these exemptions requires demonstrating the companies share at least 90% common ownership.

- Sector-Specific Regulators: If the subsidiary holds operating licenses (such as manufacturing licenses from the Ministry of International Trade and Industry), transferring the operational assets may require prior regulatory consent to keep the licenses valid.

Protecting Intellectual Property During Distress

Protecting intellectual property (IP) requires isolating these assets from insolvency proceedings to prevent their involuntary sale by liquidators. Foreign entities must audit their IP portfolios and structure assets to survive local subsidiary distress.

Hold critical IP in a stable offshore parent or a dedicated holding company, rather than within the operating Malaysian subsidiary. The Malaysian entity should use the IP through licensing agreements. Review these licensing agreements for ipso facto clauses, which are provisions that terminate the license upon the licensee's insolvency. Any prior transfers of IP out of the Malaysian subsidiary must be completed for fair market value before insolvency occurs. This prevents courts from clawing back the assets as undervalued transactions or fraudulent preferences.

Common Misconceptions About Malaysian Restructuring

Multinational directors often misunderstand how Malaysian insolvency frameworks govern foreign-owned subsidiaries. Relying on these assumptions leads to delayed interventions and personal liability.

Parent company liability: Malaysian courts uphold the principle of separate legal personality. Unless the parent company provides explicit corporate guarantees for the subsidiary's loans, or there is evidence of fraud justifying a pierced corporate veil, the parent company's assets remain protected from the subsidiary's creditors.

Schemes of arrangement: Schemes under Section 366 of the Companies Act 2016 are frequently used by solvent companies for internal group reorganizations, mergers, and debt refinancing. They are flexible corporate tools, not strictly insolvency mechanisms.

Key Operational Rules for Foreign Entities

Rights of Foreign Creditors

Foreign creditors possess the same statutory rights to prove debts and vote in creditors' meetings as domestic Malaysian creditors. There is no legal discrimination based on nationality under Malaysian insolvency frameworks. However, repatriating recovered funds to a foreign jurisdiction remains subject to local foreign exchange administration rules.

Foreign Entities as Judicial Managers

A judicial manager in Malaysia must be a qualified and locally approved insolvency practitioner. While a foreign parent company can initiate the judicial management application for its local subsidiary, the court only appoints an individual holding a valid liquidator license granted by the Malaysian Ministry of Finance.

Freezing Creditor Actions

Filing for a scheme of arrangement does not automatically freeze creditor actions. To stop creditors from suing or winding up the company, the entity must separately apply to the High Court for a restraining order under Section 368 of the Companies Act, which is subject to specific qualifying criteria.

When to Hire a Restructuring Lawyer

Engaging legal counsel is necessary the moment a foreign entity anticipates insolvency, breaches a financial covenant, or plans to reorganize its Malaysian footprint. Early intervention by restructuring and insolvency lawyers in Malaysia improves the chances of securing court-ordered moratoriums and negotiating terms with institutional creditors before winding-up petitions are filed. Directors should secure legal advice if cash flow projections indicate an inability to pay debts within the next six months. Continuing to trade while insolvent triggers personal liability under Malaysian law.

Next Steps for Foreign Entities

Proper preparation protects the parent company's global assets and aligns local operations with strategic goals.

- Audit intra-group guarantees and intercompany loans to identify exact exposure levels.

- Assemble a localized team of legal counsel, financial advisors, and tax consultants to draft a restructuring proposal.

- Initiate informal, without-prejudice discussions with key secured creditors to gauge their interest in a rescue plan before filing formal court applications.