Malaysia Foreign Manufacturing: Principal Hub vs Standard Subsidiary

- Standard manufacturing subsidiaries are ideal for straightforward localized production, while Principal Hubs suit multinationals managing regional operations and supply chains.

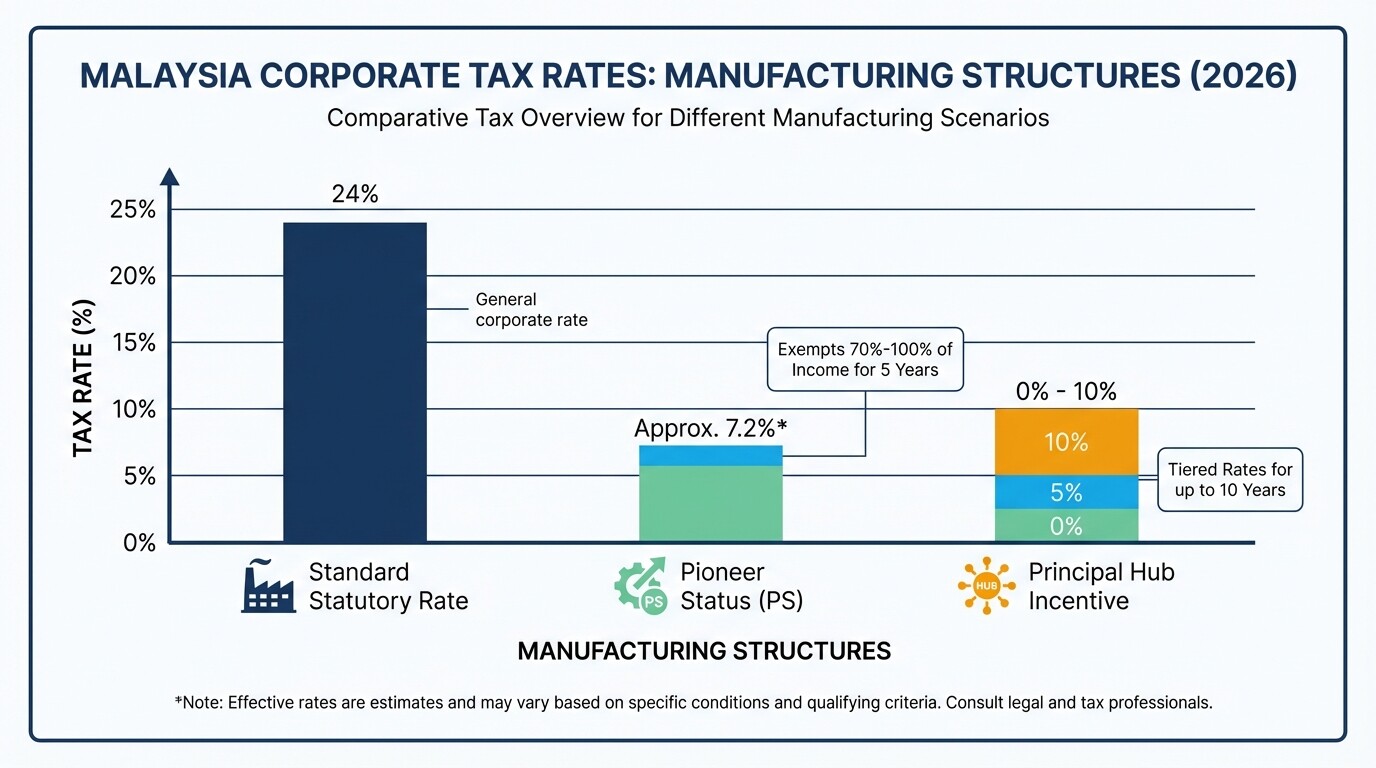

- A Principal Hub can qualify for concessionary corporate tax rates between 0% and 10% under MIDA incentives, compared to the standard 24% rate.

- Foreign investors must meet strict paid-up capital requirements, generally ranging from RM 500,000 for standard setups to RM 2.5 million or more for specialized licenses.

- Establishing a compliant structure requires a minimum of one local resident director and strict adherence to Malaysia's Companies Act 2016.

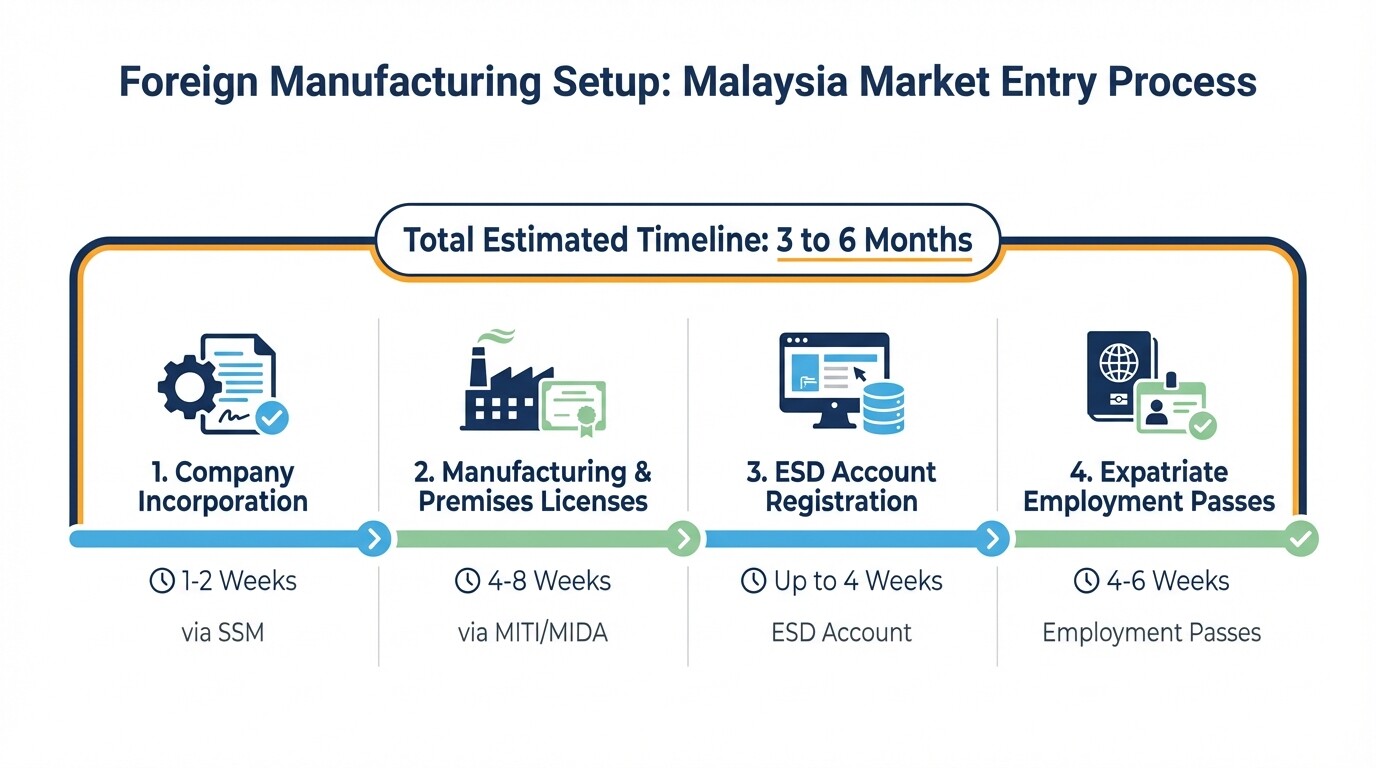

- Timelines for securing necessary manufacturing licenses and expatriate employment passes typically range from three to six months.

Principal Hub vs Standard Subsidiary Comparison

Choosing between a Principal Hub and a standard manufacturing subsidiary depends heavily on your company's regional footprint and tax strategy. A standard subsidiary handles localized manufacturing, while a Principal Hub manages regional network operations, supply chains, and strategic services.

| Feature | Standard Manufacturing Subsidiary | Principal Hub (PH) |

|---|---|---|

| Primary Function | Direct manufacturing and local production. | Regional management, strategic services, and supply chain control. |

| Corporate Tax Rate | 24% statutory rate. | 0% to 10% concessionary rate (tiered). |

| MIDA Tax Incentives | Pioneer Status (PS) or Investment Tax Allowance (ITA). | Principal Hub Incentive for 5 to 10 years. |

| Paid-Up Capital | RM 500,000 (minimum for foreign ownership); RM 2.5M for Manufacturing License. | RM 2.5 million minimum. |

| Substance Requirements | Basic employment and local operational footprint. | High local employment, high annual operational expenditure (OPEX). |

| Target Audience | Single-market focused manufacturers. | Multinationals with extensive Asia-Pacific operations. |

Evaluating MIDA Tax Incentives and Corporate Tax Rates

The Malaysian Investment Development Authority (MIDA) offers distinct tax incentives that heavily favor regional scaling. While standard manufacturing companies pay the statutory corporate tax rate of 24%, Principal Hubs can secure tiered concessionary rates based on their investment and employment commitments.

For a standard manufacturing setup, foreign investors typically apply for Pioneer Status (PS), which provides a tax exemption on 70% to 100% of statutory income for five years. Alternatively, the Investment Tax Allowance (ITA) grants an allowance of 60% to 100% on qualifying capital expenditure incurred within five years.

To attract high-value regional operations, MIDA's official Principal Hub incentive offers much deeper tax relief. Depending on the tier, a Principal Hub can achieve a corporate tax rate of 0%, 5%, or 10% for up to 10 years. Qualifying for these tiers requires strict commitments, including serving at least three network companies outside Malaysia, generating minimum annual sales, and incurring significant annual operating expenditure (OPEX) within Malaysia.

Administrative Costs and Minimum Paid-Up Capital Requirements

Foreign investors must meet specific minimum paid-up capital thresholds to legally operate and hire expatriates in Malaysia. Standard 100% foreign-owned subsidiaries typically require at least RM 500,000, while operations requiring specialized licenses face much higher capital commitments.

Setting up a standard foreign-owned Sendirian Berhad (Sdn Bhd) carries an initial baseline requirement of RM 500,000 in paid-up capital. However, under the Industrial Co-ordination Act 1975, any manufacturing company with shareholders' funds of RM 2.5 million or more, or engaging 75 or more full-time employees, must apply for a formal Manufacturing License. Consequently, most foreign manufacturers budget for a minimum RM 2.5 million injection to operate smoothly.

Administrative costs also include registration fees payable to the Companies Commission of Malaysia (SSM), which scale up to RM 1,000 depending on the authorized capital. Annual recurring administrative costs-such as company secretarial fees, statutory audits, and tax agent retainers-average between RM 15,000 and RM 30,000 annually, depending on transaction volume. Principal Hubs face higher indirect costs to maintain compliance with their MIDA OPEX commitments, which often mandate spending upwards of RM 3 million annually in local operations.

Timelines for Manufacturing Licenses and Expatriate Passes

Foreign corporations should anticipate a three to six-month timeline to become fully operational in Malaysia. This timeline accounts for company incorporation, securing manufacturing licenses from regulatory bodies, and processing Expatriate Employment Passes (EP).

The initial company incorporation via SSM takes approximately one to two weeks, assuming all director KYC (Know Your Customer) documents are prepared. Once incorporated, companies must apply for a Manufacturing License from MIDA or the Ministry of Investment, Trade and Industry (MITI), a process that generally takes four to eight weeks for approval. Standardizing factory premises and obtaining local council operating licenses run concurrently with this step.

Expatriate Employment Passes are processed through the Expatriate Services Division (ESD). A company must first register its corporate account with ESD, taking up to four weeks. Once the ESD account and the Manufacturing License are approved, individual EP applications take an additional four to six weeks. Foreign companies cannot successfully secure EPs until the minimum paid-up capital is fully injected and the relevant industry licenses are secured.

Corporate Governance: Board Composition and Resident Directors

All private limited companies in Malaysia require at least one director who ordinarily resides in the country. Strict corporate governance rules dictate board composition, fiduciary duties, and equity conditions regardless of whether you choose a Principal Hub or a standard subsidiary.

Under the Companies Act 2016, a resident director can be a Malaysian citizen, a Permanent Resident, or an expatriate holding a valid residence or employment pass. Because the resident director holds full fiduciary duties and legal liabilities, multinationals often deploy a senior executive on an Employment Pass to fulfill this role, or they engage a professional nominee director temporarily during the setup phase.

Corporate governance compliance is rigorously enforced. Directors are responsible for ensuring accurate financial reporting, timely tax submissions, and adherence to ESG (Environmental, Social, and Governance) standards increasingly mandated by MITI. Establishing these protocols early is essential, which is why multinationals frequently consult corporate governance lawyers in Malaysia to draft robust board charters and internal governance frameworks prior to incorporation.

Transfer Pricing and Intercompany Documentation

Multinationals operating a Principal Hub or manufacturing subsidiary must comply strictly with Malaysia's cross-border transfer pricing regulations. The Inland Revenue Board of Malaysia (LHDN) requires robust intercompany documentation to ensure transactions between related parties occur at arm's length.

Because Principal Hubs inherently manage regional network operations-often involving the cross-border transfer of services, IP, and raw materials-they are prime targets for transfer pricing audits. The LHDN transfer pricing framework mandates that companies maintain contemporaneous documentation, including both a Master File and a Local File.

Failure to provide proper transfer pricing documentation upon request can result in severe penalties, including surcharges of up to 5% on transfer pricing adjustments, regardless of whether the adjustment results in additional tax payable. For multinationals, ensuring that service fees, management fees, and goods transfers between the Malaysian entity and its foreign affiliates are benchmarked properly is critical to avoiding prolonged disputes with tax authorities.

Common Misconceptions About Malaysian Manufacturing Setups

Foreign investors frequently underestimate local compliance requirements and operational timelines when planning their market entry into Malaysia. Clearing up these misconceptions prevents costly delays and regulatory penalties.

- "A Principal Hub is just a tax status." Many investors assume a Principal Hub is merely a paper entity for tax optimization. In reality, MIDA requires significant economic substance, including high-level local employment (such as C-suite executives based in Malaysia) and substantial local operational spending.

- "Using a nominee director eliminates liability." Multinationals often use local nominee directors to expedite incorporation. However, under Malaysian law, a nominee director carries the exact same legal and fiduciary liabilities as an active director, and local banks increasingly scrutinize accounts opened by nominee-heavy boards.

- "100% foreign ownership guarantees total control." While Malaysia generally allows 100% foreign equity in the manufacturing sector, specific strategic industries or applications for certain local grants may trigger Bumiputera (indigenous) equity requirements or local talent hiring quotas.

Frequently Asked Questions

What is the primary role of a Principal Hub in Malaysia?

A Principal Hub functions as a centralized control tower for a multinational's regional operations. It manages strategic services, supply chain operations, and risk management for network companies across the Asia-Pacific region, rather than engaging directly in heavy localized manufacturing.

Can a standard manufacturing subsidiary upgrade to a Principal Hub later?

Yes, an existing manufacturing subsidiary can apply to MIDA to establish a Principal Hub. However, the operations must be clearly segregated, and the company must prove that the Principal Hub creates new, high-value regional jobs and investments rather than just reclassifying existing local roles.

Do I need a physical office before applying for an expatriate pass?

Yes, the Expatriate Services Division (ESD) requires proof of physical business premises. You must provide a tenancy agreement and local authority licenses (such as a signboard license) to register the company with ESD before individual pass applications can begin.

Are there restrictions on repatriating profits from Malaysia?

Malaysia maintains a liberal foreign exchange administration policy. Foreign companies are generally free to repatriate capital, profits, dividends, and royalties to their home countries, provided they have settled all local tax obligations and filed the necessary withholding tax documentation.

When to Hire a Corporate Governance Lawyer

Navigating Malaysia's foreign direct investment framework requires specialized legal counsel early in the planning phase. Engaging a corporate governance lawyer ensures your chosen entity structure aligns with MIDA's strict tax incentive requirements and the Companies Act 2016.

Retain legal counsel before executing your incorporation or signing commercial leases. A lawyer will help draft your Constitution, establish legally sound intercompany agreements for transfer pricing, and structure your board to meet resident director mandates safely. You can connect with highly qualified lawyers in Malaysia to ensure your market entry is fully compliant from day one.

Next Steps for Market Entry

Executing a successful manufacturing setup in Malaysia requires a strategic, phased approach. Begin by finalizing your operational goals to determine the correct entity type before committing capital.

First, define whether your Malaysian entity will serve purely local production (Standard Subsidiary) or manage regional supply chains (Principal Hub). Next, engage a local company secretary and legal counsel to incorporate the Sendirian Berhad and inject the required paid-up capital. Once incorporated, apply simultaneously for your premises licenses and your Manufacturing License from MITI/MIDA, which will subsequently unlock your ability to secure Expatriate Employment Passes for your foreign management team.