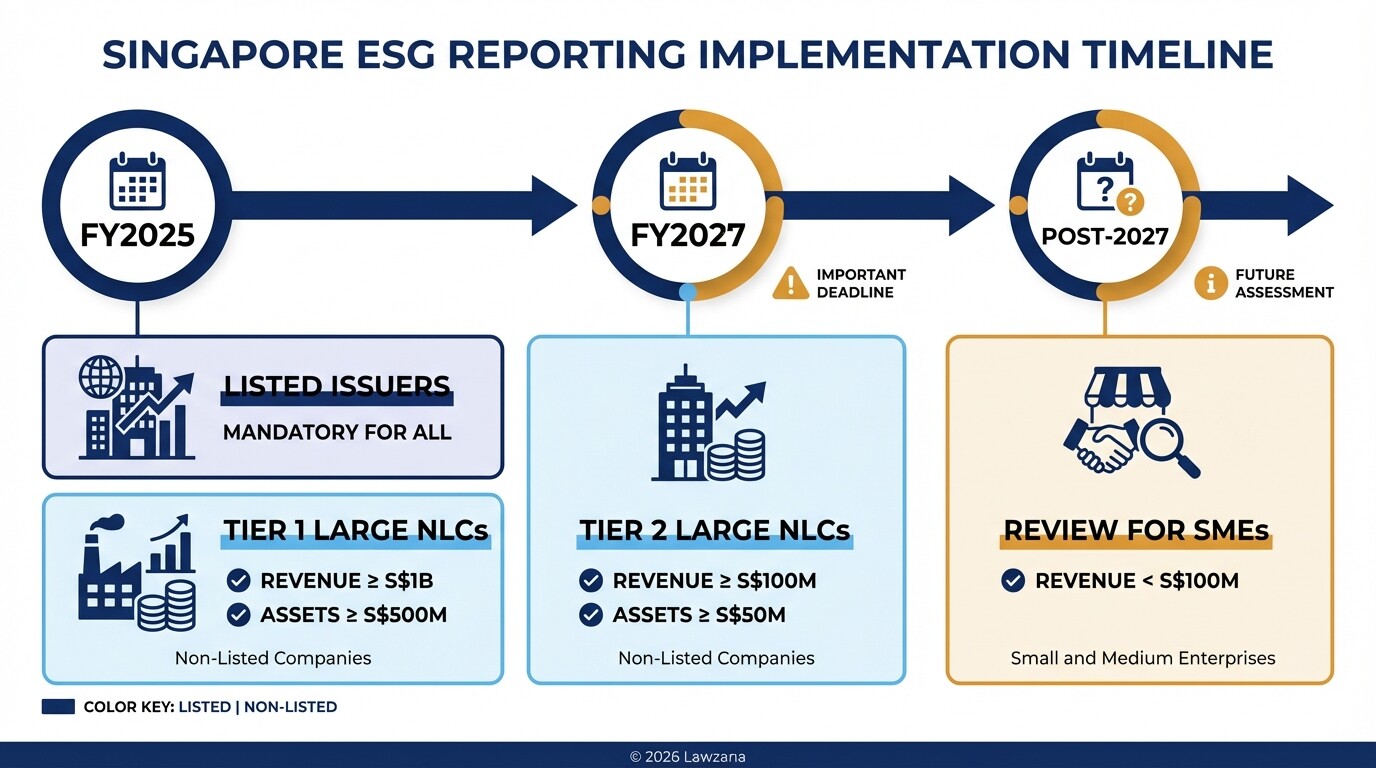

- Starting in FY2027, large non-listed companies in Singapore with annual revenue of at least S$100 million and total assets of S$50 million must file mandatory climate-related disclosures.

- All mandatory reporting must align with the International Sustainability Standards Board (ISSB) framework to ensure global comparability.

- Failure to provide accurate ESG data can lead to legal action under the Misrepresentation Act and regulatory penalties from the Accounting and Corporate Regulatory Authority (ACRA).

- Small and Medium Enterprises (SMEs) that proactively adopt ESG reporting gain preferential access to government grants and sustainable financing options.

- Integrating environmental "conditions precedent" in commercial contracts is now a critical risk management strategy for Singaporean directors.

Understanding the New ESG Reporting Thresholds for Singapore Companies

Singapore is implementing a phased approach to mandatory climate reporting, overseen by the Accounting and Corporate Regulatory Authority (ACRA) and the Singapore Exchange (SGX). While listed companies face earlier deadlines, the new "Large Non-Listed Company" (LNLC) category brings significant compliance obligations to the private sector starting from financial years commencing in 2025 and 2027.

The mandatory disclosure requirements are determined by the following financial thresholds:

| Company Type | Revenue Threshold | Asset Threshold | Implementation Year |

|---|---|---|---|

| Listed Issuers | Any | Any | FY2025 |

| Large Non-Listed (Tier 1) | ≥ S$1 billion | ≥ S$500 million | FY2025 |

| Large Non-Listed (Tier 2) | ≥ S$100 million | ≥ S$50 million | FY2027 |

| Exempt SMEs | < S$100 million | < S$50 million | Voluntary (Review in 2027) |

If your company meets these thresholds for two consecutive financial years, you are legally required to produce a climate reporting disclosure. This report must be filed alongside your annual financial statements via the ACRA portal.

ESG Compliance Checklist for Singapore SMEs

To prepare for mandatory reporting or to satisfy the requirements of larger supply chain partners, Singaporean SMEs should follow this technical roadmap. This checklist ensures your internal systems can capture the data required by the IFRS Sustainability Disclosure Standards.

- Establish Board Oversight: Formalize a board-level committee responsible for sustainability risks and opportunities.

- Identify Climate Risks: Conduct a "Physical Risk" assessment (e.g., impact of floods on warehouses) and "Transition Risk" assessment (e.g., impact of carbon taxes).

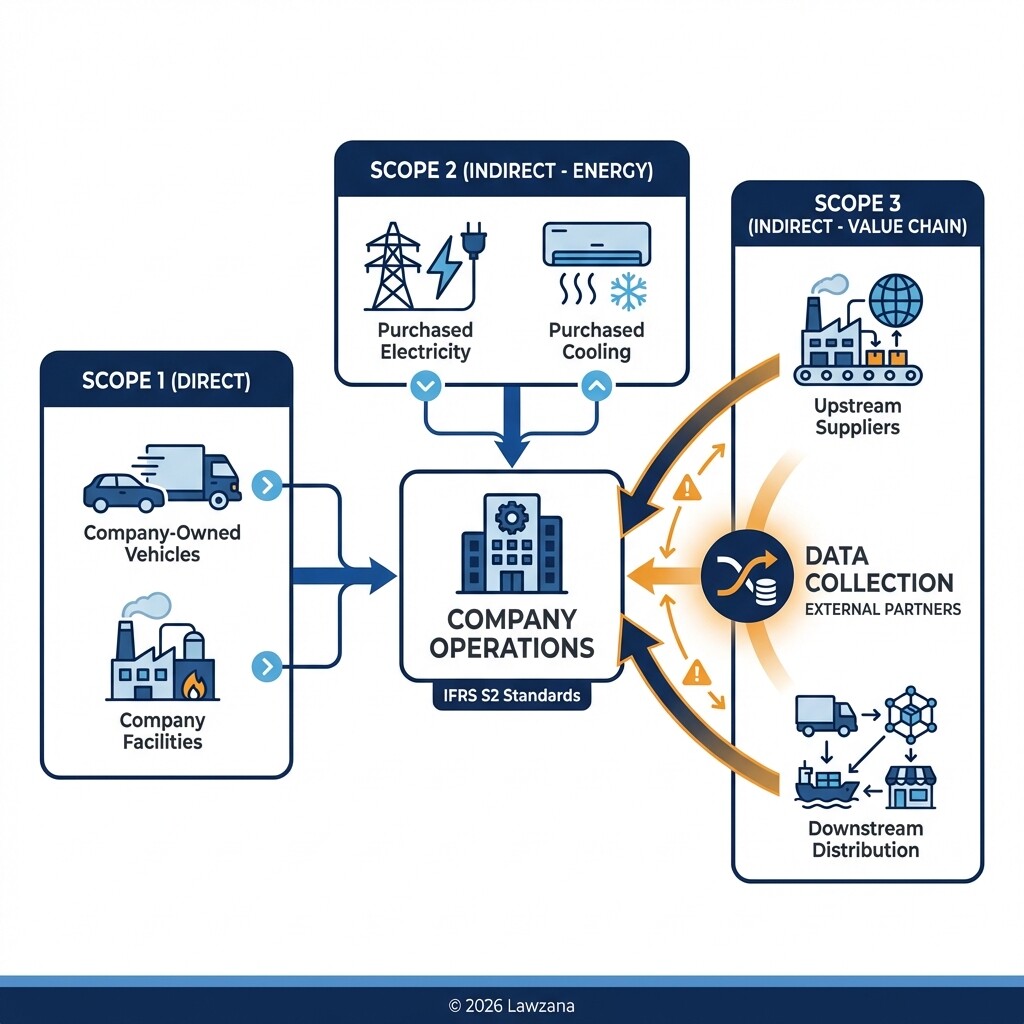

- Set Greenhouse Gas (GHG) Baselines: Measure Scope 1 (direct emissions) and Scope 2 (purchased electricity) emissions according to the GHG Protocol.

- Review Scope 3 Data: Begin dialogues with vendors to collect indirect emission data from your supply chain, as this is often the most complex reporting requirement.

- Gap Analysis: Compare current internal data against the IFRS S1 (General Requirements) and IFRS S2 (Climate-related Disclosures) standards.

- Internal Controls: Implement audit-ready data collection processes to ensure "reasonable assurance" for future third-party verification.

- Reporting Timeline: Map out your first reporting cycle to align with your annual financial audit to ensure consistency.

Legal Liability for Greenwashing in Corporate Reporting

Greenwashing in Singapore refers to the practice of making misleading or unsubstantiated claims about the environmental benefits of a product, service, or corporate policy. As reporting becomes mandatory, these claims transition from marketing fluff to legal representations that can trigger significant liability.

The legal risks for inaccurate ESG reporting primarily stem from three areas:

- ACRA Regulatory Action: Providing false or misleading information in statutory filings is an offense under the Companies Act. Directors can face fines up to S$50,000 or imprisonment if they are found to have intentionally misrepresented sustainability data.

- Misrepresentation Act: If a company secures a commercial contract or investment based on false ESG claims, the counterparty may sue for damages or rescind the contract under the Misrepresentation Act.

- Consumer Protection (Fair Trading) Act (CPFTA): For B2C companies, the Competition and Consumer Commission of Singapore (CCCS) can take enforcement action against "unfair practices," which includes misleading environmental labels.

To mitigate this risk, every ESG claim must be backed by "verifiable data." Avoid vague terms like "eco-friendly" or "carbon neutral" without providing the specific methodology and third-party certifications used to reach those conclusions.

A Step-by-Step Guide to Aligning with ISSB Standards

The International Sustainability Standards Board (ISSB) framework, specifically IFRS S1 and S2, is the legal benchmark for Singapore's new reporting regime. Alignment requires moving beyond qualitative descriptions to quantitative, data-driven disclosures.

Step 1: Governance Disclosures

Detail the processes, controls, and procedures the company uses to monitor sustainability risks. You must identify which individuals or board committees are responsible for ESG and how those responsibilities are reflected in the company's terms of reference.

Step 2: Strategy and Risk Management

Disclose the specific climate-related risks that could reasonably be expected to affect the company's cash flows, access to finance, or cost of capital over the short, medium, or long term. This includes describing how the company identifies, assesses, and prioritizes these risks.

Step 3: Metrics and Targets

Companies must disclose their absolute gross greenhouse gas emissions (Scopes 1, 2, and eventually 3). You must also report on the targets you have set to reach net-zero goals and the specific metrics used to measure progress, such as carbon intensity per dollar of revenue.

How ESG Compliance Affects Government Grants

In Singapore, ESG compliance is no longer just a regulatory burden; it is a gateway to capital. Enterprise Singapore and other statutory boards have integrated sustainability requirements into their evaluation criteria for major funding programs.

The Enterprise Sustainability Programme (ESP) provides targeted support for SMEs to build internal capabilities. Companies that demonstrate a clear ESG reporting roadmap are prioritized for:

- Sustainability Reporting Grants: Direct subsidies to cover the costs of engaging consultants and adopting reporting software.

- Energy Efficiency Grants (EEG): Up to 70% funding for SMEs in manufacturing, food services, and retail to adopt energy-efficient equipment.

- Enterprise Financing Scheme (EFS): Better interest rates for "Green Loans" where the borrower meets specific ESG Key Performance Indicators (KPIs).

Failure to maintain ESG standards can result in the clawback of grant funds if the sustainability milestones promised in the application are not met.

Integrating Environmental Clauses into Commercial Contracts

To manage Scope 3 emissions and protect against supply chain liability, Singapore companies are increasingly using "Green Clauses" in their standard B2B agreements. These clauses ensure that vendors and partners adhere to the same ESG standards as the reporting company.

Sample ESG Termination Clause

"The Service Provider warrants that it shall maintain compliance with all applicable Singapore environmental laws and regulations. If the Service Provider fails to provide annual verified Scope 1 and 2 emission data within thirty (30) days of the Company's request, or if the Service Provider is found liable for a significant environmental breach by a regulatory authority, the Company reserves the right to terminate this Agreement immediately without penalty."

Sample Data Cooperation Provision

"The Seller agrees to provide the Buyer with all necessary sustainability data, including but not limited to carbon footprint metrics and waste management logs, in a format compatible with IFRS S2 standards. This data shall be provided quarterly to facilitate the Buyer's mandatory climate reporting obligations under ACRA regulations."

Common Misconceptions About ESG in Singapore

Misconception 1: "My SME is too small to worry about ESG laws." While you may not be required to file with ACRA yet, your larger clients (who are required to report) will likely demand your ESG data to satisfy their own Scope 3 reporting requirements. If you cannot provide this data, you risk being dropped from their supplier list.

Misconception 2: "ESG is just about the environment." In the Singapore context, "Governance" is equally critical. ACRA focuses heavily on board diversity, executive compensation transparency, and anti-corruption measures. A company with low carbon emissions but poor governance will still fail an ESG audit.

FAQ

Is climate reporting mandatory for all companies in Singapore?

No, it is currently mandatory for listed companies. It becomes mandatory for non-listed companies with at least S$100 million in revenue and S$50 million in assets starting in FY2027.

What are Scope 1, 2, and 3 emissions?

Scope 1 are direct emissions from sources you own (e.g., company vehicles). Scope 2 are indirect emissions from purchased electricity. Scope 3 are all other indirect emissions in your value chain (e.g., your suppliers' footprints).

Can a company be sued for not reaching its "Net Zero" target?

A company is generally not sued for failing a goal, but it can be sued for "misleading and deceptive conduct" if it sets a target with no reasonable basis or plan to achieve it, thereby inducing investors or customers.

When to Hire a Lawyer

You should consult a legal professional if your company meets the LNLC thresholds and needs to restructure its board governance to comply with ACRA requirements. Legal counsel is also essential if you are drafting high-value commercial contracts that require specific ESG indemnity clauses or if you are facing an investigation by the CCCS regarding "green" marketing claims. A lawyer can help perform a "legal audit" of your sustainability report before it is published to ensure it does not create unintended civil liabilities.

Next Steps

- Assess Your Thresholds: Review your last two years of financial statements to see if you meet the S$100 million revenue/S$50 million asset criteria.

- Appoint an ESG Lead: Designate a senior officer to oversee the transition to ISSB-aligned reporting.

- Apply for Funding: Visit the Enterprise Singapore website to check your eligibility for the Sustainability Reporting Grant.

- Update Contract Templates: Work with legal counsel to insert data-sharing and environmental compliance clauses into your standard vendor agreements.