- The 30% ruling allows eligible expats in the Netherlands to receive up to 30% of their gross salary tax-free for a maximum of five years.

- Standard Dutch employment contracts subject all income to normal tax rates and require full taxation on worldwide wealth.

- Securing the 30% tax facility requires specific contract addendums signed before your first day of work.

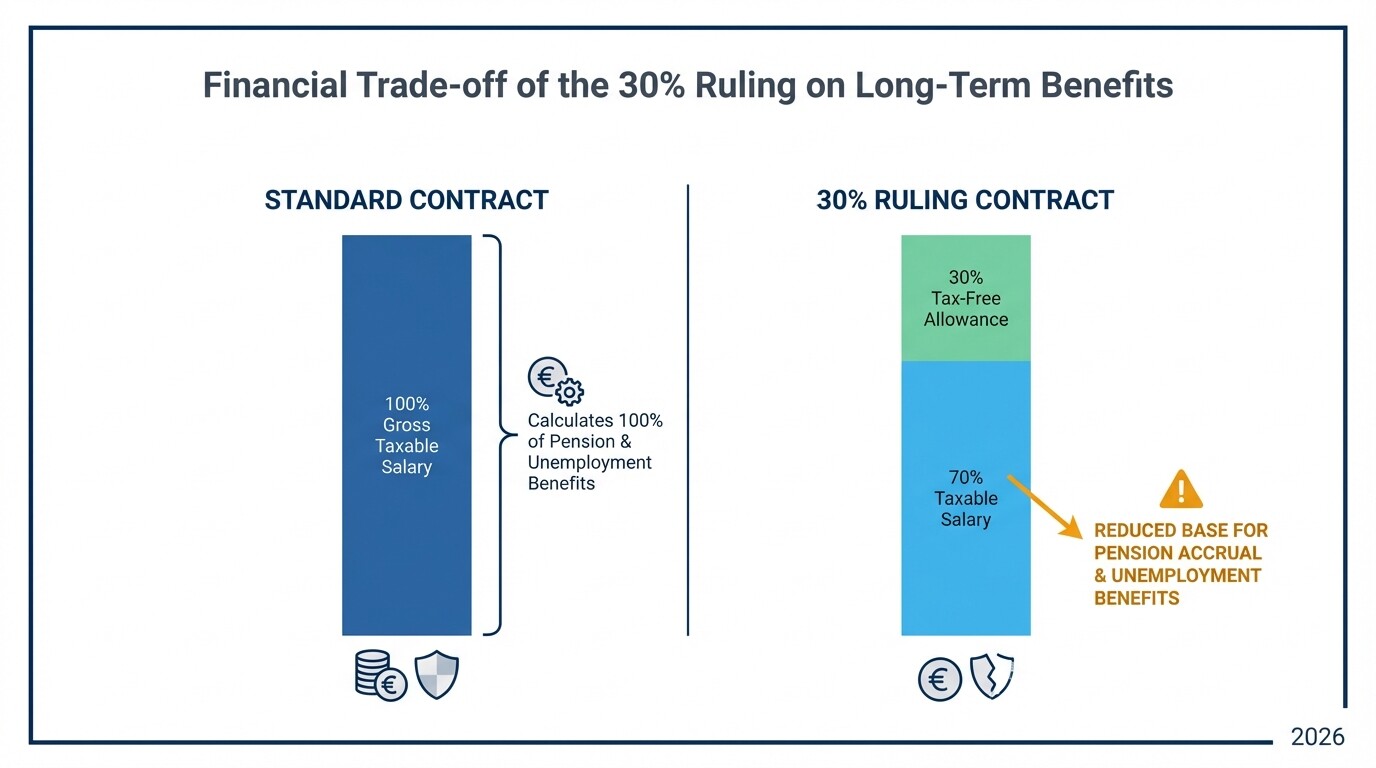

- Relying on the 30% ruling reduces your taxable gross income, which directly lowers the base used to calculate your pension accrual and unemployment benefits.

- If your tax ruling application is denied, you should negotiate backup relocation allowances directly into your employment agreement.

Comparative Checklist: 30% Tax Facility vs Standard Employment Terms

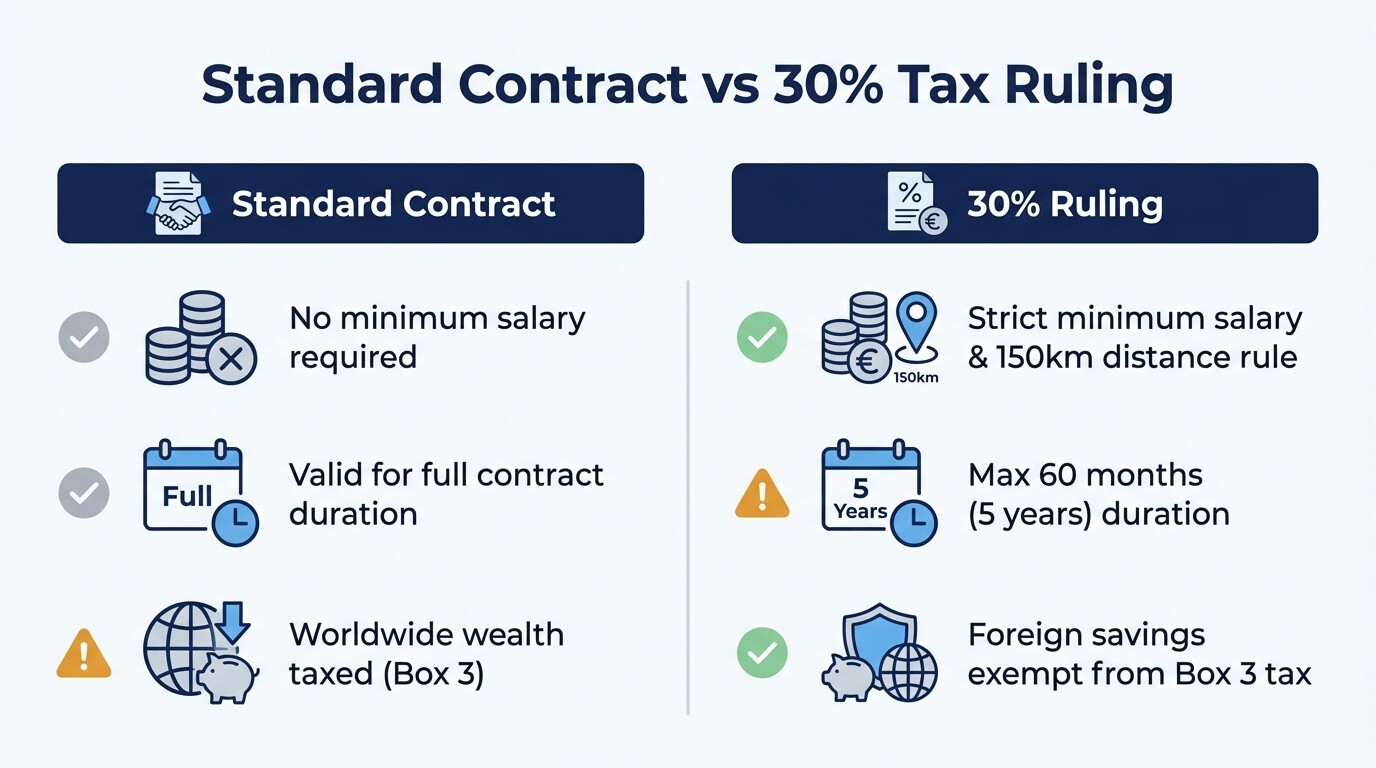

The primary difference between a standard Dutch employment contract and one leveraging the 30% ruling lies in taxation, eligibility criteria, and duration limits. A standard contract subjects all income to standard Dutch tax rates, while the 30% ruling allows up to 30% of your gross salary to be paid as a tax-free allowance to cover extraterritorial costs.

Use this checklist to compare the requirements and limitations of both contract structures:

Eligibility Criteria

- Standard Contract: Open to anyone with the legal right to work in the Netherlands. No minimum salary requirements beyond the statutory minimum wage.

- 30% Ruling: You must be recruited from outside the Netherlands (living more than 150 kilometers from the Dutch border for at least 16 of the previous 24 months).

- 30% Ruling: You must meet a strict minimum taxable salary threshold, which is updated annually (approximately €46,107 in 2024, or €35,048 if you are under 30 with a qualifying master's degree).

Duration Limits

- Standard Contract: Valid for the duration of your temporary or permanent employment agreement.

- 30% Ruling: Granted for a maximum of 60 months (five years). The tax-free percentage is currently subject to a phase-down policy over this five-year period.

Taxable Base and Wealth Tax

- Standard Contract: You are taxed on your worldwide income and assets (Box 3 wealth tax applies).

- 30% Ruling: You can opt for partial non-resident status, exempting your foreign savings and investments from Dutch Box 3 wealth tax.

Cost Estimates and Pension Impacts

Utilizing the 30% ruling impacts upfront legal costs and alters long-term financial benefits like pension accrual. Because the tax-free allowance reduces your taxable gross salary, it also lowers the base amount used to calculate your pension contributions and statutory social security benefits.

Understanding the financial impact helps you negotiate a better total compensation package:

- Legal Contract Review: Hiring an employment lawyer to review your expat contract and ensure the 30% ruling addendum is correctly drafted typically costs between €300 and €800.

- Application Assistance Fees: If your employer hires a tax advisor to process the joint application with the Dutch Tax and Customs Administration (Belastingdienst), expect fees ranging from €500 to €1,500. Employers usually cover this cost, but you should confirm this in writing.

- Pension Accrual Impact: Pension contributions in the Netherlands are calculated based on your gross taxable salary. With 30% of your salary paid tax-free, your pensionable base is reduced to 70%, resulting in lower retirement savings unless your employer agrees to base pension contributions on 100% of your pre-ruling salary.

- Unemployment Benefits (WW-uitkering): Similar to pensions, Dutch unemployment benefits are calculated on your taxable salary. Utilizing the ruling means your potential unemployment benefits will be lower.

Alternative Negotiation Clauses for Relocation

If you do not qualify for the 30% ruling, you should negotiate specific relocation allowances and benefits directly into your employment contract. Employers can legally reimburse certain extraterritorial costs tax-free under standard Dutch tax laws even without the ruling.

You should ask for these specific allowances during contract negotiations:

- Reimbursement for moving household goods and international flights.

- Coverage for temporary housing costs for the first two months.

- Allowances for international school fees for your children.

- Assistance with tax preparation for your first year in the Netherlands.

Sample Backup Relocation Clause: "In the event the Employee's joint application for the 30% ruling is formally denied by the Belastingdienst, the Employer agrees to provide a one-time, tax-free relocation allowance of €5,000. Furthermore, the Employer shall reimburse up to two months of temporary housing costs in the Netherlands, up to a maximum of €2,000 per month, subject to the submission of valid receipts."

Contract Validity Checklist: Choice of Law and Non-Compete Clauses

A valid Dutch employment contract must explicitly state the governing law and meet strict legal requirements for restrictive covenants. Non-compete clauses are generally only enforceable in permanent contracts and require a written justification of substantial business interests if included in a temporary contract.

Ensure your contract includes these critical legal components:

- Choice of Law: The contract must explicitly state that Dutch employment law governs the agreement. Even if the contract is written in English, Dutch mandatory labor laws apply.

- Language Clarification: Include a clause stating which language version prevails if the contract is translated (typically the Dutch version holds legal authority in court).

- Non-Compete Geography: The clause must define a reasonable geographic scope. A worldwide non-compete is rarely enforceable under Dutch law.

- Non-Compete Duration: The restriction should not exceed 12 months after the termination of employment.

- Temporary Contract Justification: If you are signing a fixed-term contract (e.g., one year), any non-compete clause must include a detailed written motivation explaining why the restriction is necessary to protect specific business interests. Without this motivation, the clause is void.

Severance and Transition Payments: Standard vs Highly Skilled Migrant

Severance calculations in the Netherlands depend on your years of service and salary, which differs if your taxable base is altered by the 30% ruling. Highly skilled migrants face additional residency pressures if terminated, though the statutory transition payment formula remains the same for all employees.

| Feature | Standard Employment Contract | Highly Skilled Migrant (with 30% Ruling) |

|---|---|---|

| Transition Payment Formula | 1/3 of a monthly gross salary per year of service. | 1/3 of a monthly gross salary per year of service. |

| Severance Calculation Base | Calculated on 100% of your gross monthly salary. | Calculated on your gross taxable salary (which may exclude the 30% tax-free portion depending on contract phrasing). |

| Residency Grace Period | Unaffected (assuming EU citizenship or permanent residency). | You have a maximum of 3 months to find a new recognized sponsor before your visa is revoked. |

| Garden Leave | Standard salary continues during notice period. | Standard salary continues, but the 30% ruling stops applying immediately upon active termination of duties. |

Common Misconceptions About Dutch Expat Contracts

Many international workers misunderstand how the 30% ruling applies and the level of protection Dutch employment law provides. Clarifying these myths prevents costly tax mistakes and contract disputes.

- The 30% ruling is guaranteed for all expats. The ruling is not automatic. You must meet strict salary thresholds and distance requirements. Citizens of neighboring countries living close to the border often fail the 150-kilometer distance test.

- You can apply for the 30% ruling after signing your contract. The intention to apply for the ruling must be agreed upon in writing before your first day of work. If you agree to it after starting, you will lose months of tax benefits.

- Employers can fire you without cause during probation. While probation periods offer flexibility, they are strictly capped under Dutch law. A probation period cannot exceed one month for temporary contracts under two years, and two months for permanent contracts.

Frequently Asked Questions

Who applies for the 30% tax ruling?

The employer and the employee must submit a joint application to the Belastingdienst. You cannot apply for the ruling on your own as an individual employee.

Does the 30% ruling transfer if I change employers?

The ruling can transfer to a new employer provided you still meet the minimum salary requirements and the gap between your previous employment and your new job does not exceed three months.

Can my employer keep the financial benefit of the 30% ruling?

Yes, depending on how your contract is structured. If your contract states a net salary agreement, the employer may absorb the tax benefit. You should always negotiate a gross salary agreement to ensure the tax advantage goes to you.

When to Hire a Contract Lawyer

Engaging a contract lawyer is essential when navigating complex compensation packages, facing a restrictive non-compete clause, or handling a contract termination. An employment lawyer ensures your agreement complies with Dutch labor laws and protects your international tax status before you relocate. Finding experienced contract lawyers in the Netherlands helps you secure fair terms and clarifies the long-term impact on your pension and residency.

Next Steps for Expats

Securing a fair employment contract requires early preparation and clear communication with your future employer. Follow these steps to finalize your agreement confidently.

- Request a draft of your employment contract well before your start date to allow time for a professional legal review.

- Confirm that an addendum for the 30% ruling is included in writing before you accept the job offer.

- Gather proof of your foreign residence for the 24 months prior to your hiring to ensure a smooth application process with the Dutch tax authorities.

- Clarify in writing whether your pension contributions will be based on your full gross salary or your reduced taxable salary under the ruling.