- Dutch holding companies must prove genuine local economic activity to keep tax treaty benefits under 2026 EU regulations.

- Foreign investors need exclusive local office space. Shared corporate service addresses trigger "shell company" classification and tax penalties.

- At least half of the statutory board must reside in the Netherlands.

- Annual compliance, auditing, and maintenance for a Dutch holding company cost between €7,500 and €14,000.

- You must pass specific substance and transparency tests to qualify for the 2026 dividend withholding tax exemption.

2026 Netherlands Holding Company Compliance Checklist

You must verify that your entity meets local Dutch standards and the EU Unshell Directive (ATAD 3) to maintain tax benefits. Failing these tests strips your company of withholding tax exemptions and triggers cross-border audits. Use this checklist to audit your structure before the 2026 enforcement period.

Corporate Governance and Management

- Appoint Dutch residents to at least 50% of statutory director positions.

- Verify that local directors have the professional qualifications to manage the holding company's assets.

- Hold physical board meetings in the Netherlands and document them with local minutes.

- Give local directors independent authority to execute transactions and manage daily operations.

Physical and Operational Substance

- Lease or buy dedicated office space in the Netherlands.

- Avoid shared PO boxes or standard trust office addresses.

- Open and use a bank account with an EU-licensed bank.

- Store all primary company records, ledgers, and legal documents at the Dutch office.

Financial and Tax Transparency

- Document passive income (dividends, royalties, interest) to meet minimum threshold requirements.

- Prepare evidence for the ATAD 3 "Gateway Test" to prove the entity is not a shell company.

- Budget €7,500 to €14,000 for 2026 annual compliance, director, and audit fees.

Mandatory 2026 Substance Requirements

The Netherlands requires holding companies to maintain a physical and operational presence to qualify for corporate tax exemptions. The burden of proof falls on the foreign investor. Your Dutch BV (Besloten Vennootschap) or NV (Naamloze Vennootschap) must demonstrate genuine economic presence to pass the substance test.

The Dutch tax authorities evaluate substance based on these criteria:

- Resident board members: At least half of the decision-making board members must reside in the Netherlands.

- Exclusive office space: The company needs its own premises. Shared desks at corporate service providers do not satisfy this requirement.

- Local decision making: Management must negotiate, draft, and sign key decisions in the Netherlands.

- Sufficient equity and risk: The holding company requires adequate equity to bear the financial risks of its transactions.

- Local bank account: The entity must pay its local operational expenses from a local or EU-based bank account.

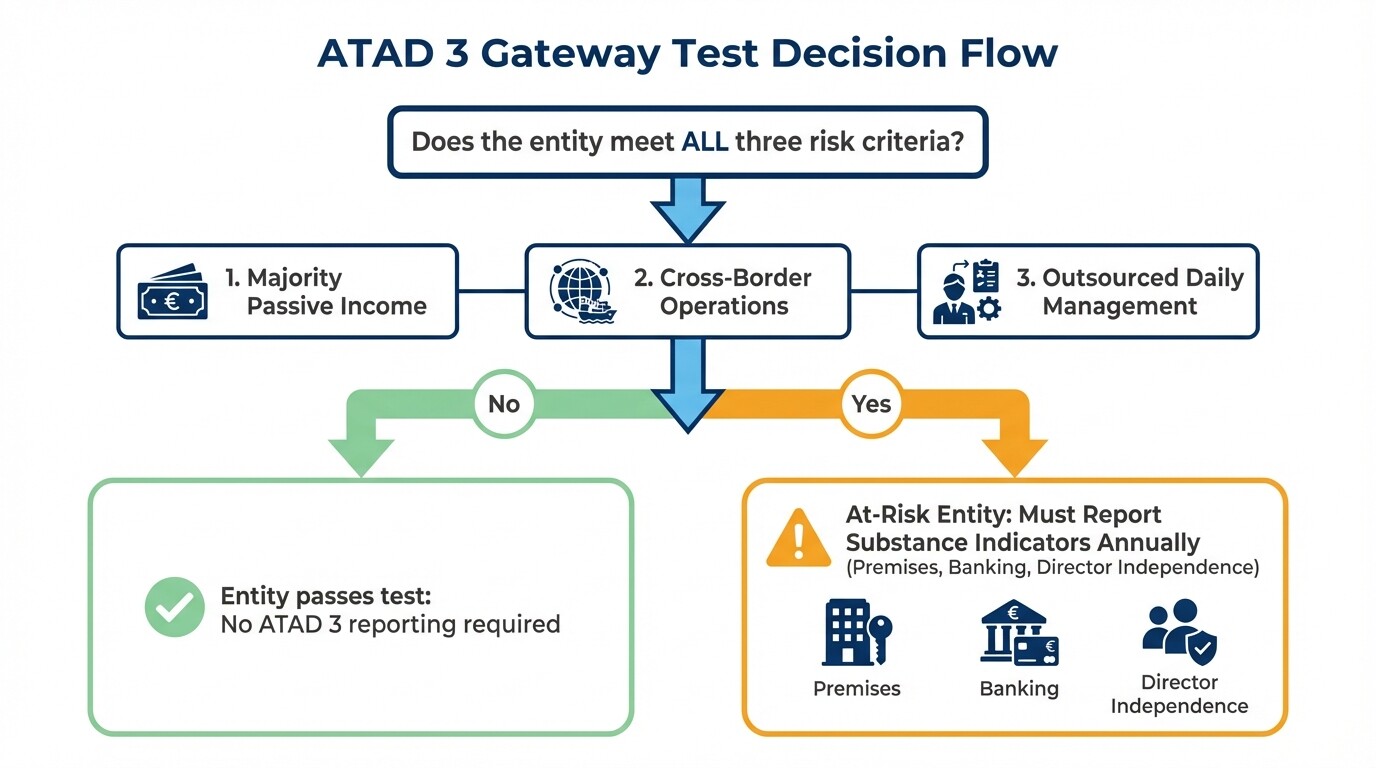

EU Unshell Directive (ATAD 3) Reporting

The EU Unshell Directive (ATAD 3) introduces reporting requirements for European holding companies to prevent the misuse of shell entities. Entities that fail to report or fail the directive's tests lose access to tax residency certificates and face increased withholding taxes.

ATAD 3 uses a "Gateway Test" to identify at-risk entities. You must submit detailed evidence to the Dutch Tax and Customs Administration if your company has majority passive income, cross-border operations, and outsourced daily management. If your company meets these three conditions, you must report specific substance indicators annually:

- Premises ownership: You must provide proof of owned or exclusively rented premises in the Netherlands.

- Active banking: You must show an active EU bank account receiving the entity's income.

- Director independence: You must prove that local directors are independent. They cannot be employed by affiliated companies or act as directors for numerous unrelated enterprises.

Avoiding the Shell Company Trap

Foreign investors often establish a holding company with insufficient local economic activity. This results in a "shell company" classification. Tax authorities examine the practical reality of how the business operates rather than just the legal formation.

Investors historically relied on corporate service providers for a registered address and a nominal local director. Under the 2026 rules, this arrangement triggers penalties. The Dutch entity must add economic value to avoid the shell company trap. The company must incur its own operational expenses and hire independent local professionals. Local directors must actively negotiate contracts instead of approving decisions made by a foreign parent company.

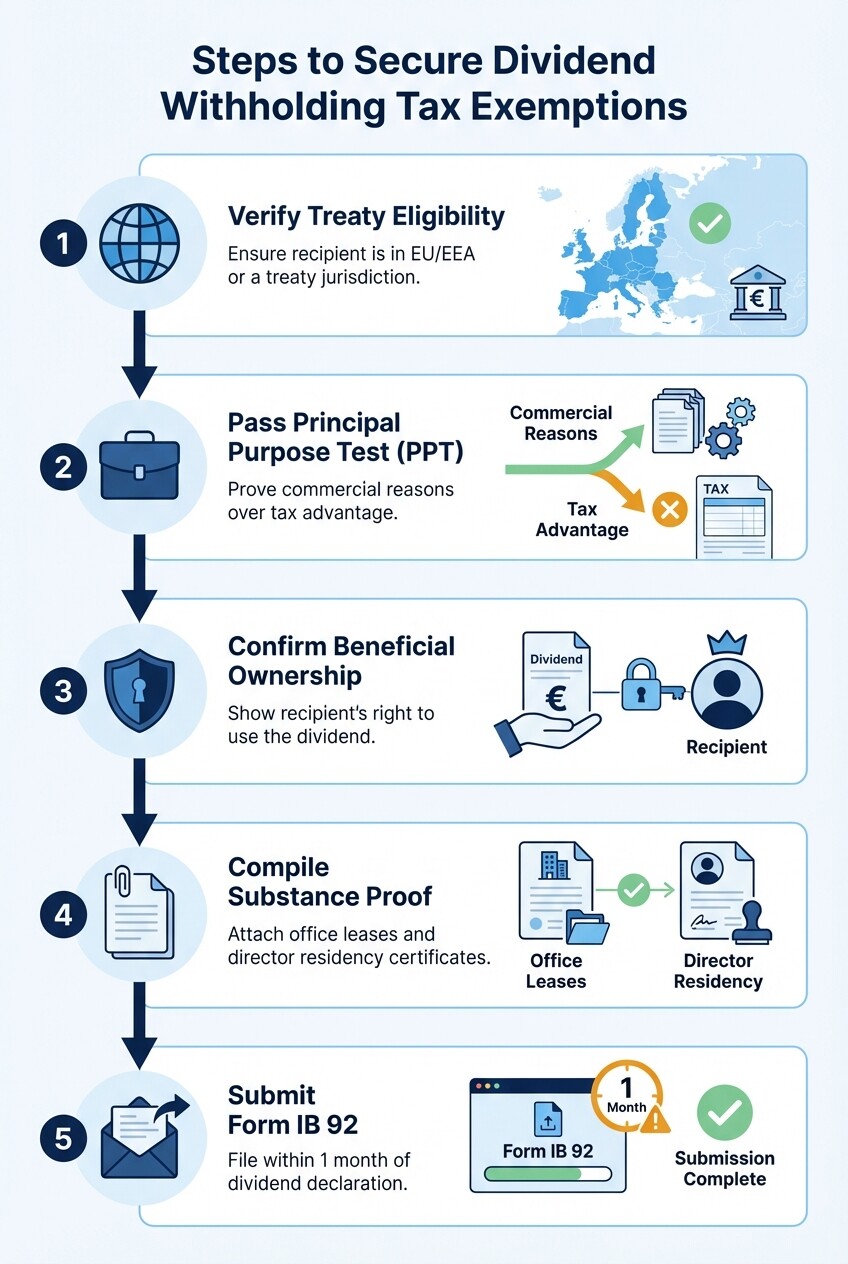

Dividend Withholding Tax Filings

You need documentation to prove non-resident shareholders qualify for dividend withholding tax exemptions under the new anti-abuse provisions. Without this evidence, the standard 15% Dutch dividend withholding tax applies automatically to your distributions.

Follow these steps to secure dividend withholding tax exemptions for non-resident shareholders:

- Verify treaty eligibility: Confirm the recipient entity resides in the EU/EEA or a jurisdiction with an active tax treaty with the Netherlands.

- Pass the Principal Purpose Test (PPT): Document that the holding structure exists for commercial reasons rather than to obtain a tax advantage.

- Confirm beneficial ownership: Provide financial evidence showing the recipient entity has the right to use the dividend without an obligation to pass it to another party.

- Compile substance proof: Attach the company's approved substance indicators. This includes local office leases and director residency certificates.

- Submit Form IB 92: File the official dividend tax return form with the Dutch Tax Authorities within one month of the dividend declaration.

Estimated Annual Compliance and Audit Costs

Maintaining a compliant holding company in the Netherlands requires a budget for local governance, accounting, and regulatory filings. Foreign investors should expect total annual compliance and audit costs to range from €7,500 to €14,000.

This baseline budget covers the local services needed to keep the entity in good standing. Costs scale upward based on transaction volume and asset portfolio complexity.

| Service Category | Estimated Annual Cost | Description |

|---|---|---|

| Local Director Fees | €3,000 - €6,000 | Independent resident directors |

| Accounting & Tax | €2,500 - €4,500 | Corporate income tax, VAT, financial statements |

| Legal Maintenance | €500 - €1,000 | Chamber of Commerce registrations, secretarial work |

| Audit Fees | €1,500 - €2,500 | Statutory audits triggered by company size or assets |

Common Misconceptions About Dutch Holding Companies

Foreign investors often operate under outdated assumptions about Dutch corporate tax planning. This leads to compliance failures under the 2026 regulations.

Many believe that renting a desk at a local trust office satisfies substance requirements. This is false under current EU directives. The law requires dedicated and exclusive premises.

Investors also assume that obtaining a tax ruling at incorporation guarantees permanent tax benefits. The Dutch tax authorities monitor substance continuously. They can revoke treaty benefits retroactively if economic activity drops.

Finally, some assume Dutch holding companies pay zero tax automatically. The participation exemption is a powerful tool, but it only applies when you meet strict ownership and substance criteria continuously.

When to Hire a Corporate Tax Lawyer

You need a corporate tax professional if you are restructuring an international holding group or setting up a new Dutch entity. The intersection of Dutch domestic law and EU directives is complex. Administrative oversights can cause a complete loss of tax exemptions. A lawyer is necessary if your company receives a formal inquiry from the tax authorities regarding economic substance or if you need to draft local management agreements that comply with ATAD 3.

Next Steps for Foreign Investors

Conduct a substance audit of your existing or planned Dutch holding structure. Review your office lease agreements, evaluate the residency status of your board members, and verify that your local economic activity meets the 2026 requirements.

If your setup relies on shared trust offices or non-resident management, transition to exclusive office space and local directorship. To restructure your operations and meet these mandates, connect with specialized corporate and commercial lawyers in the Netherlands to review your international tax strategy.