- The Netherlands is a preferred jurisdiction for private equity due to its tax treaties, legal stability, and flexible corporate forms like the Besloten Vennootschap (BV) and Commanditaire Vennootschap (CV).

- Foreign investors must comply with the Dutch Financial Supervision Act (Wft) and register Ultimate Beneficial Owners (UBOs) under EU transparency rules.

- Legal due diligence and deal structuring for a mid-market transaction cost between €50,000 and €150,000.

- Dutch entities require economic substance to qualify for the participation exemption and avoid conditional withholding taxes on repatriated funds.

Legal Frameworks Governing Foreign Private Equity

Foreign private equity transactions in the Netherlands are primarily governed by the Dutch Civil Code (Burgerlijk Wetboek) and the Financial Supervision Act (Wet op het financieel toezicht, Wft). These laws dictate entity formation and director duties while regulating fund management.

The Dutch Authority for the Financial Markets (AFM) enforces the Alternative Investment Fund Managers Directive (AIFMD) under Dutch law. Foreign private equity managers must obtain a full AIFM license or register under the "small managers" regime depending on fund size. The Dutch Central Bank (DNB) oversees prudential supervision. Failing to secure regulatory clearances before marketing to Dutch investors or closing a transaction results in financial penalties and voided agreements.

Alternative Investment Vehicles in the Netherlands

The primary private equity vehicles in the Netherlands are the private limited liability company (BV), the limited partnership (CV), and the cooperative (Coöperatie). Vehicle selection depends on tax strategy, liability requirements, and the home jurisdiction of the limited partners (LPs).

| Investment Vehicle | Legal Characteristics | Typical Private Equity Use Case | Tax Treatment |

|---|---|---|---|

| BV (Besloten Vennootschap) | Private company with shares. No minimum capital requirement. | Holding companies, BidCos (acquisition vehicles), and operating companies. | Tax-opaque. Subject to Dutch corporate income tax, eligible for participation exemption. |

| CV (Commanditaire Vennootschap) | Limited partnership with managing (general) and silent (limited) partners. | Fund aggregation vehicles and pooling entities for LPs. | Generally tax-transparent if structured properly. LPs are taxed in their home jurisdictions. |

| Coöperatie | Association acting as a business entity with members instead of shareholders. | Top-tier holding structures or joint ventures. | Can be structured to manage dividend withholding taxes. Anti-abuse rules apply. |

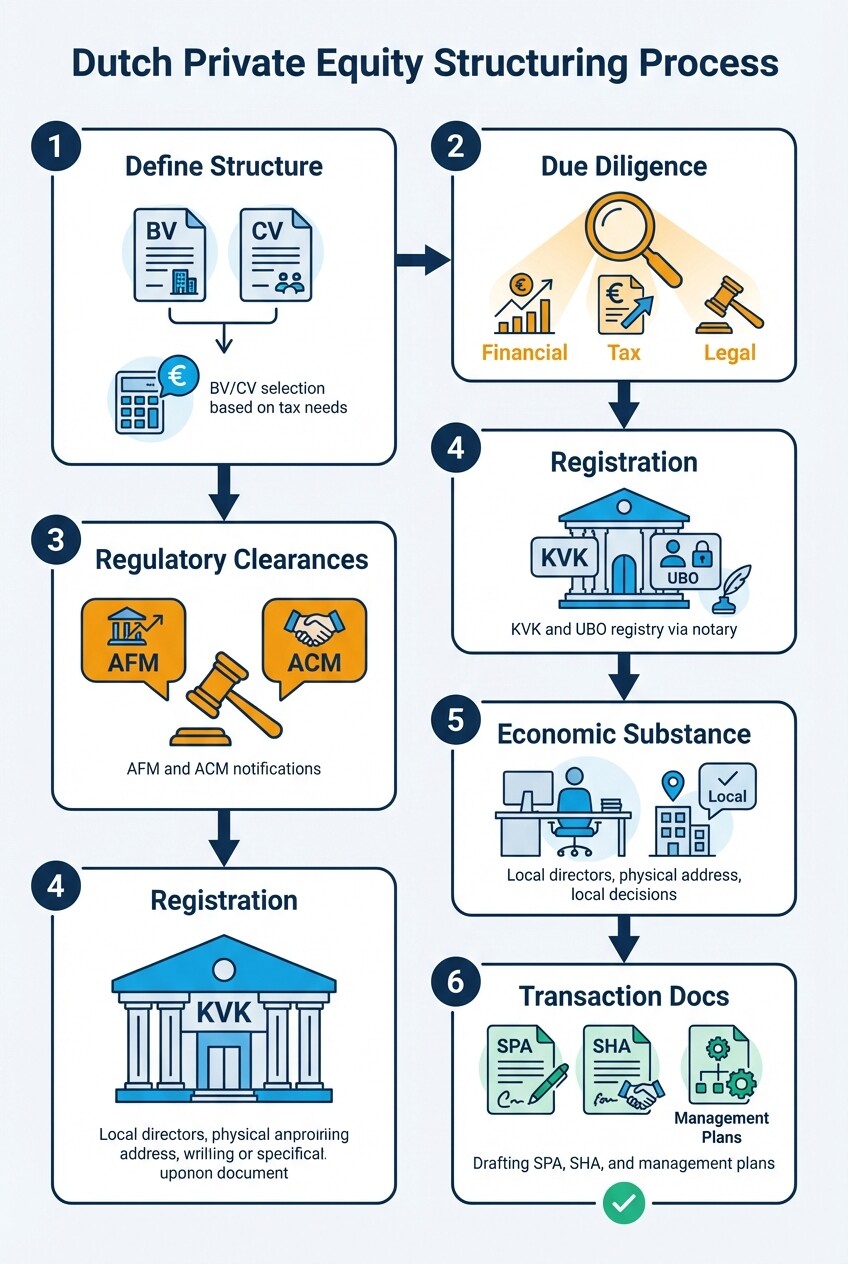

Private Equity Structuring Checklist

Structuring a private equity investment in the Netherlands requires sequential regulatory clearances, tax structuring, and entity formation. Skipping steps in the initial formation phase delays funding and complicates exits.

- Define the structure: Choose the appropriate acquisition vehicle (typically a BV) and fund pooling vehicle (typically a CV) based on LP tax residences.

- Conduct due diligence: Execute financial, tax, and legal due diligence on the Dutch target. Focus on employment liabilities and intellectual property ownership.

- Clear regulatory requirements: File notifications with the AFM to market the fund locally. Submit merger control filings to the Authority for Consumers and Markets (ACM) if revenue thresholds are met.

- Register entities and UBOs: Incorporate the entities via a Dutch civil-law notary and register them with the Commercial Register (KVK). Simultaneously file the ultimate beneficial owners with the official UBO register.

- Establish economic substance: Appoint qualified local resident directors, maintain a local physical address, and ensure major strategic decisions are formally minuted in the Netherlands.

- Draft transaction documents: Finalize the Share Purchase Agreement (SPA), Shareholders' Agreement (SHA), and management participation plans.

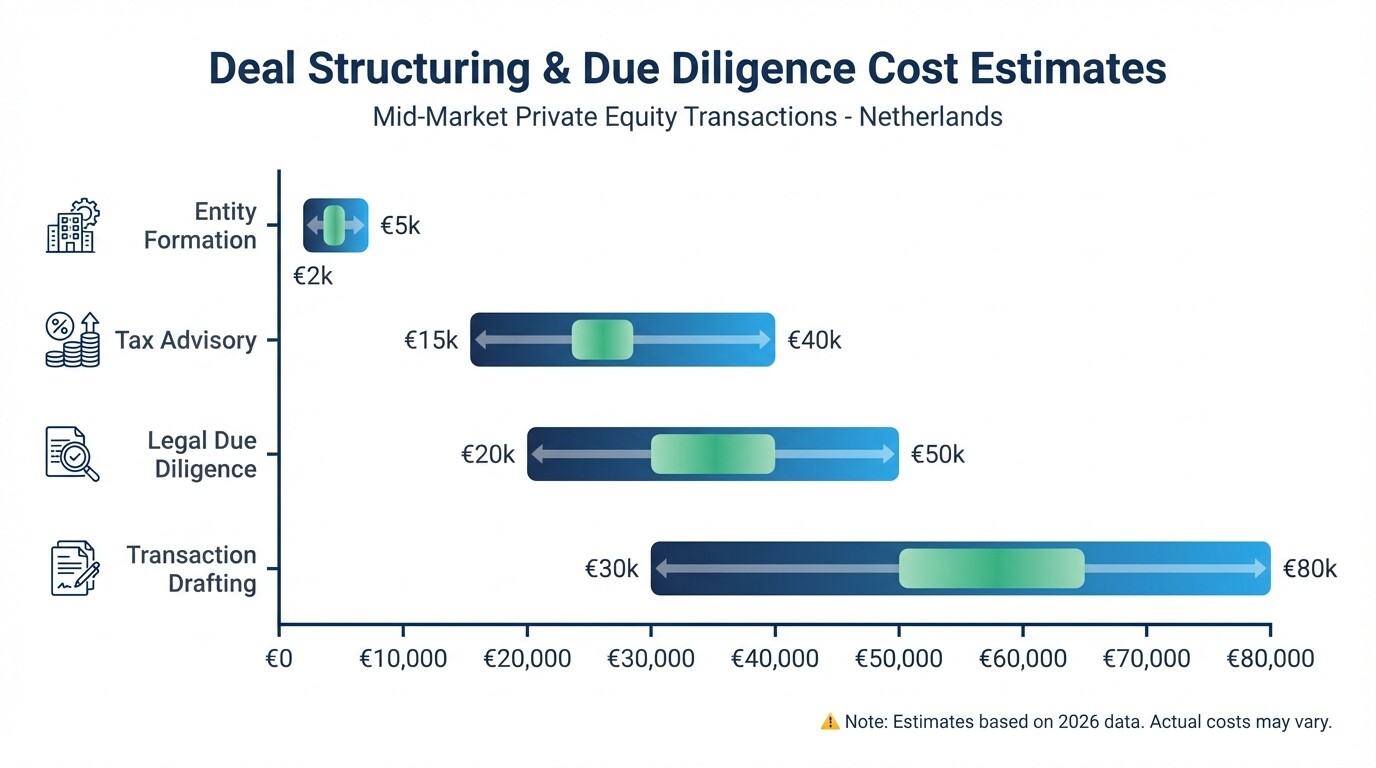

Cost Estimates for Deal Structuring and Legal Due Diligence

Legal structuring and due diligence for a mid-market private equity transaction in the Netherlands cost between €50,000 and €150,000. Costs vary based on target company size, regulatory complexity, and financing structure.

- Entity formation: €2,000 to €5,000 per entity. Dutch law requires a civil-law notary to execute the deeds of incorporation and share transfers.

- Legal due diligence: €20,000 to €50,000. This covers a review of corporate governance, material contracts, employment agreements, and regulatory compliance.

- Transaction drafting: €30,000 to €80,000. Costs increase with complex management incentive plans (MIPs) or layered debt financing terms.

- Tax advisory: €15,000 to €40,000. This is necessary to secure advance tax rulings (ATRs) and ensure the structure qualifies for the participation exemption.

Cross-Border Tax Implications and Corporate Compliance

Structuring through the Netherlands provides access to a tax treaty network and the participation exemption. It requires adherence to economic substance requirements and EU anti-abuse rules. The Dutch tax authority (Belastingdienst) scrutinizes foreign-owned structures to identify artificial arrangements designed to avoid taxation.

The participation exemption exempts qualifying dividends and capital gains from Dutch corporate income tax (CIT) if the holding company owns at least 5% of the target and the target is not a low-taxed portfolio investment.

Investors face a 15% statutory dividend withholding tax when repatriating profits. Exemptions exist for EU/EEA entities and treaty partners. The Netherlands enforces a 25.8% conditional withholding tax on dividends, interest, and royalties paid to entities in low-tax jurisdictions. Avoidance of this tax requires operational substance. The Dutch holding entity must incur local operational expenses and employ local management while assuming localized risk.

Common Misconceptions About Dutch Private Equity Structuring

International investors sometimes assume the Netherlands is an unregulated tax haven where setting up a holding company bypasses global withholding taxes. Domestic and EU regulatory changes have tightened compliance.

- Mailbox companies: Incorporating a BV is not enough to access tax treaties. Without demonstrable economic substance (local staff, active bank accounts, and local decision-making), tax authorities deny treaty benefits under the Principal Purpose Test (PPT).

- CV transparency: A Dutch CV is transparent for Dutch tax purposes, but foreign jurisdictions may view it differently. This creates hybrid mismatch arrangements, triggering double taxation under the EU Anti-Tax Avoidance Directive (ATAD).

- Employment laws: Foreign buyers underestimate Dutch labor laws. Restructuring a target post-acquisition requires consultation with a Works Council (Ondernemingsraad). This body has statutory rights to advise on and block major corporate decisions.

Exit Strategies and Execution Considerations

Tax-efficient exits

Private equity funds execute exits via share sales rather than asset sales. Under the Dutch participation exemption, capital gains realized by a Dutch holding company (BV) on the sale of shares in a qualifying target are exempt from corporate income tax.

Fund repatriation

Funds are repatriated through dividend distributions or a formal reduction of share capital. The standard dividend withholding tax is 15%. Funds domiciled in treaty countries or the EU/EEA can reduce this to 0% if the structure passes anti-abuse and economic substance tests.

Non-compete clauses

Non-compete clauses are enforceable under Dutch contract law if they are reasonable in scope, duration, and geographic area. In a share sale, courts allow broader non-competes than in standard employment contracts to protect the goodwill of the acquired business.

Foreign Direct Investment (FDI) screening

The Vifo Act (Wet Vifo) mandates that investments in Dutch companies operating in vital infrastructure or highly sensitive technologies be reported to the Bureau for Verification of Investments (BTI). Failing to notify authorities of a qualifying acquisition or exit results in the transaction being retroactively unwound.

When to Hire a Lawyer and Next Steps

Engage local legal counsel when you decide to domicile a fund in the Netherlands or sign a term sheet for a Dutch target. Early legal intervention ensures your investment vehicle aligns with cross-border tax treaties and your target undergoes proper due diligence for Works Council regulations and FDI screenings.

To proceed, gather your investment mandate, LP jurisdictional breakdown, and target financial summaries. Browse private equity lawyers in the Netherlands on Lawzana to find legal professionals who can execute your structuring strategy from incorporation through exit.