Foreign Direct Investment and M&A Regulatory Compliance in the UK

- Foreign acquirers must navigate the UK's National Security and Investment Act (NSIA), which imposes mandatory notifications for transactions in 17 sensitive economic sectors.

- Completing a transaction without mandatory clearance in a covered sector automatically voids the deal and exposes the parties to severe financial and criminal penalties.

- There are no minimum financial or market share thresholds for NSIA reviews; the UK government can scrutinize acquisitions of any size if they present a national security risk.

- Cross-border buyers can mitigate regulatory risk by structuring alternative joint ventures that keep voting rights and equity ownership below the critical 25% threshold.

- Post-merger success requires rapid alignment of corporate governance frameworks with the UK Companies Act 2006 and managing complex data integration under UK GDPR.

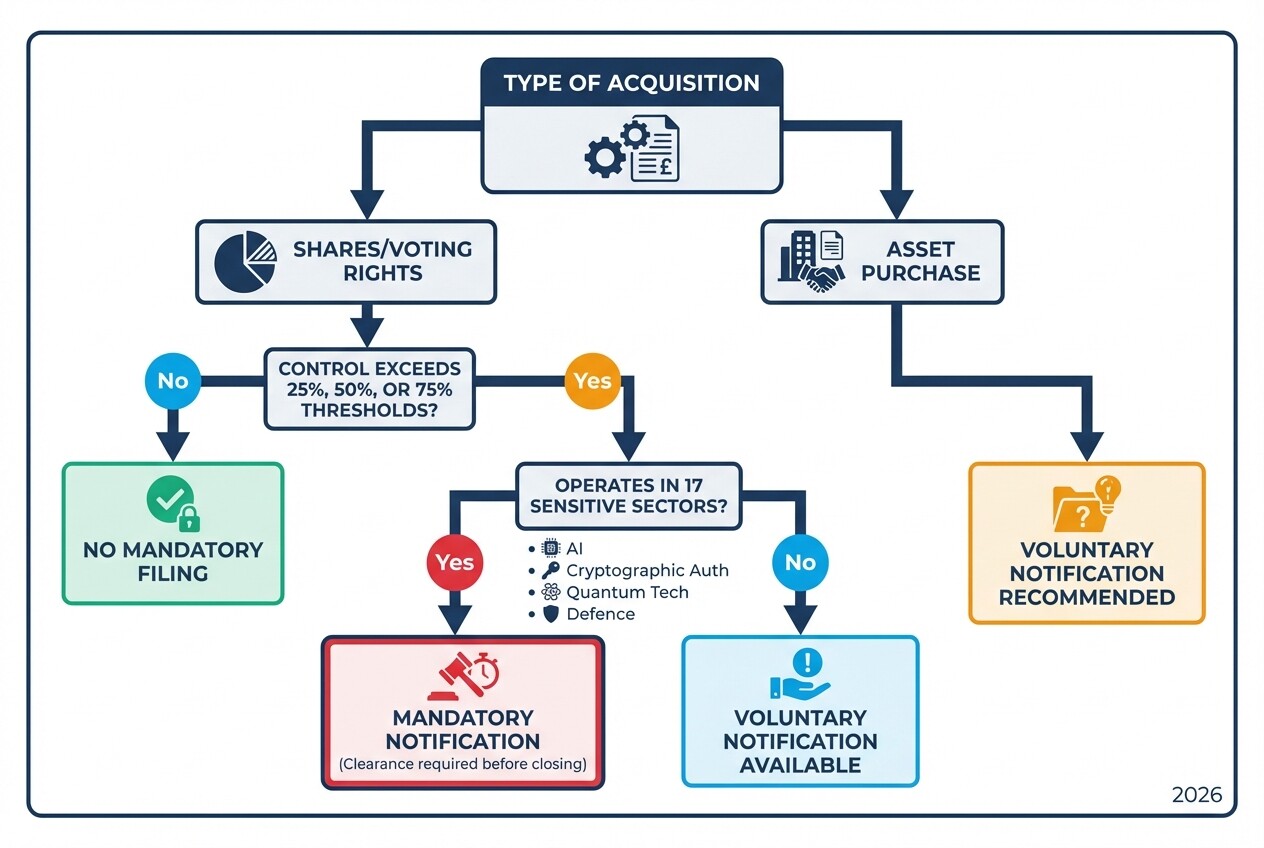

Mandatory vs. Voluntary Notification Triggers for Foreign M&A

The UK requires mandatory notification for share acquisitions in 17 sensitive sectors under the National Security and Investment Act 2021. Voluntary notification is available for transactions outside these core sectors, or for asset purchases, where national security risks might still prompt government intervention.

To determine if a transaction requires mandatory notification, foreign acquirers must assess both the target's activities and the level of control being acquired. Mandatory filings are triggered when an investor acquires more than 25%, 50%, or 75% of the votes or shares in a qualifying entity, or acquires voting rights that enable them to pass or block corporate resolutions.

The 17 mandatory sectors include, but are not limited to:

- Advanced Robotics and Artificial Intelligence

- Data Infrastructure and Communications

- Defense and Dual-Use Technologies

- Energy and Critical Suppliers to Government

- Advanced Materials and Quantum Technologies

If a deal does not meet the mandatory criteria-such as acquiring intellectual property rather than shares, or operating in a non-specified sector-parties can submit a voluntary notification. Choosing the voluntary route provides legal certainty, preventing the UK government from using its retroactive "call-in" power to unwind the deal up to five years after completion.

Cross-Border Regulatory Due Diligence Checklist and Common Pitfalls

Effective regulatory due diligence requires mapping the target company's operations against the NSIA's sensitive sectors and assessing their broader compliance framework. Overlooking even minor regulatory touchpoints can lead to delayed clearances, structural remedies, or blocked transactions.

International buyers frequently encounter legal pitfalls during due diligence, primarily by assuming that small revenue figures exempt a target from scrutiny. Another common pitfall is failing to identify indirect acquisitions, where buying a foreign parent company inadvertently triggers UK jurisdiction due to a UK-based subsidiary.

Use this diligence checklist to identify regulatory risks early in the M&A lifecycle:

- Map Sector Overlap: Audit all products, services, and R&D activities of the target against the precise definitions of the 17 NSIA sectors.

- Identify Government Contracts: Review existing and past supply agreements with the UK Ministry of Defence, intelligence agencies, or local governments.

- Trace Ultimate Beneficial Ownership (UBO): Document the exact corporate structure post-transaction to ensure all entities triggering the 25% threshold are identified.

- Assess Intellectual Property Transfers: Categorize patents, algorithms, and trade secrets that may require voluntary notification or export control licenses.

- Evaluate Antitrust Risk: Beyond national security, assess if the merger triggers a separate competition review by the Competition and Markets Authority (CMA) based on market share.

Managing the Timeline for UK Government Clearance and Intervention

The UK government has an initial 30 working days to review an accepted NSIA notification and decide whether to clear the transaction or call it in for full assessment. If a deal is called in, the review period extends for an additional 30 working days, with the potential for further extensions if complex national security issues arise.

Managing this timeline is critical for cross-border deal execution. Buyers must account for regulatory delays in their transaction documents, often negotiating longer "long-stop dates" (the deadline by which the deal must close) to accommodate potential government intervention.

| Clearance Phase | Typical Timeline | Action / Outcome | | : | : | : | | Pre-Notification | 1-3 Weeks | Drafting the filing, gathering corporate data, and submitting via the digital portal. | | Acceptance Review | 3-5 Working Days | The Investment Security Unit (ISU) reviews the submission for completeness before starting the clock. | | Initial Review | Up to 30 Working Days | The ISU evaluates the deal. Outcome: Clearance granted or a "Call-in" notice issued. | | Full Assessment | 30 Working Days | Detailed security review for called-in deals. Outcome: Final order clearing, blocking, or imposing conditions. | | Voluntary Extension | Up to 45 Working Days | Additional time agreed upon by the government and the acquirer to negotiate mitigation remedies. |

Structuring Alternative Joint Ventures to Mitigate Foreign Investment Risks

When outright acquisitions trigger insurmountable regulatory hurdles, international buyers often use alternative joint ventures to access UK markets and technologies. These structures can limit voting control and equity ownership below the 25% mandatory NSIA threshold, keeping the transaction outside the scope of mandatory clearance.

By structuring a deal as a strategic alliance or a contractual joint venture, a foreign investor can collaborate with a UK entity without assuming legal control. This approach is highly effective for cross-border technology sharing and co-development projects.

Strategic structuring options include:

- Minority Equity Investments: Acquiring less than 25% of shares while securing financial returns, ensuring no board veto rights are attached that could constitute material influence.

- Contractual Joint Ventures: Forming a partnership based entirely on commercial contracts rather than creating a new jointly-owned corporate entity.

- Licensing and R&D Agreements: Providing funding to a UK company in exchange for global licensing rights to the intellectual property developed, avoiding share ownership altogether.

Post-Merger Integration Challenges and Corporate Governance Requirements

Post-merger integration in the UK requires foreign acquirers to align corporate governance with the UK Companies Act 2006 and manage complex employee transitions under TUPE regulations. Successful integration demands the immediate harmonization of board structures, reporting lines, and compliance protocols to ensure seamless operations.

Foreign directors appointed to UK boards face strict statutory duties, including the obligation to promote the success of the company and avoid conflicts of interest. International parent companies must also be cautious of acting as a "shadow director," where the UK board merely rubber-stamps decisions made abroad, exposing the parent company to direct legal liability in the UK.

Additionally, integrating IT systems and transferring customer data across borders requires strict adherence to UK GDPR. Acquirers must establish secure data transfer mechanisms and update privacy notices before consolidating global databases.

Common Misconceptions About UK Foreign Direct Investment

International acquirers frequently misunderstand the scope of the UK's regulatory regime, often assuming that small deal sizes or non-defense sectors are exempt from scrutiny. These assumptions routinely lead to critical deal delays, compliance breaches, or the discovery of voided transactions post-closing.

- Misconception: Small deals are exempt. Unlike UK competition law, the NSIA has no minimum financial turnover or market share thresholds. The acquisition of a pre-revenue startup holding sensitive quantum computing patents is just as susceptible to review as a multi-billion-pound corporate buyout.

- Misconception: Asset purchases do not require government attention. While asset purchases (like buying machinery, land, or intellectual property) do not trigger mandatory filings, the UK government actively monitors these deals and can call them in for review. Submitting a voluntary filing is highly recommended for sensitive assets.

- Misconception: Foreign-to-foreign mergers are ignored. If a US company buys a German company that has a UK subsidiary operating in a sensitive sector, the UK's mandatory notification rules still apply. Ignoring indirect acquisitions is a frequent and costly error in global M&A.

FAQs on UK M&A Compliance

What are the penalties for failing to submit a mandatory NSIA notification?

Completing a transaction without mandatory clearance automatically voids the deal under UK law. Additionally, the government can impose civil fines of up to 5% of the global corporate group's turnover or £10 million (whichever is higher), alongside potential criminal prosecution for executives.

Can the UK government review completed transactions retroactively?

Yes. The government can retroactively call in a transaction for review up to five years after it has completed, or within six months of becoming aware of it. This power underscores the strategic value of submitting a voluntary notification to gain legal certainty.

Does UK merger control apply alongside the National Security and Investment Act?

Yes. The NSIA operates entirely separately from antitrust regulations. A transaction may require both an NSIA clearance for national security and a separate filing to the Competition and Markets Authority (CMA) if it meets the relevant market share or turnover thresholds.

How long does a voluntary notification take to process?

The timeline for a voluntary notification is identical to a mandatory one. Once the Investment Security Unit accepts the filing, they have a statutory limit of 30 working days to either clear the transaction or call it in for further review.

When to Hire an M&A Lawyer

Engaging legal counsel early in the deal lifecycle is critical to determining filing requirements, conducting regulatory due diligence, and drafting a transaction agreement that protects you from intervention delays. Corporate transactions involving cross-border entities are complex, and regulatory missteps can permanently collapse a deal. Experienced United Kingdom M&A lawyers can structure the transaction, manage the communication with the Investment Security Unit, and negotiate appropriate condition precedent clauses.

Next Steps

- Assess Sector Overlap: Before signing any letters of intent, analyze the target company's products and services against the 17 sensitive sectors defined by the UK government.

- Structure the Deal Strategy: Determine whether the transaction requires a mandatory filing, warrants a voluntary filing, or should be restructured as an alternative joint venture to minimize risk.

- Draft Conditional Contracts: Ensure your Share Purchase Agreement (SPA) includes robust condition precedent clauses, stating that the transaction will only close upon successful regulatory clearance from the UK authorities.