US HSR Act Merger Filings FAQ: 2026 Antitrust Guide for Foreign Acquirers

- The Hart-Scott-Rodino (HSR) Act requires foreign acquirers to notify the US government before completing mergers that meet specific financial thresholds.

- Government filing fees for 2026 are tiered based on transaction value, ranging from approximately $30,000 to $2.25 million.

- Transactions involving foreign buyers often trigger parallel national security reviews by the Committee on Foreign Investment in the United States (CFIUS).

- Failing to file an HSR notification carries civil penalties exceeding $50,000 per day and the risk of the government unwinding the transaction.

- Alternative deal structures, such as passive minority investments, can sometimes minimize antitrust risk and avoid lengthy agency investigations.

2026 Hart-Scott-Rodino (HSR) Act Filing Thresholds

For 2026, foreign acquirers must file a premerger notification if a transaction meets the revised statutory thresholds, which are adjusted annually based on the gross national product. The core jurisdictional test requires assessing both the size of the transaction and the size of the parties involved.

The Federal Trade Commission (FTC) updates these thresholds at the beginning of each year. To trigger a filing requirement, a cross-border merger typically must satisfy three primary tests:

- Size of Transaction Test: The acquirer will hold an aggregate amount of voting securities, non-corporate interests, or assets of the target company exceeding the base threshold (projected to be over $120 million for 2026).

- Size of Person Test: For transactions valued below the absolute threshold (typically around $480 million), one party must have total assets or annual net sales of at least the higher threshold (around $240 million), and the other party must meet the lower threshold (around $24 million).

- US Nexus Exemption: Under rules 802.50 and 802.51, foreign-to-foreign transactions are exempt if the target's US assets or sales in or into the United States fall below the base transaction threshold.

Companies must consult the official Federal Trade Commission HSR thresholds prior to closing any international merger to confirm current jurisdictional requirements.

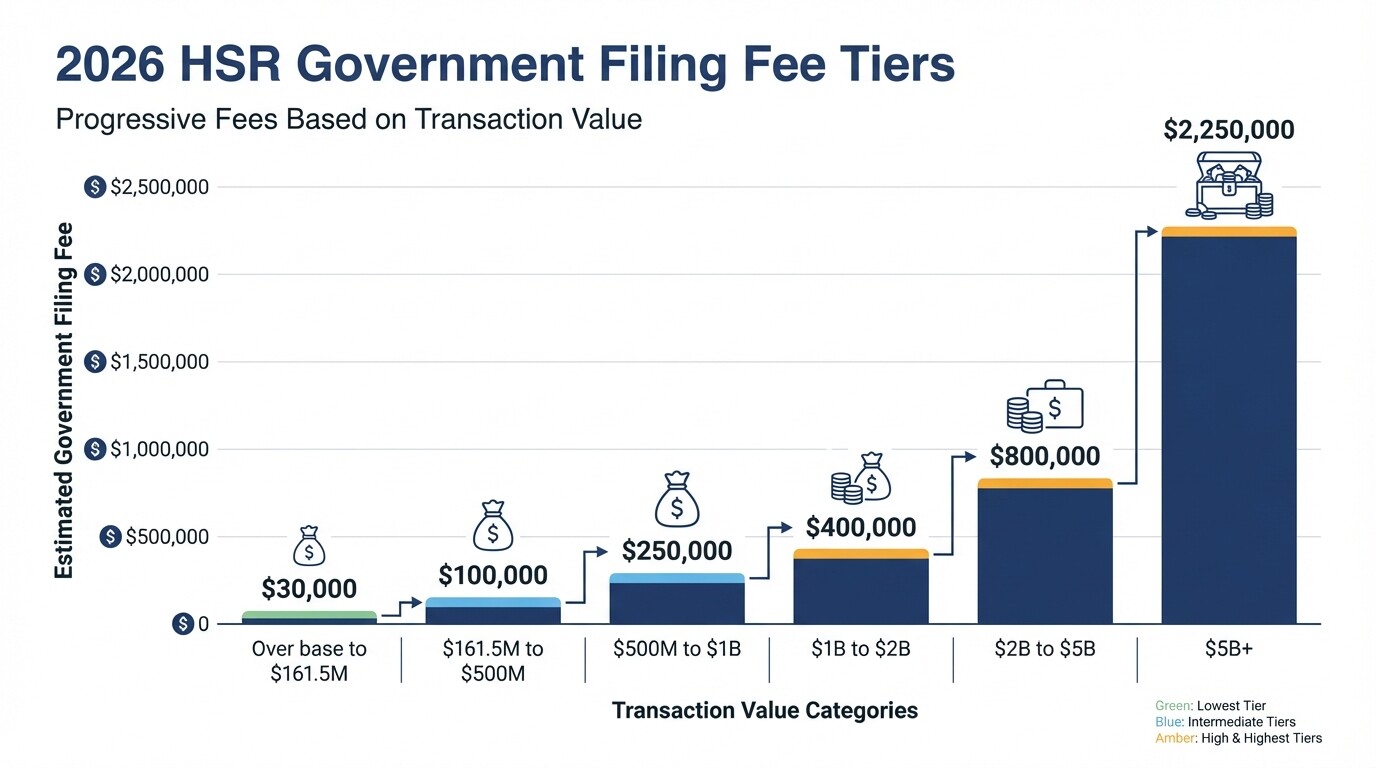

Estimated Legal Costs and Government Filing Fees

Government filing fees for HSR reviews range from $30,000 to $2.25 million, depending entirely on the total value of the proposed transaction. When combined with legal counsel and economic analysis, total costs for an uncontested filing typically exceed $100,000.

The Merger Filing Fee Modernization Act introduced a highly progressive fee structure. While the exact figures adjust slightly with inflation, foreign buyers should budget based on the following general tiers for 2026:

| Transaction Value | Estimated Government Filing Fee |

|---|---|

| Over base threshold to $161.5 million | $30,000 |

| $161.5 million to $500 million | $100,000 |

| $500 million to $1 billion | $250,000 |

| $1 billion to $2 billion | $400,000 |

| $2 billion to $5 billion | $800,000 |

| $5 billion or more | $2,250,000 |

Beyond government fees, acquirers must factor in professional costs. Preparing a standard HSR filing involves significant document collection, competitive overlap analysis, and coordination among global teams. Uncontested filings typically incur $50,000 to $100,000 in legal fees. If the government initiates an in-depth investigation, legal and economic expert costs can rapidly escalate into the millions.

Alternative Transaction Structures to Minimize Antitrust Risk

Restructuring a deal can legally bypass HSR filing requirements or reduce the likelihood of a lengthy antitrust investigation. Foreign buyers often use joint ventures, minority investments, or staggered acquisitions to stay below jurisdictional thresholds.

When planning a US market entry or expansion, consider these structural alternatives to mitigate antitrust friction:

- Passive Minority Investments: The "investment-only" exemption applies if a buyer acquires 10% or less of a company's voting securities solely for investment purposes, with no intention of participating in basic business decisions.

- Asset Carve-Outs: Instead of acquiring an entire global entity, buyers can acquire specific foreign assets while excluding the US assets and revenue streams, keeping the transaction's US nexus below the filing threshold.

- Non-Corporate Entity Investments: Acquiring interests in a Limited Liability Company (LLC) or partnership only triggers an HSR filing if the buyer gains "control" (the right to 50% or more of profits or assets upon dissolution). Acquiring a 49% stake in an LLC avoids the filing requirement, unlike acquiring 49% of voting securities in a corporation.

- Licensing Agreements: Structuring a transaction as an exclusive or non-exclusive intellectual property license, rather than an outright asset transfer, may avoid HSR scrutiny if structured correctly to avoid transferring all commercially significant rights.

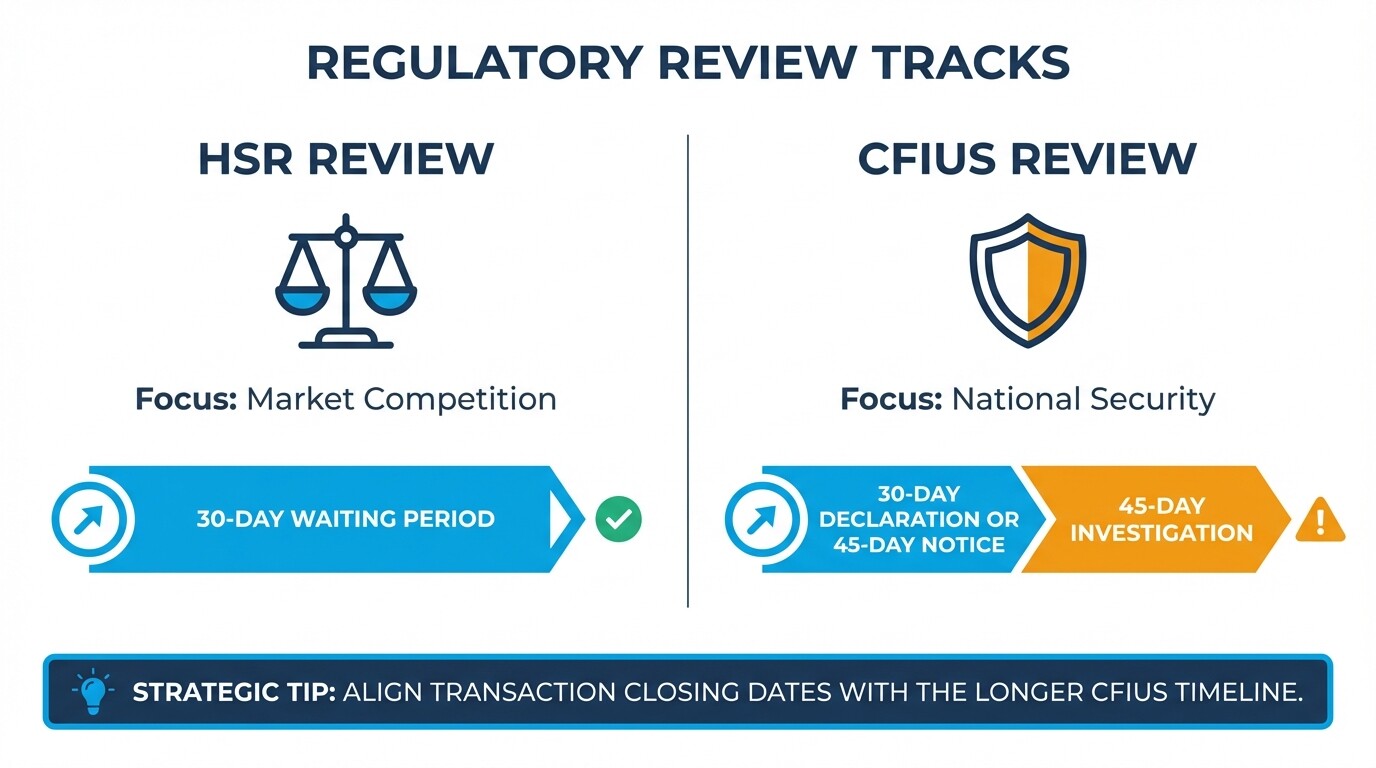

Navigating the Intersection of HSR and CFIUS

Foreign acquirers must manage HSR antitrust filings simultaneously with Committee on Foreign Investment in the United States (CFIUS) national security reviews. While the FTC evaluates market competition, CFIUS assesses whether foreign control over a US business threatens national security.

These parallel regulatory reviews operate on entirely different timelines and objectives. To navigate this intersection effectively:

- Assess Mandatory Filing Triggers: CFIUS filings are mandatory for certain transactions involving US critical technology, critical infrastructure, or sensitive personal data (TID US businesses). HSR filings are purely financial and structural.

- Sequence Regulatory Timelines: The HSR waiting period is typically 30 days. CFIUS reviews begin with a 30-day declaration assessment or a 45-day notice review, often followed by a 45-day investigation. Buyers should align closing dates with the longer CFIUS timeline.

- Coordinate Information Sharing: Agencies increasingly share information. Ensure consistency in how the transaction's rationale, market impact, and post-merger governance are described in both HSR and CFIUS submissions.

Finding experienced antitrust litigation lawyers in the United States who frequently collaborate with CFIUS counsel is vital for preventing conflicting agency narratives.

Strategies for Responding to FTC Second Requests

A Second Request is a detailed demand for documents and data issued when the government needs more information to evaluate competitive effects. Responding efficiently requires immediate data preservation, negotiating scope limitations with regulators, and using advanced e-discovery tools.

Receiving a Second Request halts the transaction waiting period until the parties substantially comply. To accelerate clearance, foreign acquirers should implement the following strategies:

- Negotiate Custodian Limits: Promptly engage with FTC or Department of Justice (DOJ) staff to reduce the number of executives and employees whose files must be searched.

- Use Technology-Assisted Review (TAR): Leverage predictive coding and artificial intelligence to filter millions of documents rapidly. Agencies generally accept TAR if the methodology is transparent and validated early in the process.

- Address Foreign Data Privacy Conflicts: Foreign acquirers often face conflicts between US document production demands and local data privacy laws (like the GDPR). Legal teams must negotiate production modifications to satisfy US regulators without violating foreign statutes.

- Draft a Timing Agreement: Negotiate a formal agreement governing the pace of document production and the schedule for agency depositions to create a predictable timeline for deal closure.

Common Misconceptions About US Antitrust Filings

Many foreign executives misunderstand US antitrust laws, assuming that a lack of US headquarters exempts them from regulatory scrutiny. Clarifying these misconceptions prevents severe financial penalties and delayed deal closures.

- Myth 1: Foreign-to-foreign mergers are exempt. Even if both the buyer and the target are located outside the United States, an HSR filing is required if the target generates sufficient sales into the US or holds sufficient US assets to meet the jurisdictional thresholds.

- Myth 2: Submitting a filing guarantees antitrust clearance. The HSR process is only a premerger notification. Expiration of the waiting period allows the deal to close, but the FTC or DOJ retains the authority to challenge a consummated merger years later if it harms competition.

- Myth 3: A small market share eliminates the need to file. The HSR Act is a strict liability statute based on transaction size, not market power. Even if the merging parties operate in entirely different industries with zero market overlap, a filing is required if the financial thresholds are met.

Frequently Asked Questions (FAQ)

What is the standard waiting period for an HSR filing?

The initial waiting period is 30 days after both parties submit their complete filings. For cash tender offers or specific bankruptcy transactions, the waiting period is reduced to 15 days. If the government issues a Second Request, the waiting period is suspended.

Are there penalties for failing to file an HSR notification?

Yes, parties that fail to file or prematurely integrate their businesses ("gun-jumping") face severe civil penalties. The statutory maximum penalty is adjusted annually for inflation and currently exceeds $50,000 per day of noncompliance.

Can the government block a merger involving foreign companies?

Yes. If the FTC or DOJ determines that a transaction will substantially lessen competition within the United States market, they can seek a federal court injunction to block the merger globally or force the divestiture of US-facing business units.

Do joint ventures require an HSR filing?

The formation of a corporate joint venture or an LLC can trigger an HSR filing if the transaction meets the financial thresholds and at least one party will acquire "control" of the newly formed entity.

Next Steps and When to Hire an Antitrust Lawyer

Engaging specialized legal counsel early in the deal negotiation phase is essential for cross-border mergers. An antitrust lawyer will conduct a threshold analysis, manage agency communications, and coordinate simultaneous national security reviews.

Do not wait until a letter of intent is signed to consider antitrust implications. Start by taking the following steps:

- Calculate the precise transaction value according to HSR valuation rules, which differ from standard accounting principles.

- Compile a preliminary list of overlapping global product lines and relevant US sales data.

- Consult qualified antitrust litigation lawyers to map out a regulatory timeline and draft necessary risk-allocation clauses (such as reverse breakup fees or divestiture caps) in the merger agreement.