- Secondary Sanctions Are Expanding: The Office of Foreign Assets Control (OFAC) is aggressively leveraging secondary sanctions, meaning foreign financial institutions (FFIs) can lose access to the US financial system even if transactions involve no US persons or US dollars.

- Voluntary Self-Disclosure is Critical: Proactively reporting a sanctions violation to OFAC through a Voluntary Self-Disclosure (VSD) can reduce baseline civil monetary penalties by up to 50%.

- Strict Recordkeeping: US law mandates that institutions retain comprehensive records of sanctions screening and blocked transactions for a minimum of five years.

- Compliance is Costly but Necessary: Establishing a compliant infrastructure typically requires a first-year investment of $150,000 to $500,000 for mid-sized institutions, offsetting the risk of penalties that regularly exceed tens of millions of dollars.

What Are the Key OFAC Updates and Secondary Sanctions Risks for 2026?

The Office of Foreign Assets Control (OFAC) is intensifying its focus on secondary sanctions in 2026, targeting foreign financial institutions that facilitate significant transactions for sanctioned entities. Even operating entirely outside the United States without US dollars, FFIs risk losing access to US correspondent banking networks if they engage in prohibited activities involving jurisdictions like Russia or Iran.

Secondary sanctions are essentially a choice forced upon foreign entities: stop doing business with targeted actors, or lose access to the US financial system. OFAC's recent enforcement actions highlight a shift from investigating purely US-nexus violations to scrutinizing global supply chains and cross-border payment flows.

To mitigate these risks in 2026, foreign banks must monitor:

- Expanded Executive Orders: New directives targeting foreign facilitators of military-industrial bases and illicit technology transfers.

- Correspondent Account Terminations: Under secondary sanctions authority, the US Treasury can instruct domestic banks to close the correspondent accounts of non-compliant FFIs.

- Strict Liability Enforcement: OFAC operates on a strict liability standard. A penalty can be assessed even if the foreign institution did not know the transaction violated US sanctions, provided they had reason to know based on available data.

Required Screening Documentation and Record Retention

OFAC requires institutions to maintain comprehensive records of all sanctions screening activities, alert adjudications, and blocked property reports for a minimum of five years. Failure to produce these documents during a regulatory audit or OFAC investigation is considered a separate, penalizable violation under US law.

Under Title 31, Chapter V of the Code of Federal Regulations, financial institutions must retain a highly structured paper trail. Your compliance department must systematically archive:

- Screening Logs: Timestamped records showing exactly which customer databases and transaction batches were screened against the Specially Designated Nationals (SDN) list.

- Alert Adjudication Memos: Detailed notes explaining why a potential screening match was discounted as a false positive (e.g., mismatched dates of birth or geographic locations).

- Blocked Property Reports: Copies of the initial and annual reports submitted to OFAC detailing any frozen assets.

- KYC and End-User Certificates: Due diligence documentation proving the institution investigated the ultimate beneficial owners (UBOs) of its corporate clients.

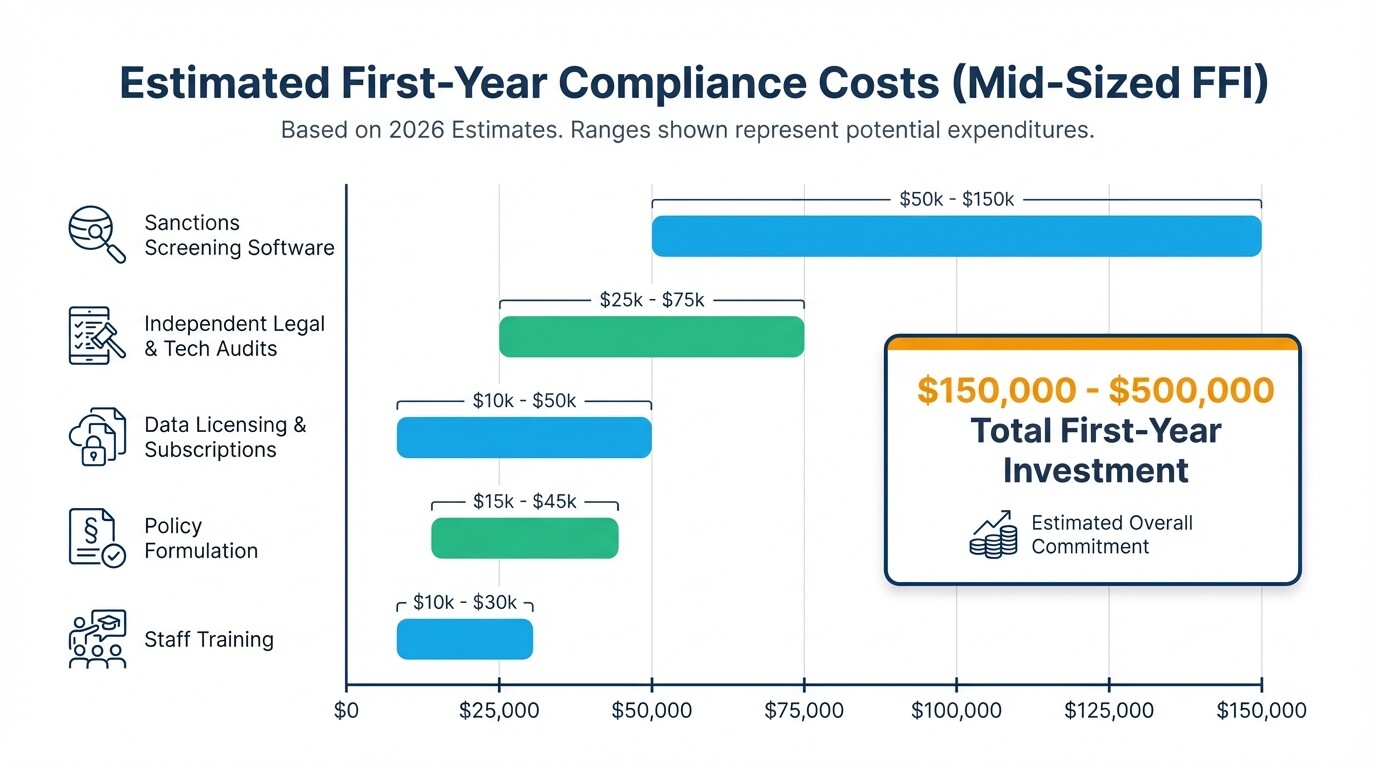

Projected Costs for Sanctions Compliance Implementation

For a mid-sized foreign financial institution, implementing a robust sanctions compliance infrastructure typically ranges from $150,000 to $500,000 in the first year. This budget must account for enterprise-grade screening software, database subscriptions, and independent legal and technical audits.

Attempting to cut corners on compliance technology often leads to catastrophic regulatory penalties. Below is a realistic breakdown of first-year implementation costs for a mid-market foreign bank establishing a US-compliant framework:

| Compliance Component | Estimated First-Year Cost (USD) | Description | | : | : | : | | Sanctions Screening Software | $50,000 - $150,000 | Integration of API-driven, fuzzy-logic screening systems for transactions and onboarding. | | Data Licensing & Subscriptions | $30,000 - $80,000 | Annual access to enriched watchlists (Dow Jones, Refinitiv) identifying UBOs and complex corporate structures. | | Independent Legal & Tech Audits | $40,000 - $120,000 | Retaining external counsel and auditors to test system effectiveness and perform gap analyses. | | Staff Training & Certification | $15,000 - $30,000 | Specialized OFAC training for compliance officers and frontline banking staff. | | Policy Formulation | $15,000 - $40,000 | Drafting custom, institution-specific Sanctions Compliance Program (SCP) manuals. |

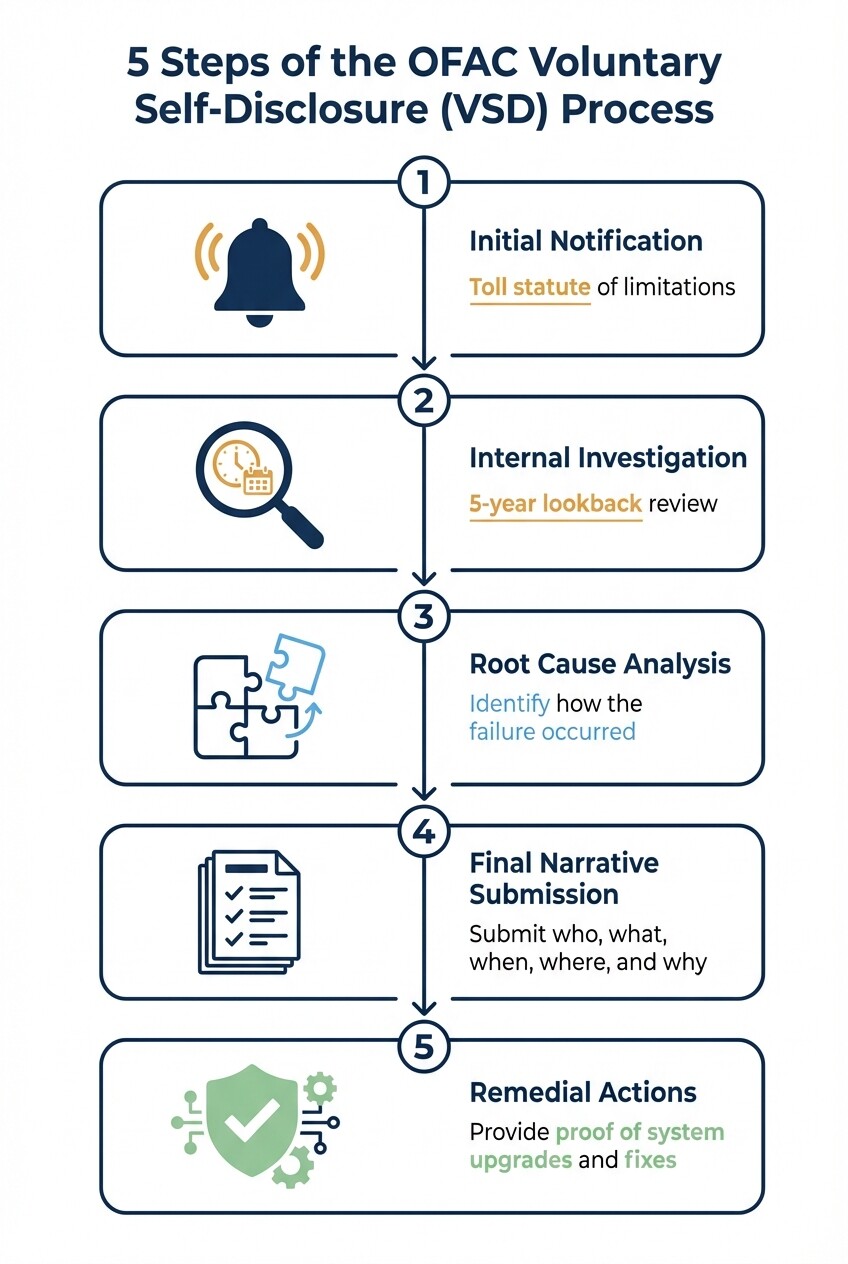

Step-by-Step Voluntary Self-Disclosure (VSD) Process

Filing a Voluntary Self-Disclosure (VSD) with OFAC can reduce base penalties by up to 50% if an institution discovers a sanctions violation. The process requires submitting an initial notification followed by a comprehensive narrative report and supporting evidence before OFAC discovers the violation independently.

Filing a VSD is a high-stakes legal maneuver. The standard step-by-step process includes:

- Initial Notification: Submit a brief initial notification to OFAC immediately upon discovering the potential violation. This tolls the statute of limitations and secures credit for self-disclosing before a third party reports it.

- Internal Investigation: Conduct a thorough lookback investigation, usually covering the previous five years. This involves reviewing transaction histories, emails, and KYC files to determine the scope of the violation.

- Root Cause Analysis: Identify exactly how the compliance failure occurred (e.g., outdated screening software, human error, circumvention by a client).

- Final Narrative Submission: Submit a detailed written report to OFAC outlining the who, what, when, where, and why of the transactions, alongside total monetary values.

- Remedial Actions: Provide documented proof of the steps the institution has taken to fix the root cause, such as firing responsible employees, upgrading software, or exiting high-risk client relationships.

Establishing a Resilient Internal Sanctions Compliance Program (SCP)

A defensible Sanctions Compliance Program (SCP) must align with OFAC's formalized framework, which centers on five essential components. These pillars demonstrate to US regulators that your institution takes a risk-based, proactive approach to compliance, which acts as a mitigating factor during any enforcement action.

To meet US regulatory expectations, FFIs must integrate these five elements:

- Management Commitment: The board of directors and senior executives must visibly allocate sufficient budget, authority, and autonomy to the compliance unit.

- Risk Assessment: The institution must conduct routine, documented assessments of its geographic reach, customer base, and product offerings to identify specific sanctions vulnerabilities.

- Internal Controls: Implementation of written policies, automated screening tools, and escalation procedures that halt prohibited transactions before execution.

- Testing and Auditing: An independent party-either an internal audit function or external sanctions and export controls lawyers in the United States-must regularly stress-test the screening software to ensure it catches name variations and structural circumvention.

- Training: Annual, role-specific training for all relevant employees, ensuring they understand both US law and the institution's specific internal controls.

Common Misconceptions About US Sanctions for FFIs

Many foreign banks mistakenly believe that operating entirely outside the United States shields them from OFAC jurisdiction. In reality, US sanctions enforcement mechanisms are highly extraterritorial and aggressively target the facilitation of prohibited transactions anywhere in the world.

- "We don't use US dollars, so OFAC doesn't apply to us." While clearing transactions in US dollars creates a direct US nexus, secondary sanctions do not require US currency. OFAC can sanction any foreign entity that provides material support or significant financial services to designated parties.

- "We didn't know our customer was routing money to a sanctioned country." OFAC enforces strict liability. Ignorance is not a defense if the regulator determines your institution failed to conduct adequate due diligence or ignored "red flags" that a reasonable compliance program would have caught.

Frequently Asked Questions

What happens if our screening software misses a sanctioned entity?

If your software fails to catch a sanctioned entity and a transaction is processed, it is a sanctions violation. You may face severe civil monetary penalties. However, if you can prove your software was regularly tested and the failure was an isolated anomaly, OFAC may consider this a mitigating factor when calculating penalties.

Do foreign branches of US banks have to comply with OFAC?

Yes. Foreign branches of US parent institutions are treated as US persons under OFAC regulations and must comply strictly with all primary US sanctions programs.

How long does it take OFAC to process a specific license application?

OFAC does not have a statutory deadline for processing specific license applications. Depending on the complexity of the request and the foreign policy implications, processing can take anywhere from a few months to over a year.

When to Hire a Sanctions Compliance Lawyer

Engage a US sanctions attorney immediately if you discover a potential violation, receive an administrative subpoena from OFAC, or plan to expand financial services into high-risk jurisdictions. Specialized legal counsel is critical for navigating the complexities of US financial regulations and protecting your institution's global banking access.

Retaining external counsel is particularly important when drafting a Voluntary Self-Disclosure or designing an independent audit. Legal professionals ensure that internal investigations are protected by attorney-client privilege where applicable, and they possess the institutional knowledge to negotiate effectively with Treasury officials.

Next Steps for Foreign Financial Institutions

Preparing for 2026 requires immediate action to stress-test your current compliance frameworks against evolving secondary sanctions. Begin by scheduling a comprehensive risk assessment of your cross-border payment flows and correspondent banking relationships. Upgrade your screening algorithms to account for new beneficial ownership rules, and ensure your recordkeeping policies are strictly aligned with the five-year retention mandate.