- Foreign nationals and foreign corporate entities can legally act as promoters, shareholders, and directors of a Section 8 company in India.

- At least one director on the board must be a resident of India, defined as having stayed in India for at least 136 days in the previous financial year.

- Foreign directors must obtain a Digital Signature Certificate (DSC) and have their identity documents notarized and apostilled in their home country.

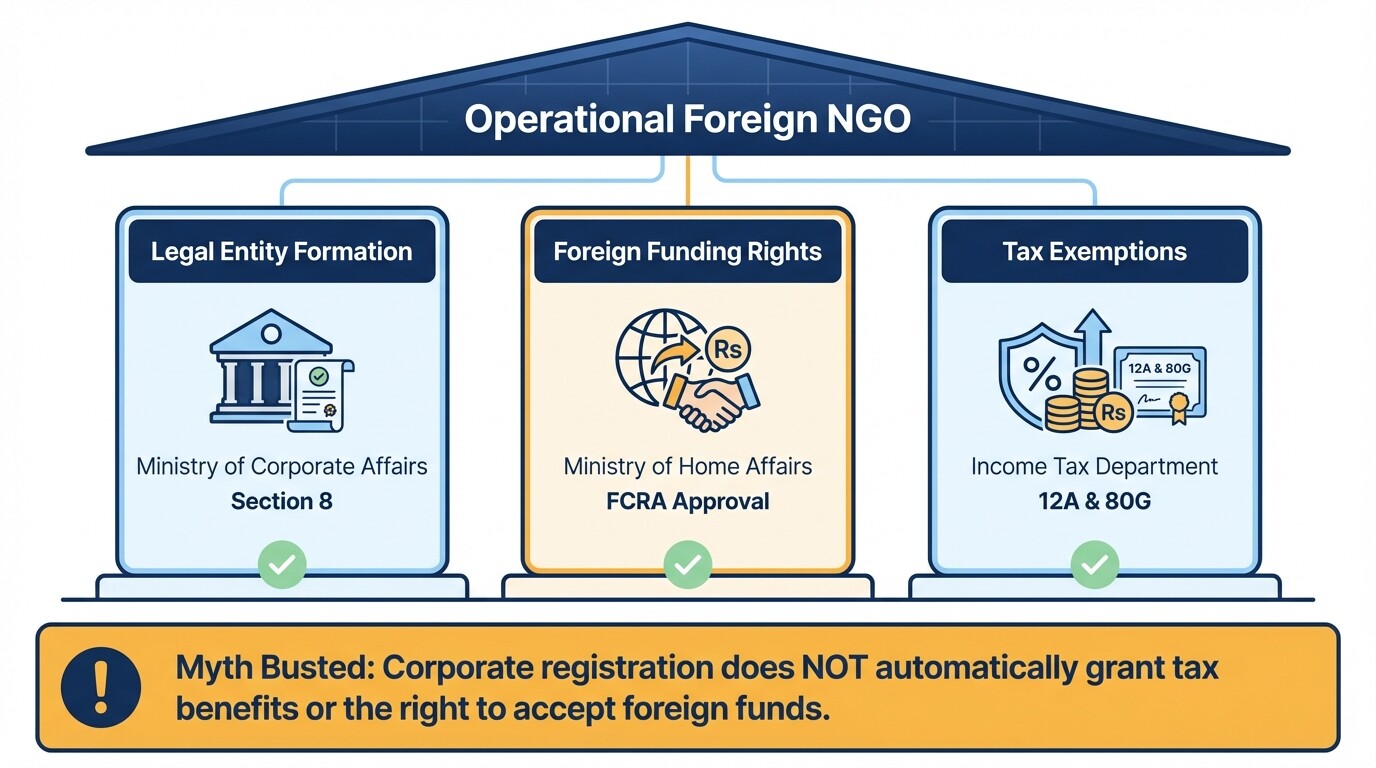

- Registering the entity does not automatically grant the right to accept foreign funds. You must separately obtain Foreign Contribution Regulation Act (FCRA) registration.

- Tax benefits require independent applications under Section 12A (tax exemption for the NGO) and Section 80G (tax deductions for donors) of the Income Tax Act.

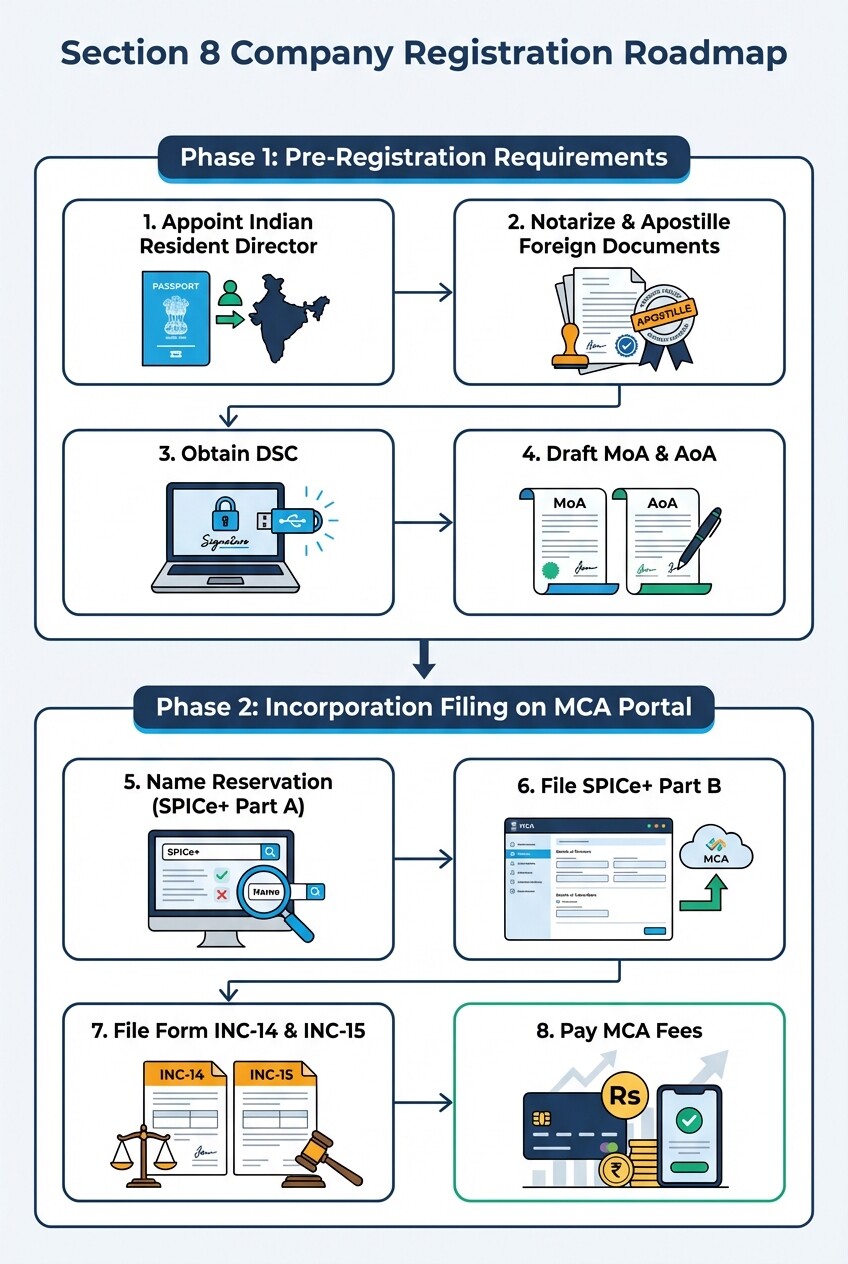

Section 8 Company Registration Checklist for Foreign Entities

Registering a Section 8 company for foreign charitable activities requires specific documentation, name reservation, and formal incorporation filings with the Ministry of Corporate Affairs (MCA). Follow this step-by-step checklist to ensure compliance and avoid application rejection.

Phase 1: Pre-Registration Requirements

- Appoint an Indian Resident Director: Identify at least one individual who meets the residency requirement (136 days in India during the previous financial year).

- Notarize and Apostille Foreign Documents: All foreign directors must have their passport, address proof, and identity proof notarized and apostilled in their home country.

- Obtain DSC: Procure a Digital Signature Certificate for all proposed directors and promoters.

- Draft MoA and AoA: Prepare the Memorandum of Association and Articles of Association detailing the specific charitable objectives.

Phase 2: Incorporation Filing on MCA Portal

- Name Reservation: Submit the SPICe+ Part A form to reserve a unique name that reflects the charitable nature of the organization (e.g., Foundation, Association, Council).

- File SPICe+ Part B: Submit the comprehensive incorporation form including director details, registered office address, and PAN/TAN applications.

- File Form INC-14 and INC-15: Submit declarations by practicing professionals and proposed directors confirming compliance with Section 8 requirements.

- Pay MCA Fees: Remit the official stamp duty and registration fees, which generally range from ₹5,000 to ₹15,000 depending on the authorized capital and state of registration.

Eligibility Criteria for Foreign Promoters in Section 8 Companies

Foreign nationals and international corporate entities are fully eligible to incorporate and serve as directors or promoters of a Section 8 company in India. The Companies Act 2013 permits 100% foreign direct ownership in non-profit companies without requiring prior government approval.

While foreign founders maintain complete control over the organization's vision, Indian corporate law mandates local representation on the board. You must appoint at least one Resident Indian Director to the board. To qualify as a resident, this individual must have stayed in India for a minimum of 136 days during the preceding financial year. For foreign promoters, providing identity and address proofs involves an extra layer of authentication. If the director's home country is a signatory to the Hague Convention, the documents must be notarized and apostilled. For non-Hague countries, documents require consularization by the Indian embassy in that specific country.

The Process of Obtaining a Digital Signature Certificate (DSC)

A Digital Signature Certificate is a mandatory electronic credential required for all foreign directors and promoters to securely sign incorporation forms on the Ministry of Corporate Affairs portal. Without a valid Class 3 DSC, foreign nationals cannot apply for a Director Identification Number (DIN) or file any company registration documents.

The process for a foreign national to obtain a DSC requires meticulous document preparation. The typical cost ranges from ₹2,000 to ₹4,500 per certificate.

- Submit the Application: Complete an application with a recognized Indian Certifying Authority (CA) through a registered professional.

- Provide Authenticated Proofs: Submit the notarized and apostilled copies of your passport, a recent photograph, and an address proof (like a bank statement or utility bill not older than two months).

- Complete Video Verification: The CA will send a link for a mandatory video verification process. The foreign applicant must record a short video holding their original passport and reading a unique code to confirm their identity.

- Download the Certificate: Once approved, the DSC is downloaded onto a secure USB token, which is then used by your legal representative in India to sign the incorporation forms.

Drafting the Memorandum and Articles of Association for Non-Profits

The Memorandum of Association (MoA) and Articles of Association (AoA) for a Section 8 company must explicitly state that all income is applied solely toward the charitable objective and strictly prohibit the payment of dividends to its members. These documents form the constitutional foundation of the non-profit and are scrutinized heavily by the Registrar of Companies during registration.

The MoA must be drafted in the format prescribed by Form INC-13. The Object Clause must clearly define the specific charitable fields such as education, poverty relief, environmental protection, or healthcare.

Sample MoA Non-Profit Clause: "The objects of the company shall be to promote education, healthcare, and social welfare. The company shall apply its profits, if any, or other income in promoting its objects. No portion of the income or property of the company shall be paid or transferred directly or indirectly by way of dividend, bonus, or otherwise to the persons who at any time are or have been members of the company."

Mandatory Compliance With the Foreign Contribution Regulation Act (FCRA)

Any Section 8 company intending to receive foreign donations, grants, or financial contributions must obtain registration or prior permission under the Foreign Contribution Regulation Act. Incorporating the company with foreign directors does not bypass this strict national security and financial regulation governed by the Ministry of Home Affairs.

Newly formed Section 8 companies typically cannot get permanent FCRA registration immediately, as standard registration requires a three-year operational history and a minimum localized spending of ₹15,00,000 on core charitable activities. Instead, new foreign-backed NGOs must apply for "Prior Permission" to receive a specific amount of funding from a specific foreign donor for a defined project. Additionally, all foreign funds must enter India exclusively through a designated FCRA bank account maintained at the State Bank of India (SBI), New Delhi Main Branch.

Tax Exemption Benefits Under Section 12A and 80G

Section 12A exempts the non-profit organization's income from corporate tax, while Section 80G allows Indian taxpayers who donate to the organization to claim tax deductions. These registrations are not automatic and must be proactively applied for through the Income Tax Department after the company is incorporated.

Under the current framework, newly registered Section 8 companies must apply for provisional registration under Section 12A and 80G using Form 10A.

- Provisional Registration: Granted for a period of three years. This allows the newly formed entity to start operations and accept donations with tax benefits immediately.

- Regular Registration: Must be applied for at least six months before the expiry of the provisional registration or within six months of commencing actual charitable activities. Regular registration is valid for five years and requires renewal. Securing 80G status is particularly crucial for local fundraising, as it incentivizes Indian corporations to donate their mandatory Corporate Social Responsibility (CSR) funds to your organization.

Common Misconceptions About Section 8 Companies in India

Many foreign founders mistakenly believe that registering a Section 8 company automatically permits them to accept foreign donations and grants immediate tax-exempt status. Navigating Indian non-profit law requires understanding the distinct separation between corporate existence, tax benefits, and foreign funding laws.

- Myth: Registration guarantees the right to receive foreign funds. Truth: A Section 8 registration only creates the legal entity. Receiving foreign money requires entirely separate, highly regulated approval under the FCRA.

- Myth: Founders can take back remaining assets if the NGO closes. Truth: The assets of a Section 8 company are irrevocably locked into the charitable sector. Upon dissolution, any remaining assets cannot be distributed to founders or members. They must be transferred to another Section 8 company with similar objectives.

- Myth: You need a massive amount of starting capital. Truth: Unlike traditional commercial companies in the past, there is no statutory minimum paid-up capital requirement to start a Section 8 company in India.

Frequently Asked Questions

How long does it take to register a Section 8 company with foreign directors?

The entire process, including document apostillation, DSC procurement, name reservation, and final incorporation filing, typically takes 4 to 6 weeks, assuming all foreign documents are formatted correctly.

Can a Section 8 company pay salaries to its foreign directors?

Yes, a Section 8 company can pay reasonable remuneration to its directors and employees for actual services rendered. However, it cannot distribute profits, dividends, or bonuses based on surplus income.

What is the difference between an NGO Trust and a Section 8 company?

A Section 8 company is governed by the central Companies Act, offering better transparency, easier foreign promoter entry, and higher credibility among international donors compared to a Trust, which is governed by fragmented state-specific laws.

When to Hire a Lawyer

Navigating cross-border charitable regulations, document apostillation, and FCRA compliance requires specialized legal intervention. You should hire a corporate lawyer experienced in Indian non-profit law before you draft your Memorandum of Association or begin the foreign document notarization process. A minor error in the Object Clause or improper formatting of foreign address proofs will result in outright rejection by the Ministry of Corporate Affairs.

Engaging specialized legal counsel in India ensures your constitutional documents align with both corporate laws and future tax-exemption requirements. Furthermore, FCRA applications involve strict scrutiny by the Ministry of Home Affairs, making professional legal representation critical for foreign entities aiming to bring philanthropic funds into the country.

Next Steps

To begin establishing your foreign charitable presence in India, follow these immediate actionable steps. First, finalize your exact charitable objectives and ensure they align with the permitted non-profit activities under the Companies Act 2013. Next, identify your Indian Resident Director, as their presence is a strict legal prerequisite. Once your board is structured, begin the process of notarizing and apostilling the passports and address proofs of all foreign directors in their home countries. Finally, consult with a qualified legal professional to initiate the Digital Signature Certificate applications and reserve your organization's name with the Ministry of Corporate Affairs.