- Strict Documentation Tiers: India mandates a rigorous three-tiered documentation structure, requiring a Local File, Master File, and Country-by-Country (CbC) Report for qualifying multinational enterprises.

- Proactive Dispute Resolution: Utilizing Advance Pricing Agreements (APAs) or Safe Harbour rules provides binding certainty and prevents years of costly litigation with Indian tax authorities.

- Localized Benchmarking is Critical: Global transfer pricing studies are frequently rejected in India; companies must use domestic databases and account for local market conditions to survive a tax audit.

- Heavy Penalties for Non-Compliance: Failing to maintain required documents or report transactions can result in penalties equal to 2% of the international transaction value.

How Does India Apply the Arm's Length Principle?

India requires all cross-border intra-group transactions to be conducted at market value, a standard globally recognized as the arm's length principle. The Indian Income Tax Department strictly enforces this to prevent multinational subsidiaries from artificially shifting profits out of the country to lower-tax jurisdictions.

Governed by the Income Tax Act, 1961, Indian authorities evaluate transactions based on a thorough analysis of Functions performed, Assets employed, and Risks assumed (FAR analysis). If the tax authority determines that your pricing deviates from what independent entities would agree upon, they will make aggressive upward adjustments to your taxable income.

To determine the arm's length price, Indian regulations authorize several specific methods:

- Comparable Uncontrolled Price (CUP) Method: Compares the price charged for property or services in a controlled transaction to an uncontrolled transaction.

- Resale Price Method (RPM): Used primarily for distributors, focusing on the gross margin earned upon reselling products to independent buyers.

- Cost Plus Method (CPM): Applies a market-standard markup to the costs incurred by the supplier of property or services.

- Profit Split Method (PSM): Splits the combined profits of the transaction based on the relative value of each enterprise's contribution.

- Transactional Net Margin Method (TNMM): The most frequently utilized method in India, comparing net profit margins relative to an appropriate base (costs, sales, or assets).

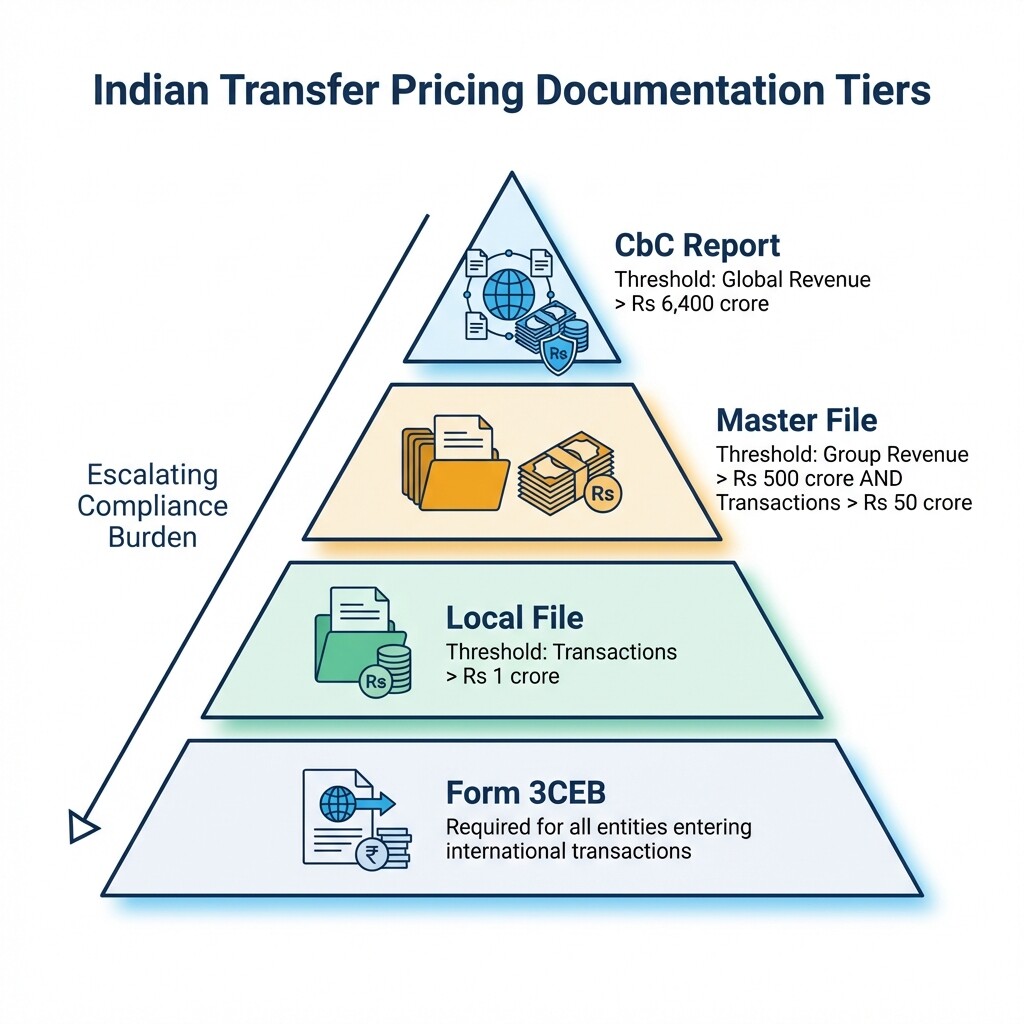

Mandatory Transfer Pricing Documentation Checklist

Multinational entities operating in India must maintain a specific three-tiered documentation structure to justify their transfer pricing policies. Failing to file these forms by the designated statutory deadlines triggers substantial monetary penalties and intense audit scrutiny.

To ensure total compliance under Indian law, multinational subsidiaries must prepare and file the following:

- Accountant's Report (Form 3CEB): Every entity entering into an international transaction must obtain an independent certification from an Indian Chartered Accountant. This form details all intra-group transactions and must be filed electronically by October 31 of the assessment year.

- Local File (Rule 10D Documentation): Contemporaneous documentation supporting the arm's length nature of the transactions. This is mandatory if the aggregate value of international transactions exceeds INR 1 crore (10 million rupees).

- Master File (Form 3CEAA): A high-level overview of the global enterprise's business operations and transfer pricing policies. Filing is triggered if the consolidated group revenue exceeds INR 500 crore and the aggregate value of international transactions exceeds INR 50 crore (or INR 10 crore for intangible properties).

- Country-by-Country (CbC) Report (Form 3CEAD): Applies to large multinational groups with consolidated global revenue exceeding INR 6,400 crore (approximately €750 million) in the preceding accounting year. It provides a breakdown of revenue, taxes paid, and economic activity across all tax jurisdictions.

Comparing Safe Harbour Rules and Advance Pricing Agreements (APAs)

Both Safe Harbour rules and Advance Pricing Agreements (APAs) allow multinational companies to agree on transfer pricing margins with Indian tax authorities before a dispute ever arises. While Safe Harbour provides immediate certainty for routine transactions, APAs offer tailored, long-term protection for complex and high-value business models.

Evaluating which pre-litigation dispute prevention tool fits your corporate structure depends on your risk tolerance, transaction complexity, and timeline.

| Feature | Safe Harbour Rules | Advance Pricing Agreements (APAs) |

|---|---|---|

| Eligibility | Limited to specific routine services (e.g., IT, ITeS, contract R&D, auto components). | Available for all types of international intra-group transactions. |

| Profit Margins | Rigid, statutorily defined profit margins that are non-negotiable. | Highly flexible; negotiated based on your specific FAR analysis and business model. |

| Certainty Period | Applicable for up to 5 consecutive assessment years. | Up to 5 consecutive years, plus a "rollback" option covering 4 prior years. |

| Time to Conclude | Nearly immediate certainty upon filing the application. | A rigorous negotiation process that typically takes 2 to 4 years to conclude. |

| Compliance Cost | Low; requires basic documentation to prove eligibility. | High; requires extensive economic studies, site visits, and legal representation. |

Best Practices for Maintaining Defensible Financial Records

Surviving a transfer pricing audit in India requires contemporaneous documentation that proves your pricing strategy aligns with local market realities. Tax authorities frequently reject global transfer pricing studies that apply broad, regional data without accounting for Indian market conditions.

To build a defensible file that prevents pre-litigation inquiries from escalating into formal tax disputes, implement the following practices:

- Use Domestic Benchmarking: Indian tax officers exhibit a strong bias against foreign comparable data. Utilize recognized Indian financial databases-such as Prowess or Capitaline-to identify local comparable companies.

- Substantiate Intra-Group Services: Management fees and royalty payouts are heavily scrutinized. Maintain an evidence dossier containing emails, meeting minutes, deliverables, and cost-benefit analyses proving that actual services were rendered and that they provided an economic benefit to the Indian subsidiary.

- Document Extraordinary Events: If your Indian subsidiary operates at a loss or lower-than-industry margin due to market downturns, capacity underutilization, or initial setup costs, clearly document the economic rationale. Do not wait for an audit to explain away poor financial performance.

- Align Agreements with Conduct: Ensure that written intercompany contracts exactly match the actual conduct of the parties. If an Indian subsidiary is contractually designated as a "risk-free" captive service provider, it must not bear market or foreign exchange risks in reality.

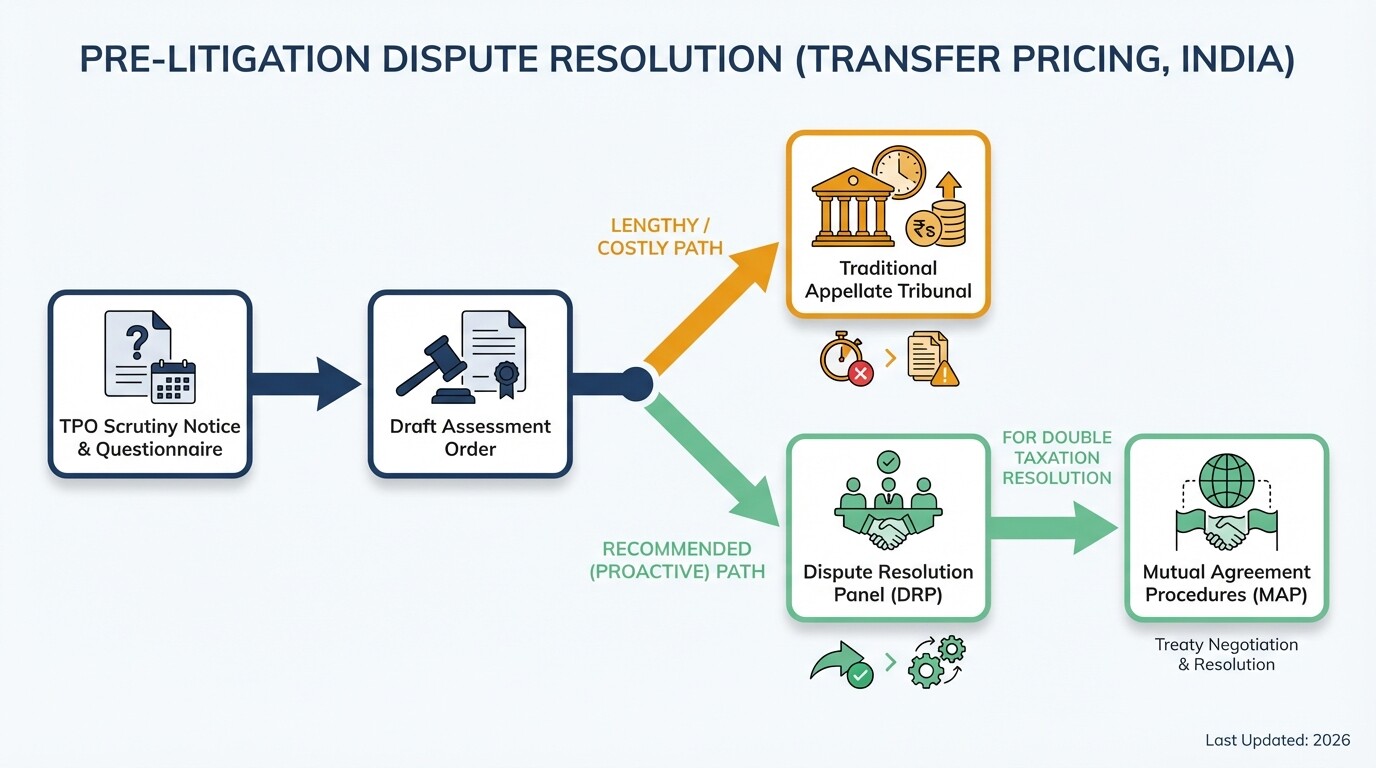

Strategies for Pre-Litigation Dispute Prevention and Handling Tax Notices

Pre-litigation dispute prevention relies on proactive engagement with alternative resolution panels and immediate, structured responses to scrutiny notices. Ignoring early communications or providing incomplete data often forces assessing officers to make arbitrary, aggressive tax adjustments.

When a tax notice is issued, managing the flow of information and selecting the correct appellate channel is critical to resolving the issue efficiently:

- Respond Precisely to Questionnaires: Transfer Pricing Officers (TPOs) typically issue extensive questionnaires. Provide exact, well-indexed responses. Over-sharing irrelevant documents can inadvertently expand the scope of the audit.

- Leverage the Dispute Resolution Panel (DRP): Instead of proceeding through traditional, lengthy appellate tribunals, foreign companies can challenge a draft assessment order before the DRP. This panel of three principal commissioners provides an alternative mechanism to resolve disputes before a final tax demand is issued.

- Initiate Mutual Agreement Procedures (MAP): If an adjustment leads to double taxation, multinational enterprises can invoke MAP under applicable tax treaties. This process shifts the negotiation to the competent authorities of both nations to agree on a fair tax allocation, keeping the company out of domestic court litigation.

Common Misconceptions About Indian Transfer Pricing

Many foreign executives misunderstand the aggressive nature of Indian transfer pricing enforcement, leading to avoidable compliance failures. Relying strictly on headquarters' policies without local adaptation is a primary cause of costly tax litigation.

- Global transfer pricing policies work automatically in India: A Master File drafted in the US or EU is not sufficient for Indian compliance. Indian regulations demand localized FAR analysis and domestic comparables to validate the arm's length price.

- Only highly profitable subsidiaries are audited: Tax authorities heavily target entities showing consistent losses or marginal profits. A captive service center operating at a loss in India will almost certainly trigger scrutiny, as the assumption is that profits are being improperly shifted abroad.

- Domestic transactions are entirely exempt: Transfer pricing provisions also apply to Specified Domestic Transactions (SDTs) between related resident entities if they enjoy a tax holiday and the transaction volume exceeds INR 20 crore.

FAQ

What is the penalty for not filing Form 3CEB in India?

Failing to furnish the accountant's report (Form 3CEB) attracts a flat penalty of INR 100,000. Additionally, failing to maintain transfer pricing documentation or report a transaction can result in a penalty equal to 2% of the value of the international transaction.

Can we apply an Advance Pricing Agreement (APA) retroactively?

Yes. India's APA program includes a rollback provision. You can apply the agreed transfer pricing methodology to four prior assessment years, providing retrospective tax certainty alongside the prospective five-year agreement.

What are the most heavily scrutinized intra-group transactions in India?

The Indian Revenue heavily scrutinizes royalty payouts, brand fees, intra-group management service charges, and the profit margins of captive software development and IT-enabled service (ITeS) centers.

When to Hire a Lawyer

Transfer pricing in India involves a complex intersection of corporate finance, tax law, and international treaties. You should consult a lawyer immediately if you receive a scrutiny notice from a Transfer Pricing Officer, or if you are considering filing for an Advance Pricing Agreement or Mutual Agreement Procedure. Early legal intervention is vital to structure your responses and prevent the dispute from escalating into a formal tax demand.

To ensure your multinational operations remain compliant and protected, browse dispute prevention and pre-litigation lawyers in India on Lawzana.

Next Steps

- Audit Your Supply Chain: Map out all existing cross-border transactions involving your Indian subsidiary to ensure every interaction is covered by an intercompany agreement.

- Review Benchmarking Data: Check if your current transfer pricing study relies on regional data. Commission an update using Indian databases to reflect local comparables.

- Assess Pre-Litigation Options: If your transactions are high-value or complex, schedule an advisory session with a tax lawyer to evaluate the cost-benefit of initiating an Advance Pricing Agreement (APA).