- Malaysia offers a preferential corporate tax rate of 5% or 10% for companies qualifying under the Global Services Hub (GSH) incentive scheme.

- Eligibility requires a minimum annual operating expenditure of MYR 500,000 and the creation of high-value local jobs.

- The Malaysian Investment Development Authority (MIDA) is the primary gateway for all regional hub applications and approvals.

- Intellectual Property (IP) transferred to a Malaysian hub must comply with international "substance" requirements to qualify for tax exemptions.

- Labuan IBFC remains a viable alternative for firms seeking a mid-shore jurisdiction with a flat 3% tax rate on audited profits.

Global Services Hub Setup Checklist

Global firms must meet specific threshold requirements to qualify for the 2024-2027 tax incentives. This checklist outlines the mandatory operational milestones for a successful application with MIDA.

| Category | Requirement for New Companies | Requirement for Existing Companies |

|---|---|---|

| Corporate Tax Rate | 5% or 10% for up to 10 years | 10% on incremental income for 5 years |

| Minimum Annual Spend | MYR 500,000 | MYR 500,000 |

| High Value Jobs | Min. 5 (Min salary MYR 5,000) | Maintain existing + 20% increase |

| C-Suite/Key Positions | At least 1 (Min salary MYR 10,000) | At least 1 (Min salary MYR 10,000) |

| Local Internship | Minimum 2 per year | Minimum 2 per year |

| ESG Reporting | Mandatory annual contribution | Mandatory annual contribution |

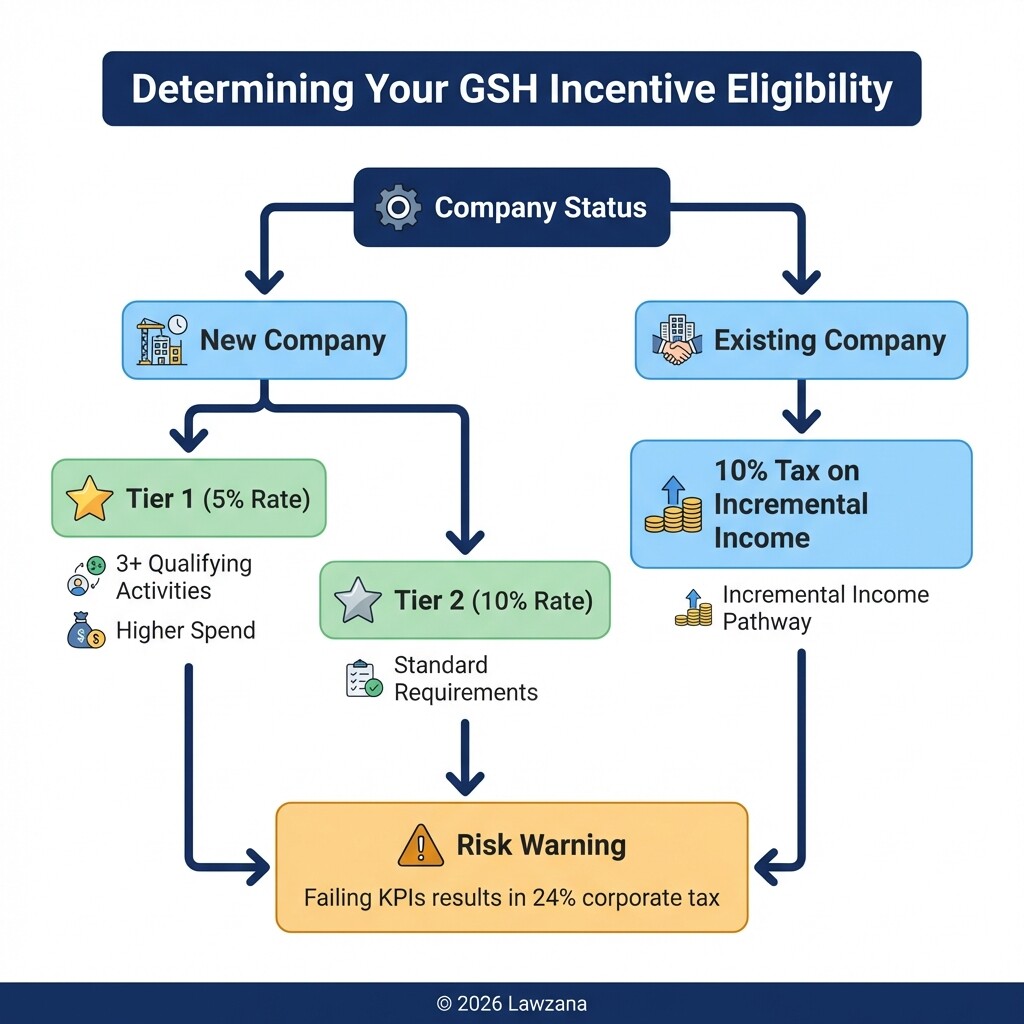

Eligibility for the 5-10% Preferential Corporate Tax Rate

The Global Services Hub (GSH) incentive provides a reduced corporate tax rate of 5% or 10% for a period of five to ten years. This incentive is designed for multinational companies that use Malaysia as a base for regional or global decision-making, trading, and support services.

To qualify for the 5% tier, companies generally must demonstrate higher levels of business spending and employment than the 10% tier. Specifically, the hub must perform at least three qualifying activities, which often include regional distribution, central procurement, or technical support services. The "outcome-based" approach means that the tax benefit is tied directly to your firm's ability to meet annual Key Performance Indicators (KPIs) regarding local economic contribution.

Common Mistake: Failing to Meet Local Headcount and Spending Requirements

The most frequent error global firms make is treating the regional hub as a "brass plate" office without sufficient operational substance. Malaysian tax authorities, specifically the Inland Revenue Board (LHDN), strictly enforce minimum local employment and annual operating expenditure (OPEX) thresholds.

If a company falls short of its hiring quotas or fails to spend the committed MYR 500,000 annually within the Malaysian economy, the tax incentive may be revoked retroactively. This results in the company being taxed at the standard corporate rate of 24%. Firms must maintain rigorous documentation of payroll, local vendor contracts, and utility bills to prove that the hub is a legitimate center of economic activity rather than a shell for profit shifting.

Legal Steps for Transferring International IP to a Malaysian Hub

Transferring Intellectual Property (IP) to a Malaysian hub requires a formal legal assignment and a valuation that complies with transfer pricing guidelines. Malaysia follows the "nexus approach," meaning that tax benefits are only granted to IP income if the underlying Research and Development (R&D) was actually performed or managed by the Malaysian entity.

- Valuation and Assignment: Conduct an independent valuation of the IP and draft an Assignment Agreement to transfer ownership from the parent company to the Malaysian subsidiary.

- Stamp Duty Adjudication: Submit the transfer documents to the LHDN for stamp duty adjudication. While some incentives provide exemptions, standard transfers may incur nominal fees.

- Registration with MyIPO: File the trademark, patent, or industrial design with the Intellectual Property Corporation of Malaysia (MyIPO) to ensure local legal protection.

- Transfer Pricing Documentation: Prepare a contemporaneous transfer pricing report to prove that the royalty rates or buy-in payments between the parent and the hub are at "arm's length" (market value).

Alternative Locations: Labuan International Business and Financial Centre

Labuan IBFC serves as a "mid-shore" alternative to mainland Malaysia, offering a simplified tax regime for international trading and non-trading activities. It is particularly attractive for firms focused on offshore banking, insurance, and wealth management that do not require a physical presence in major cities like Kuala Lumpur.

While mainland Malaysia offers the GSH incentive at 5-10%, Labuan provides a flat tax rate of 3% on audited profits for trading entities, provided they meet specific substance requirements (local employees and local spending). However, Labuan entities are generally restricted from dealing extensively in the Malaysian Ringgit or providing services directly to mainland residents without specific approvals.

| Feature | Mainland Malaysia (GSH) | Labuan IBFC |

|---|---|---|

| Tax Rate | 5% or 10% (Incentive based) | 3% on audited profits |

| Currency | Malaysian Ringgit (MYR) | Multi-currency (USD, EUR, etc.) |

| Target Audience | Regional operations, Manufacturing | Finance, Leasing, Holding companies |

| Regulator | MIDA / LHDN | Labuan FSA |

Step-by-Step Setup Guide with MIDA

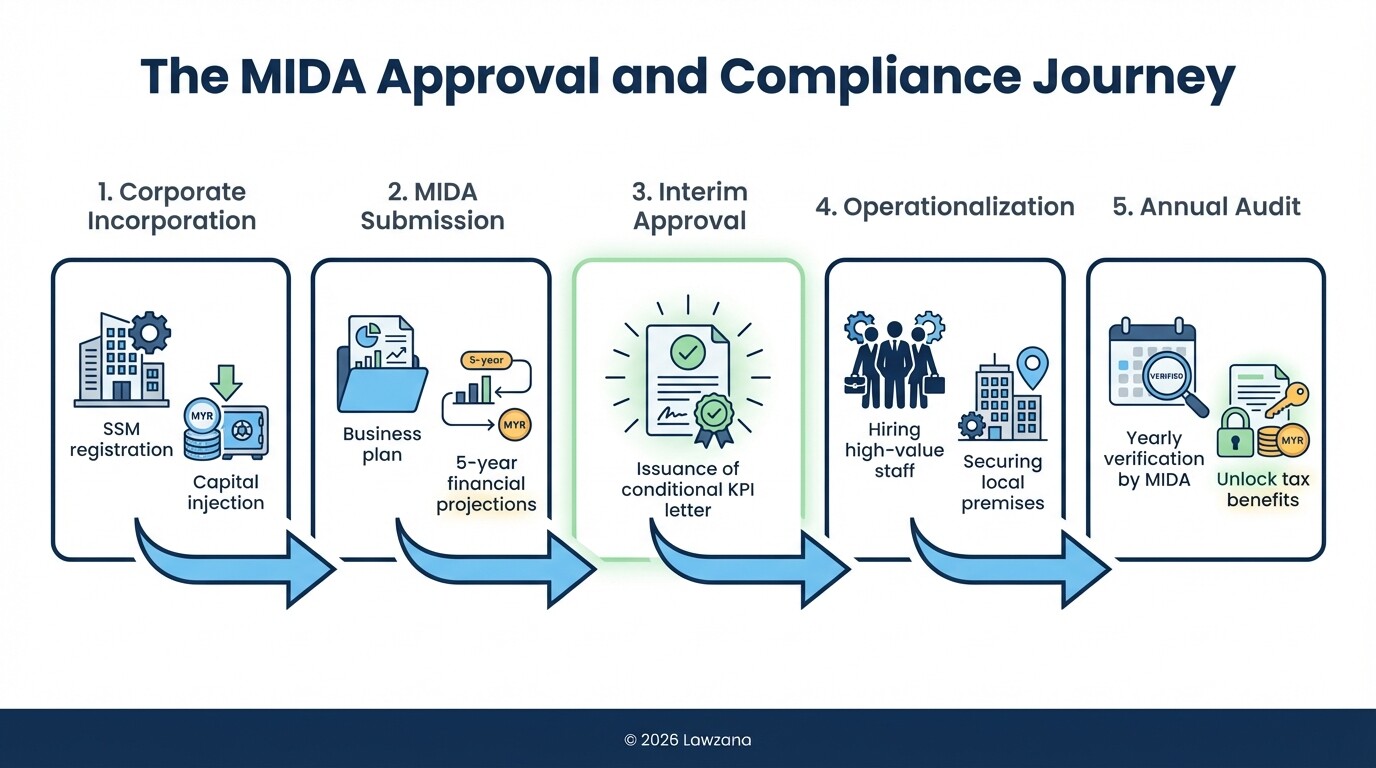

Setting up a regional hub involves a dual process of corporate incorporation and incentive application through the Malaysian Investment Development Authority (MIDA).

Step 1: Corporate Incorporation

Before applying for incentives, you must incorporate a private limited company (Sdn Bhd) via the Companies Commission of Malaysia (SSM). This entity should have a minimum paid-up capital that reflects its operational scale, often starting at MYR 500,000 to MYR 1 million for regional hubs.

Step 2: MIDA Consultation and Submission

Submit a formal application for the Global Services Hub incentive through the MIDA Invest Malaysia portal. This submission must include a detailed five-year business plan, financial projections, and a human resources plan detailing the specific high-value roles you intend to create.

Step 3: Evaluation and Interim Approval

MIDA will evaluate the application based on the "outcome-based" criteria. If successful, you will receive an "Interim Approval Letter" which outlines the specific conditions (KPIs) your firm must meet to enjoy the tax rate.

Step 4: Operationalizing the Hub

Finalize office leases, hire the required headcount, and begin operations. You must ensure that the "Center of Regional Management" is established, meaning senior decision-makers must be physically based in Malaysia.

Step 5: Annual Compliance Audit

To claim the 5% or 10% rate on your tax return, you must obtain an annual verification letter from MIDA. This letter confirms that you have met the hiring and spending requirements for that year.

FAQ

What counts as "High Value Jobs" in Malaysia?

High-value jobs are defined as roles requiring professional qualifications or technical expertise, with a minimum monthly salary of MYR 5,000. For regional hubs, at least 10% of the staff should be in "Key Positions" with salaries exceeding MYR 10,000.

Can existing Malaysian companies apply for the Global Services Hub incentive?

Yes, existing companies can apply, but the tax incentive (typically 10%) will only apply to "incremental income"-the profit generated above their average income from the previous three years.

How long does the MIDA approval process take?

The evaluation process generally takes 4 to 8 weeks from the date of complete submission, provided all supporting documents and the business plan meet MIDA's requirements.

Is there a minimum investment requirement?

There is no fixed "investment" amount for the GSH incentive, but you must prove a minimum annual operating expenditure of MYR 500,000. This includes salaries, rent, and local services.

When to Hire a Lawyer

Navigating the transition of a global firm to Malaysia involves complex intersections of tax law, immigration, and intellectual property. You should consult a legal professional if:

- You are transferring high-value IP and need to ensure compliance with the "nexus approach" to avoid double taxation.

- Your hub structure involves complex inter-company service agreements that require transfer pricing defense.

- You need to draft executive employment contracts that comply with the Malaysian Employment Act while meeting MIDA's salary thresholds.

- You are deciding between a Mainland (GSH) structure and a Labuan IBFC structure.

Next Steps

- Feasibility Study: Calculate your projected annual OPEX and headcount to determine if you meet the 5% or 10% tax tier thresholds.

- Draft a Business Plan: Prepare a five-year roadmap focusing on "qualifying activities" such as regional distribution or central procurement.

- Engage with MIDA: Schedule a pre-submission consultation with the Business Services Division at MIDA to vet your eligibility.

- Secure Local Premises: Identify a physical office location, as a registered office address is required for the application.