Dutch BV Formation for EU Import Logistics and VAT Deferment

Key Takeaways

Establishing a Dutch Besloten Vennootschap (BV) is highly effective for non-EU companies seeking to manage European supply chains. The Netherlands serves as Europe's premier logistics hub, offering distinct corporate and tax advantages for international trade.

- A Dutch BV requires minimal share capital but must be incorporated through a civil law notary.

- Securing an Article 23 license allows companies to defer 21% import VAT, drastically improving cash flow.

- You must register for an EORI number through Dutch customs before importing commercial goods.

- Strict Ultimate Beneficial Owner (UBO) compliance requires transparency of all individuals holding over 25% ownership.

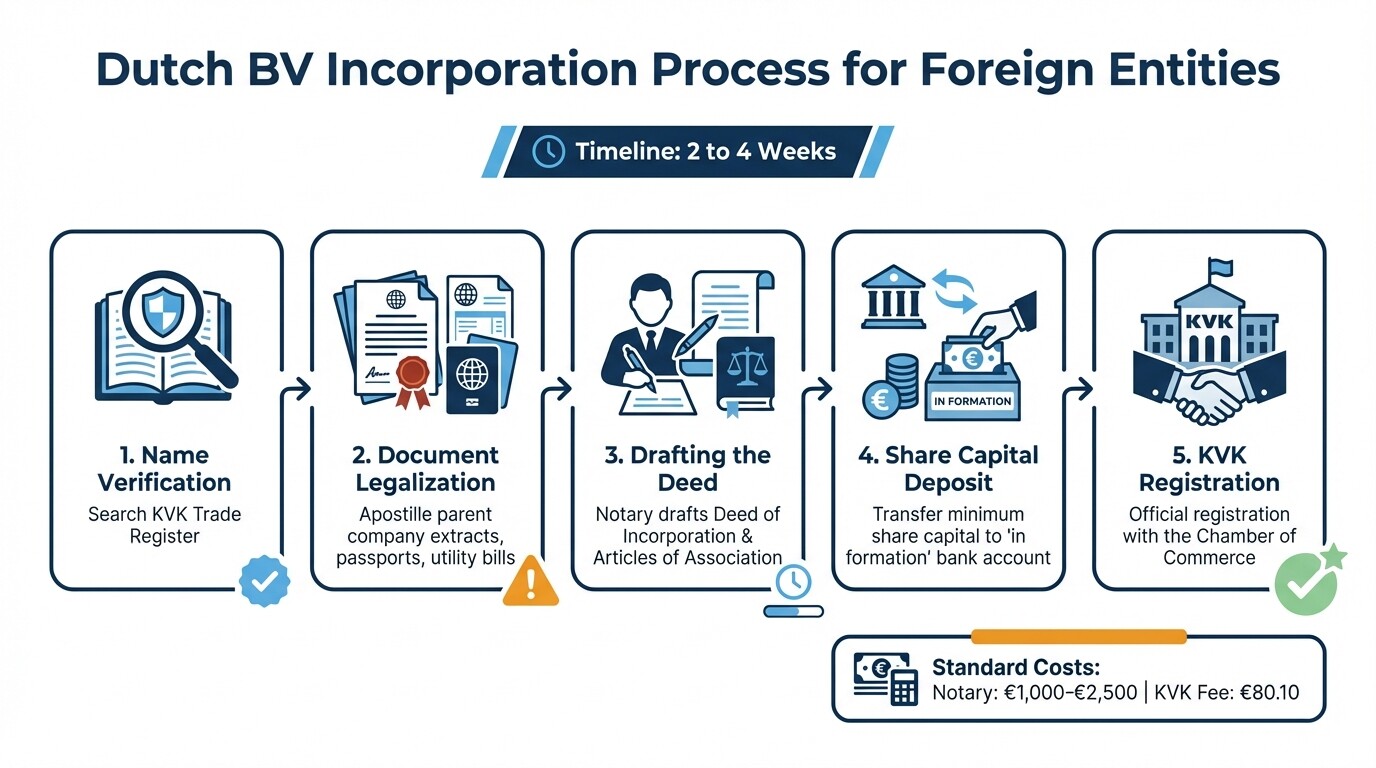

BV Incorporation Checklist for Foreign Corporate Shareholders

Incorporating a Dutch BV as a foreign entity requires a civil law notary, corporate document legalization, and registration with the Dutch Chamber of Commerce (KVK). The standard timeline from document submission to active registration is two to four weeks.

To complete the incorporation, foreign corporate shareholders must follow these exact steps:

- Name Verification: Verify the proposed company name availability in the KVK Trade Register.

- Document Legalization: Obtain an apostilled or legalized extract from the foreign parent company's local corporate registry, alongside legalized passports and utility bills for all foreign directors.

- Drafting the Deed: Engage a Dutch civil law notary to draft the Deed of Incorporation and Articles of Association in Dutch, with a sworn English translation provided for your records.

- Share Capital Deposit: Transfer the required share capital to an "in formation" bank account. The minimum statutory share capital is just €0.01, though €100 to €1,000 is standard practice.

- KVK Registration: The notary registers the fully formed BV with the Dutch Chamber of Commerce.

Standard incorporation costs include notary fees ranging from €1,000 to €2,500 depending on corporate structure complexity, plus a one-time KVK registration fee of €80.10.

Applying for a Dutch EORI Number

An Economic Operators Registration and Identification (EORI) number is legally required to import commercial goods into the European Union. You must apply for this unique identifier through the Dutch Customs Administration after your BV is successfully registered with the KVK.

Your Dutch EORI number acts as your customs tracking ID across all 27 EU member states. Because the Netherlands links the EORI directly to your Dutch tax identification number, the application process is streamlined. Application is free of charge and generally processes within three to five business days. Goods cannot clear customs at the Port of Rotterdam or Schiphol Airport without this active number.

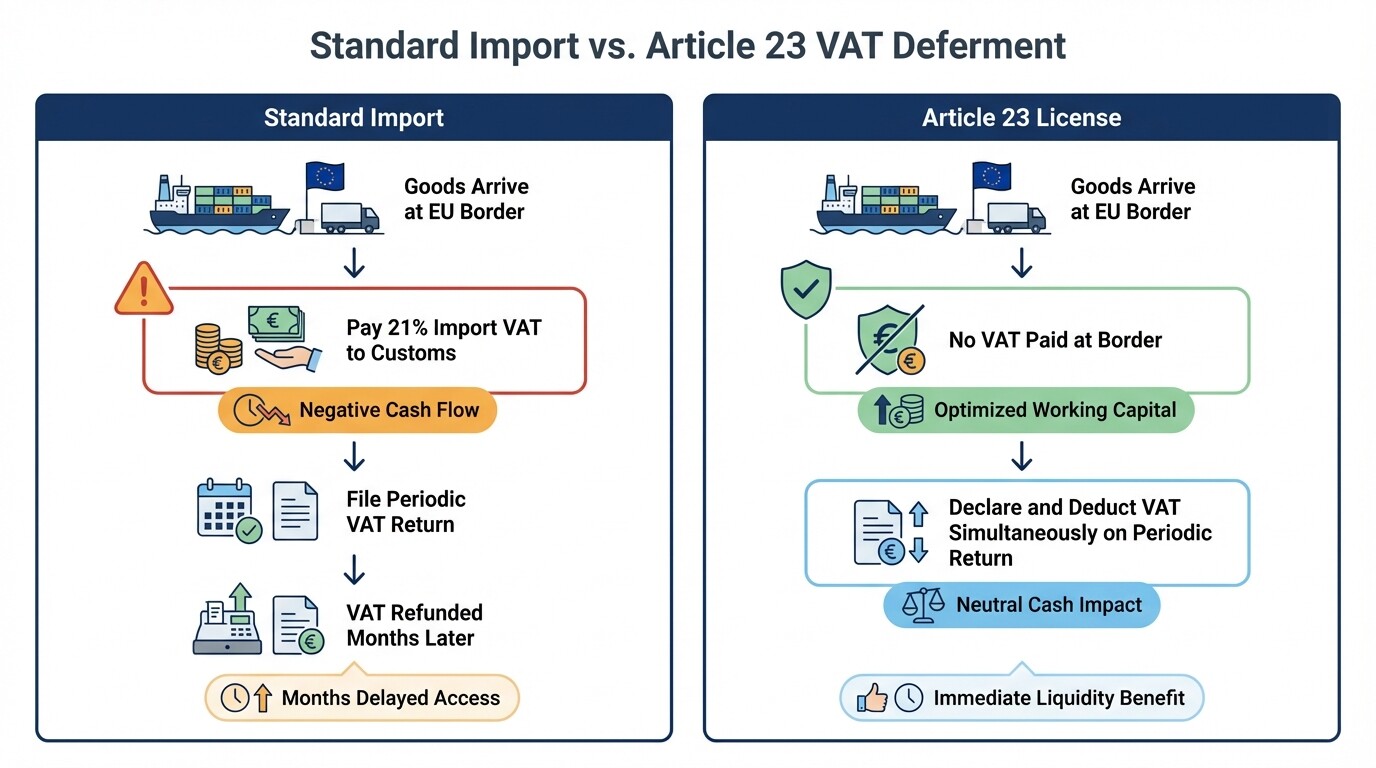

How to Secure an Article 23 License for VAT Deferment

An Article 23 license allows businesses to defer import VAT from the moment of customs clearance to their periodic VAT return. This eliminates the need to pre-finance the standard 21% Dutch import VAT at the border, freeing up substantial working capital.

To secure an Article 23 VAT deferment license, your Dutch BV must meet specific criteria set by the Dutch Tax and Customs Administration.

- You must be registered for VAT in the Netherlands.

- You must regularly import goods from non-EU countries.

- You must maintain accurate, transparent bookkeeping records detailing your import and export activities.

If your foreign parent company operates without a physical BV presence but uses a Dutch logistics provider, you can still access Article 23 benefits by appointing a fiscal representative. This representative assumes joint liability for your VAT obligations while facilitating the deferment on your behalf.

Compliance with UBO Registry Requirements

The Ultimate Beneficial Owner (UBO) register mandates that all natural persons holding more than 25% of economic interest or voting rights in the BV must be formally recorded. Non-compliance results in severe economic sanctions, fines, or criminal prosecution under Dutch anti-money laundering regulations.

When a foreign corporate shareholder owns the Dutch BV, you must trace the ownership chain all the way up to the human individuals at the top of the corporate structure. The civil law notary will require organizational charts, corporate registers, and certified identification documents to verify these owners. The BV must register its UBOs with the KVK within eight days of incorporation.

Distribution and Agency Agreements Under EU Trade Law

Commercial agreements in the European Union heavily regulate the relationship between suppliers and local distributors, often favoring the commercial agent. If your Dutch BV engages local agents to sell your imported goods, contracts must explicitly define jurisdiction, termination indemnities, and exclusivity parameters to avoid costly severance disputes under the Dutch Civil Code.

Sample Exclusivity and Territory Clause

Below is standard foundational language for defining territory in a commercial distribution agreement governed by Dutch law.

"The Principal hereby appoints the Distributor as its exclusive distributor for the sale of the Products within the territory of the Netherlands, Belgium, and Luxembourg (the 'Territory'). The Distributor shall not actively market, advertise, or establish any branch to sell the Products outside of the Territory. However, the Distributor may fulfill unsolicited orders (passive sales) from customers located outside the Territory, provided such sales comply with prevailing European Union competition law restrictions."

Common Misconceptions About Dutch Import Logistics

Many foreign businesses misunderstand the operational and legal footprint required to benefit from Dutch trade incentives. Recognizing these errors early prevents shipment delays and tax penalties.

- A BV automatically grants an Article 23 license: Simply forming a BV does not automatically trigger VAT deferment. You must submit a separate, formal application to the tax authorities proving your import frequency and reliable bookkeeping.

- A virtual office is sufficient for tax residency: The Dutch tax authorities require "economic substance." Using a purely virtual address without actual management activity in the Netherlands can lead to a denial of VAT registration and corporate tax benefits.

- EU law applies identically in every member state: While customs tariffs are uniform across the EU, VAT rules, corporate governance, and employment laws vary significantly by country. The Dutch Article 23 system is unique to the Netherlands and does not apply if goods clear customs in Germany or France.

Frequently Asked Questions

Can a non-EU resident be the sole director of a Dutch BV?

Yes. There are no nationality or residency requirements for the director of a Dutch BV. However, having only non-resident directors may complicate local bank account opening and require additional proof of Dutch economic substance for tax purposes.

How long does it take to get an Article 23 license?

Once your Dutch BV is incorporated and VAT registered, processing the Article 23 license application generally takes four to six weeks. You should account for this timeline before scheduling your first major ocean or air freight shipment.

Do I need to lease a physical warehouse in the Netherlands?

No. Many foreign-owned Dutch BVs operate successfully by partnering with third-party logistics providers (3PLs) who manage warehousing and fulfillment. You do not need to own or lease real estate to maintain a BV, provided your registered address meets legal substance requirements.

When to Hire a Lawyer for International Trade Setup

Structuring a cross-border logistics hub requires careful corporate and tax planning. You should hire an attorney when you are ready to incorporate the entity, need to structure complex parent-subsidiary relationships, or require tailored commercial contracts for European distributors. A qualified professional ensures your entity architecture prevents double taxation and complies with strict European customs regulations.

You can find experienced international trade law lawyers in the Netherlands to guide you through the incorporation and regulatory approval process.

Next Steps

Launching your European logistics hub requires coordinating with a Dutch notary, a tax advisor, and a logistics partner. Follow a phased approach to ensure full legal compliance before your cargo arrives at the border.

- Gather and notarize all corporate documents from your foreign parent company.

- Engage a Dutch civil law notary to draft and execute the Deed of Incorporation.

- Register your newly formed BV for Dutch VAT and apply immediately for an EORI number.

- Submit your application for an Article 23 license either directly or through your appointed customs broker.