Key Takeaways

Declaring personal bankruptcy in South Africa (voluntary sequestration) affects expatriates differently because of strict visa requirements and the existence of international assets.

- Proof of benefit: You must prove to the High Court that selling your assets financially benefits your creditors.

- Upfront costs: Filing for sequestration requires paying administrative and legal fees, typically between R20,000 and R40,000.

- Alternatives: Debt review and administration orders protect your assets and restructure your payments without declaring bankruptcy.

- Visa risks: Civil judgments for unpaid debt can hurt your ability to renew your visa.

- Global assets: South African law requires you to disclose all of your worldwide assets.

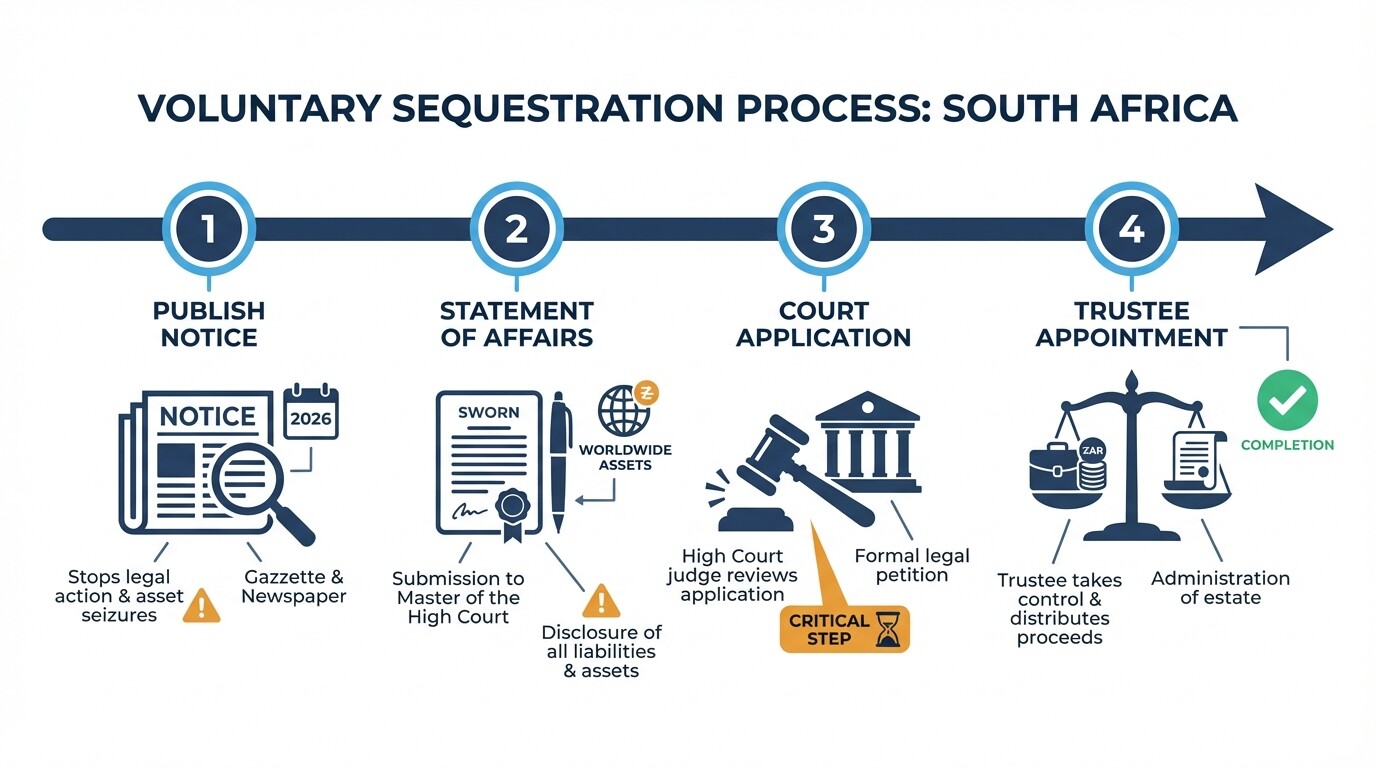

The Threshold and Process for Voluntary Sequestration

Voluntary sequestration in South Africa is the legal process of surrendering your estate to the Master of the High Court. To apply, you must prove your liabilities exceed your assets. You must also have enough cash to cover the administrative costs and show that sequestration pays your creditors a minimum dividend (usually 10 to 20 cents on the Rand). If your estate has no assets or funds to distribute, the High Court will reject your application.

The sequestration process follows these mandatory steps:

- Publish notice: Your attorney publishes a formal notice in the Government Gazette and a local newspaper. This stops creditors from continuing legal action or seizing assets.

- Statement of affairs: You submit a sworn statement of your worldwide assets, liabilities, and creditors to the Master of the High Court.

- Court application: A High Court judge reviews the application and grants a sequestration order if legal thresholds are met.

- Trustee appointment: A trustee takes control of your estate, sells your non-exempt assets, and distributes the proceeds to your creditors.

Estimated Costs for Personal Insolvency

Filing for personal bankruptcy in South Africa costs between R20,000 and R40,000 based on the complexity of your estate. The High Court requires you to prove you have liquid assets or cash to cover these fees upfront. Because the process involves High Court litigation, you must hire an attorney.

You should budget for these specific fees:

- Legal fees: R15,000 to R25,000 for attorneys and advocates to draft the application and represent you in court.

- Advertising: R1,500 to R3,000 to publish legal notices.

- Appraiser fees: R2,000 to R4,000 for a sworn appraiser to value physical assets like vehicles or property.

- Trustee fees: Deducted directly from the sale of your assets. The trustee takes a statutory percentage of the funds recovered for creditors.

Debt Solutions Comparison

Expatriates should evaluate statutory debt relief programs like debt review and administration orders before choosing sequestration. These programs legally restructure your payments, protect your assets from seizure, and help you avoid the restrictions of bankruptcy.

South Africa provides consumer protection mechanisms to help individuals manage debt. The most common alternative for expats is Debt Counselling (Debt Review), governed by the National Credit Act. The South African Government provides official guidance on debt counselling.

| Feature | Debt Review (Counselling) | Administration Order | Voluntary Sequestration |

|---|---|---|---|

| Ideal user | Expats with regular income and high unsecured debt. | Individuals with low debt and low income. | Severe insolvency where debt far exceeds assets. |

| Debt limit | None. | Maximum R50,000. | Must have enough debt to justify court costs. |

| Asset protection | High. | High. | Low (non-exempt assets sold). |

| Duration | 3 to 5 years. | Varies based on payment size. | Up to 10 years before automatic rehabilitation. |

| Legal status | You retain full control over finances. | Finances managed by an administrator. | You lose control of your estate and cannot serve as a company director. |

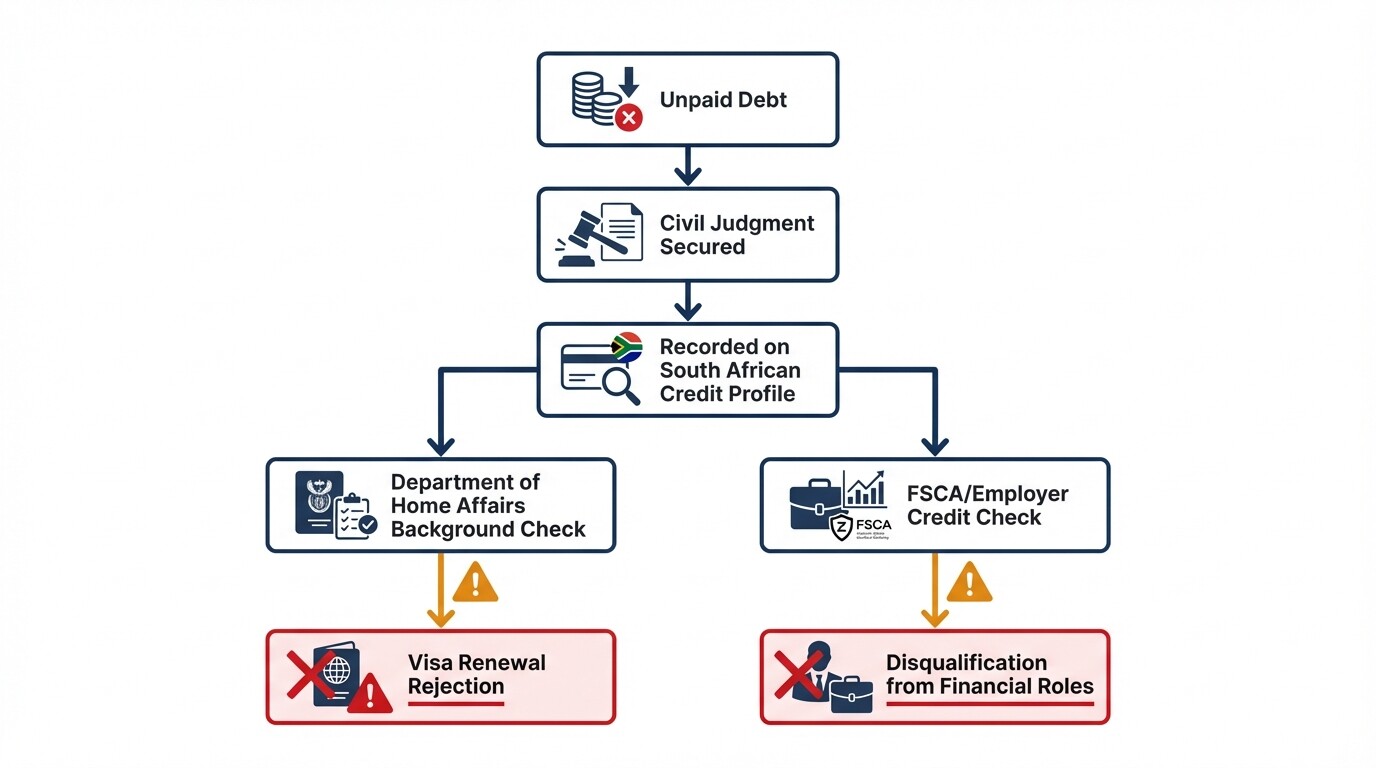

How Credit Judgments Impact Expatriate Visas

Unpaid debts and credit judgments can prevent you from renewing a South African work visa or securing new employment. Civil judgments appear on background checks and can violate the "good and sound character" requirements of the Department of Home Affairs.

If a creditor secures a civil judgment against you for unpaid debt, it is recorded on your South African credit profile. This creates specific hurdles for expats.

Visa applications for permanent residency, business visas, and financially independent visas require proof of good financial standing. Judgments can trigger requests for additional documentation or cause outright rejections. Working in the financial sector requires meeting strict "fitness and propriety" standards set by the Financial Sector Conduct Authority (FSCA). A civil judgment disqualifies you from many of these roles, and major corporate employers routinely conduct credit checks before extending job offers.

Cross-Border Assets and Common Misconceptions

Expatriates often misunderstand how South African insolvency law affects their home-country finances and residency status.

- Leaving the country: Fleeing South Africa does not erase your debt. Creditors can secure default judgments in your absence. These remain valid for 30 years and complicate any return to the country.

- Foreign bank accounts: South African creditors cannot directly seize foreign accounts without applying to a court in your home country. This cross-border litigation is expensive and typically reserved for massive commercial debts.

- Overseas property: You must disclose all worldwide assets and liabilities when applying for voluntary sequestration in South Africa. Hiding foreign real estate or investments is a criminal offense under the Insolvency Act.

- Home credit score: A South African sequestration order does not automatically appear on foreign credit reports. Credit bureaus operate strictly within national borders. However, international banks operating in both countries may internally flag your global accounts.

- Immigration status: Entering a statutory debt review program does not negatively affect your immigration status. It protects you from the civil judgments that actually cause visa issues.

- Instant debt relief: Sequestration does not immediately clear your record. You remain an "insolvent" person with financial restrictions until you apply to the High Court for formal legal rehabilitation, which takes between one and ten years.

When to Hire a Lawyer

You need a South African insolvency attorney if you plan to petition the High Court for voluntary sequestration. Consult legal counsel if creditors have issued a summons or if your visa status is at risk due to impending judgments.

A qualified lawyer can negotiate with creditors, halt asset seizures, and advise you on debt review versus sequestration. You can find restructuring and insolvency lawyers in South Africa to evaluate your situation and protect your rights.

Next Steps for Expats in Financial Distress

Taking direct action is the best way to protect your assets and immigration status in South Africa. Ignoring creditors accelerates legal action and limits your debt relief options.

- Pull your credit report: Obtain a free credit report from South African bureaus like TransUnion or Experian to see exactly who you owe and if any judgments have been filed.

- Gather documentation: Collect loan agreements, credit card statements, payslips, and a list of your monthly living expenses.

- Consult a professional: Reach out to a registered debt counselor or insolvency attorney to discuss restructuring options before defaulting on major payments.

- Stop borrowing: Do not use credit cards or take out personal loans to pay off existing debt. This can disqualify you from legal protections under the National Credit Act.