- Shipping B2B goods to the UK requires a valid GB EORI number and a full digital declaration through the Customs Declaration Service (CDS).

- Overseas sellers must register for UK VAT immediately. The standard domestic registration threshold does not apply to foreign businesses.

- You must classify goods using the 10-digit UK commodity code to calculate tariffs and claim reduced rates under free trade agreements.

- Manage disputed customs holds by clearly defining shipping liabilities through standardized Incoterms in your contracts.

- Importing animal, plant, and food products requires advance notification and certified health documentation under the UK Border Target Operating Model.

What customs declaration documents do I need to ship B2B goods to the UK?

Shipping B2B goods into the UK requires a full digital import declaration via the Customs Declaration Service (CDS), a commercial invoice, and a packing list. Depending on your products, you may also need specific export health certificates or proof of origin documents. Border authorities expect precise data that matches your physical cargo.

Your standard import documentation must include:

- GB EORI Number: An Economic Operators Registration and Identification number starting with "GB" is mandatory for all businesses importing goods into England, Wales, or Scotland. Apply directly through the official UK government EORI registration portal.

- Commercial Invoice: Detail the buyer and seller identities, exact goods description, value in GBP (£), currency used, and agreed Incoterms.

- Packing List: Detail the shipment weight, dimensions, packaging type, and outer box marks or numbers.

- Customs Declaration (CDS): The single customs document is entirely digital. Your freight forwarder or customs broker submits this data into the CDS before goods arrive at a UK port.

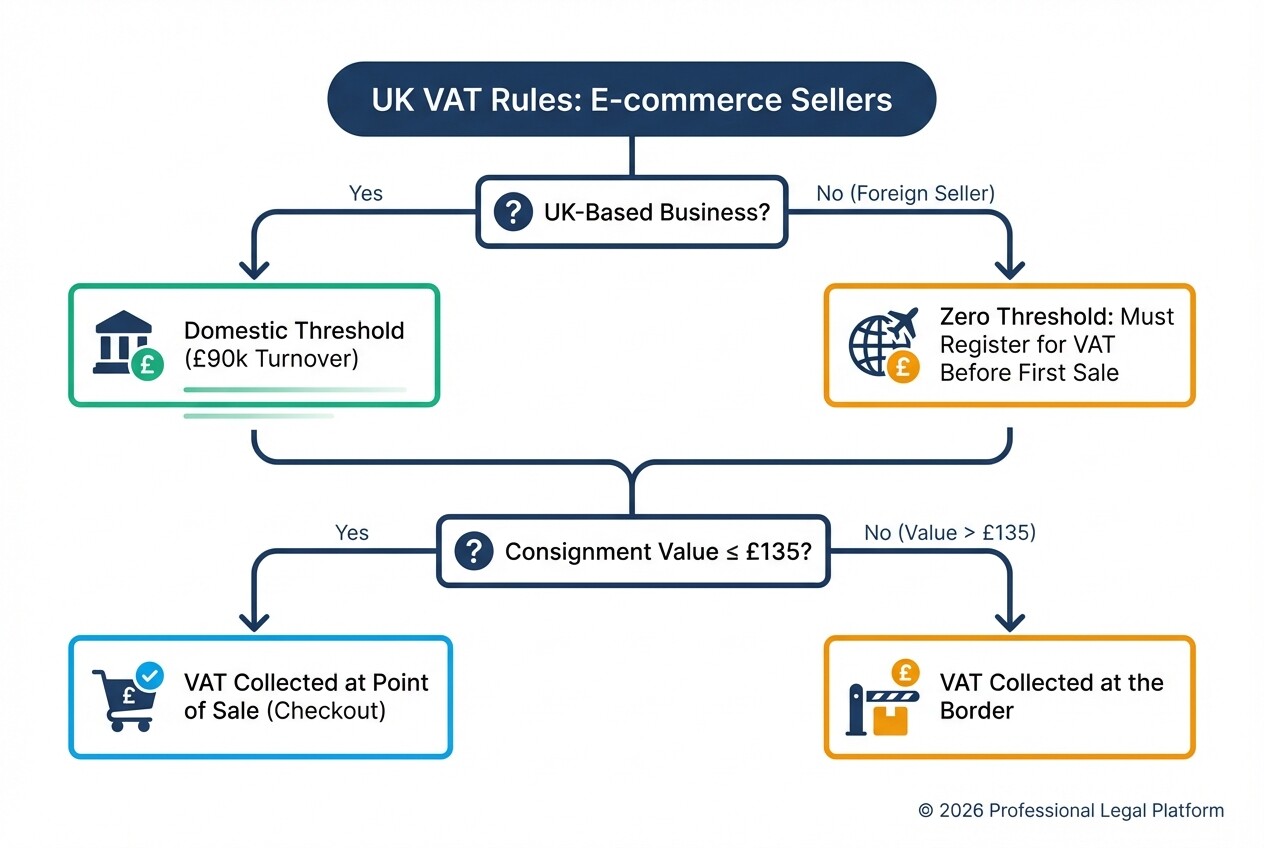

What VAT mistakes do foreign e-commerce sellers make in the UK?

Foreign e-commerce sellers frequently fail to register for UK Value Added Tax (VAT) before their first sale. They often incorrectly assume the domestic registration threshold applies to them. This mistake leads to border seizures, financial penalties from HM Revenue and Customs (HMRC), and blocked supply chains. The UK tax system treats non-established taxable persons differently than local companies.

- Ignoring the zero threshold rule: UK-based businesses only register for VAT when taxable turnover exceeds £90,000. Foreign businesses have no threshold. They must register for VAT before making a single taxable sale in the UK.

- Misunderstanding the £135 threshold: For B2C and B2B consignments valued at £135 or less, VAT collection shifts from the border to the point of sale. Sellers often fail to collect this at checkout, causing unexpected tax bills for the buyer and damaged customer relationships.

- Using an EU VAT number: A European Union VAT number holds no legal weight in the UK. You must obtain a dedicated UK VAT registration number from HMRC to import and sell goods.

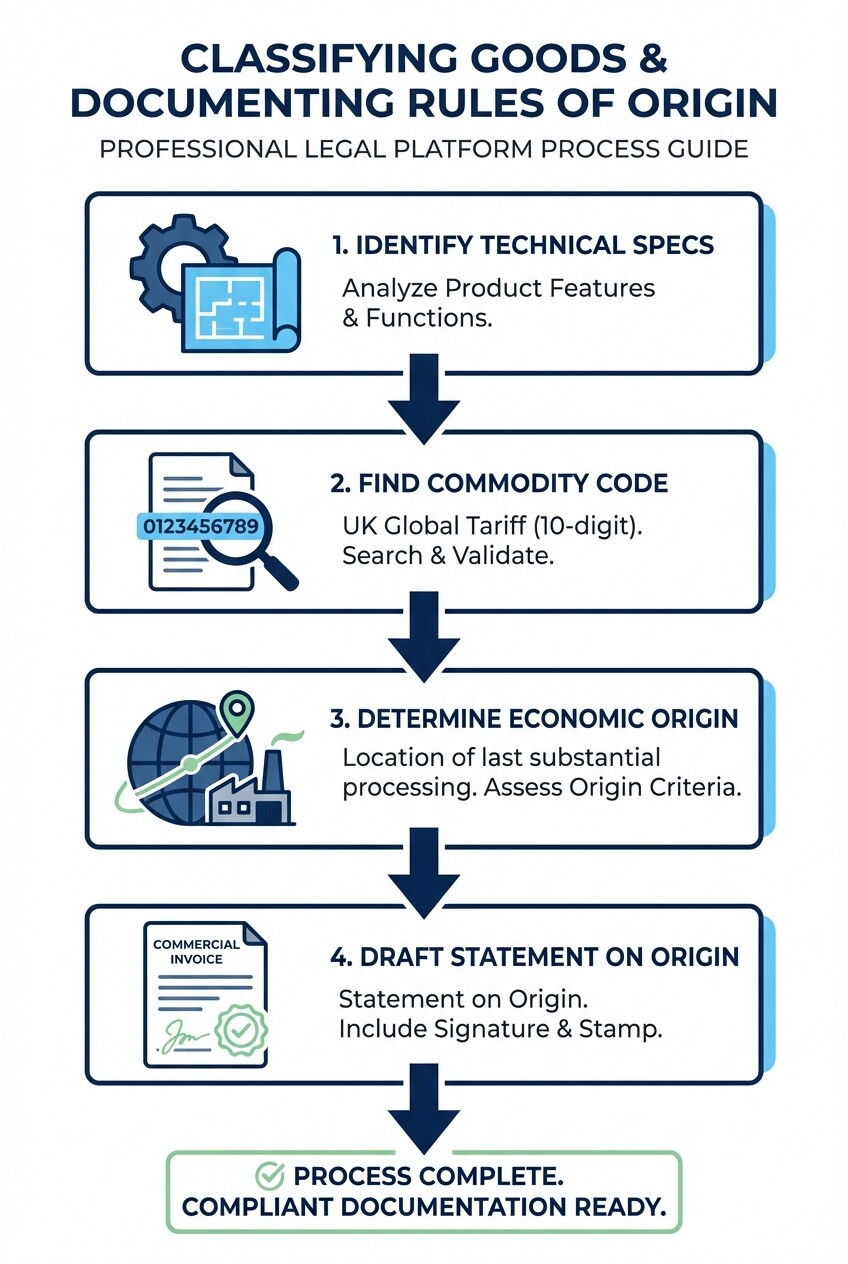

How do I classify goods and document rules of origin?

Classifying goods requires matching your product to the 10-digit commodity code in the UK Global Tariff schedule. Documenting rules of origin involves proving where the product was manufactured to claim preferential tariff rates under UK trade agreements. Incorrect classification causes import delays and unexpected tax liabilities.

- Identify technical specifications: Gather the exact materials, function, and manufacturing methods of your product.

- Search the UK Global Tariff: Use the official UK Trade Tariff tool to find the correct 10-digit commodity code. This code determines your duty rate and flags any import restrictions.

- Determine economic origin: The origin is where the goods were wholly obtained or underwent their last substantial, economically justified processing. Shipping from a country does not automatically make it the country of origin.

- Draft the statement on origin: To claim preferential tariffs, the exporter must provide a formal text statement on the commercial invoice declaring the originating status of the goods.

How can I resolve disputes from UK customs holds?

Resolving disputes from UK customs holds requires rapid communication with your freight forwarder and fast submission of missing documents through the CDS. You must review contracts to determine who bears the risk of delay. Clear Incoterms defend against financial losses. Storage fees (demurrage) accumulate quickly when goods sit at the border.

| Dispute Scenario | Recommended Action | Preventative Strategy |

|---|---|---|

| Missing valuation data | Provide the commercial invoice directly to the National Clearance Hub. | Automate invoice generation to include standardized customs values. |

| Unpaid duty or VAT | Instruct your customs broker to use your duty deferment account immediately. | Maintain sufficient funds in your HMRC Cash Account linked to the CDS. |

| Damaged goods during hold | File a claim against the carrier or warehouse operator. | Use appropriate Incoterms and secure marine cargo insurance. |

If border holds lead to contract breaches with buyers, consulting international trade law lawyers in the United Kingdom helps you enforce your rights and recover capital.

What are the most common UK import misconceptions?

International sellers often assume standard global shipping documents satisfy UK border requirements. The UK enforces specific rules separated entirely from European Union customs procedures. Relying on outdated assumptions leads to non-compliance penalties.

- Freight forwarders absorb liability: Even if a broker files your paperwork, the importer of record remains legally and financially responsible for the accuracy of all declarations, duties, and taxes.

- Low-value shipments are exempt: Every commercial shipment entering the UK requires a formal customs declaration, regardless of monetary value.

- CE marking is permanently accepted: The UK extended the recognition of CE marking for many goods, but specific sectors face deadlines where the UKCA (UK Conformity Assessed) mark becomes mandatory.

What SPS documentation do I need for food and plant imports?

The UK Border Target Operating Model requires strict Sanitary and Phytosanitary (SPS) documentation for animal, plant, and food products. You must pre-notify UK authorities and provide standardized health certificates to prevent the destruction of goods at the border.

- Required certificates: You need an Export Health Certificate for animal products or a Phytosanitary Certificate for plants. A competent regulatory authority in the exporting country must issue and sign these documents before shipment.

- Pre-notification: Importers must submit advance notification through the Import of products, animals, food and feed system (IPAFFS). Complete this at least one full working day before the consignment arrives at the UK point of entry.

- Incomplete documentation consequences: If certificates contain errors or are missing, authorities detain the shipment at a UK Border Control Post. They can legally return the goods to the origin country or destroy them at your expense.

When should I hire an international trade lawyer?

Hire an international trade lawyer when facing an HMRC customs audit, negotiating complex B2B supply agreements, or dealing with seized shipments. Legal counsel ensures your logistics contracts protect you from liability and align with UK trade statutes.

A lawyer can draft terms and conditions that designate the buyer as the importer of record. This transfers the burden of UK import duties and VAT directly to the customer. Legal representation is also necessary if you need to appeal a tariff classification decision made by UK border authorities.

Next Steps for UK E-commerce Importers

Prevent costly disruptions at the border by auditing your customs data, product classifications, and logistics contracts.

- Apply for a GB EORI number if you do not already possess one.

- Register for UK VAT as a non-established taxable person before finalizing UK-bound sales.

- Audit your product catalog to ensure every item has a verified 10-digit UK commodity code.

- Review your shipping contracts to confirm your Incoterms accurately reflect your risk and tax liabilities.