- Registering as a Non-Resident Importer simplifies logistics and checkout for Canadian buyers.

- Accurate tariff classification under the Harmonized System prevents border delays and monetary penalties.

- E-commerce sellers with over CAD 30,000 in global sales across four calendar quarters must collect and remit Canadian sales tax.

- You must retain detailed import records for six years to pass Canada Border Services Agency (CBSA) compliance audits.

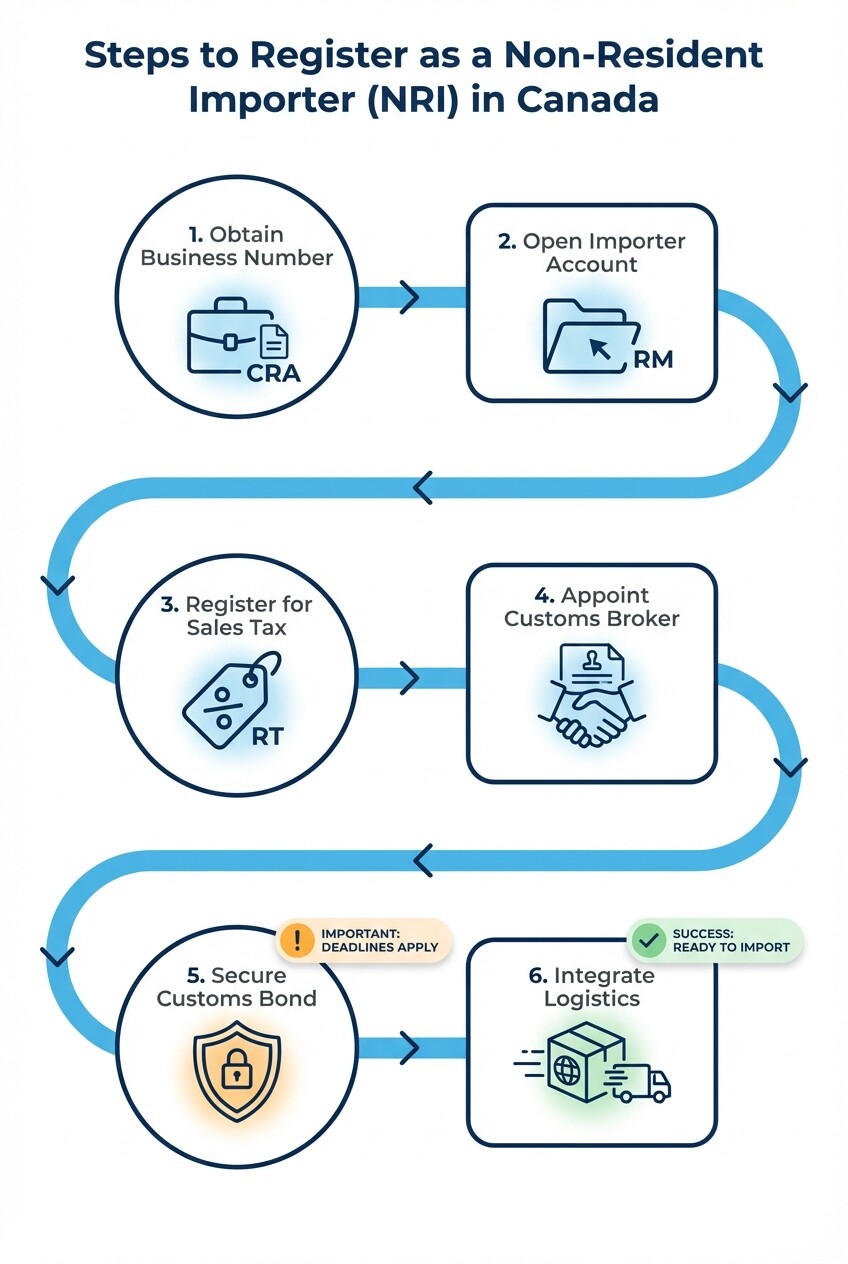

Registering as a Non-Resident Importer (NRI)

A Non-Resident Importer (NRI) program allows foreign companies to act as the legal importer of record in Canada. Your business clears customs and pays duties and taxes directly instead of passing the bill to the buyer upon delivery.

- Obtain a Business Number: Apply for a nine-digit Canadian Business Number from the Canada Revenue Agency.

- Open an Importer Account: Register for an RM account, an importer and exporter identifier linked to your Business Number.

- Register for Sales Tax: Open an RT account to collect and remit Goods and Services Tax and Harmonized Sales Tax on Canadian sales.

- Appoint a Customs Broker: Sign a General Agency Agreement authorizing a licensed Canadian customs broker to file declarations on your behalf.

- Secure a Customs Bond: Obtain a surety bond to secure the release of goods before duty and tax payments are processed.

- Integrate Logistics: Set up your e-commerce platform and shipping partners to route commercial goods under your NRI account number.

Core CBSA Documentation Requirements

The Canada Border Services Agency (CBSA) requires specific documentation to clear commercial goods. Missing forms flag shipments for secondary inspection. This causes delivery delays and storage fees.

- Canada Customs Invoice: Commercial shipments valued at CAD 3,300 or more need a formal Canada Customs Invoice or a commercial invoice with equivalent data.

- Cargo Control Document: Transportation companies use a manifest or bill of lading to report the physical movement of goods to the CBSA.

- Certificates of Origin: Sellers claiming preferential tariff treatment under trade agreements like the Canada-United States-Mexico Agreement must provide valid origin certifications.

- Permits and Licenses: Products regulated by departments like Health Canada or the Canadian Food Inspection Agency need import permits before reaching the border.

Determining Tariff Classifications

Every item imported into Canada requires a 10-digit code under the Canadian Customs Tariff, which integrates the international Harmonized System (HS). This code dictates the duty rate and identifies import restrictions.

- Global Standard: The first six digits are standard across all countries using the Harmonized System.

- Canadian Specifics: The final four digits are unique to Canada. They determine domestic duty rates and track statistical data.

- Penalty Risks: Misclassification results in retroactive duty assessments and shipment seizures, alongside administrative monetary penalties.

- Advance Rulings: You can apply for a National Customs Ruling from the CBSA to guarantee classification status before shipping complex items.

Remitting GST/HST on E-commerce Goods

Canada imposes a 5 percent federal Goods and Services Tax (GST). In several provinces, this blends into a Harmonized Sales Tax (HST) of up to 15 percent. Foreign e-commerce sellers must collect this tax at checkout and remit it to the government if they meet the revenue threshold.

- Revenue Threshold: The registration threshold is CAD 30,000 in worldwide taxable sales across four consecutive calendar quarters.

- Duty-Paid Value: Canadian import taxes are calculated based on the duty-paid value. The tax applies to the product value plus any customs duties.

- Platform Rules: Non-resident digital marketplaces and fulfillment warehouses must manage tax collections if third-party sellers do not register independently.

Misconceptions About Canadian Import Laws

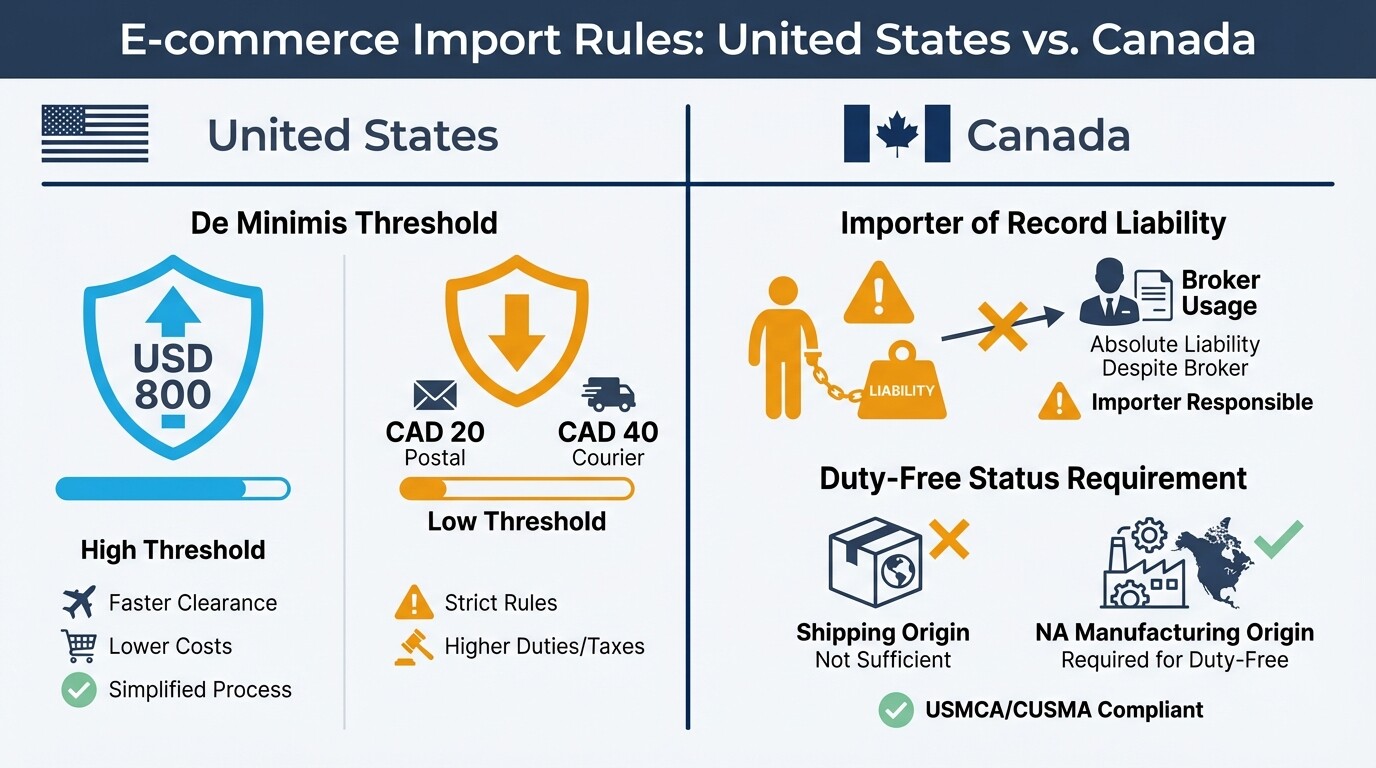

Many international e-commerce sellers assume Canadian trade regulations mirror United States law. This leads to compliance violations and border rejections.

- De Minimis Thresholds: The United States allows duty-free entry for shipments up to USD 800. Canada maintains a strict de minimis threshold of CAD 20 for postal shipments and CAD 40 for courier shipments.

- Broker Liability: A licensed customs broker files your import paperwork, but the importer of record bears total legal and financial liability for errors.

- Shipping Origin vs. Manufacturing Origin: Goods shipped from an American warehouse do not automatically qualify for duty-free status. They must be manufactured or significantly transformed in North America to qualify under the trade agreement.

Preparing for Customs Compliance Audits

The CBSA conducts trade compliance verifications to verify tariff classifications, product valuation, and country of origin. Failing these audits triggers retroactive duty charges going back up to four years, plus penalty interest.

- Maintain Detailed Records: Canadian law requires importers to retain all commercial invoices, accounting records, and shipping documents for six years following the importation year.

- Self-Audit Regularly: Check product catalog classifications periodically to ensure codes align with Customs Tariff updates.

- Document Procedures: Create compliance manuals detailing internal processes for managing import data and communicating with customs brokers.

- Utilize Voluntary Disclosures: If you find a reporting error before the CBSA initiates an audit, submit an adjustment request. This may waive monetary penalties.

When to Hire an International Trade Lawyer

International trade law is technical, and administrative mistakes carry heavy financial penalties. An international trade lawyer in Canada can structure your market entry and establish a Non-Resident Importer program safely. Legal representation is also necessary if you face a CBSA compliance verification audit, appeal a penalty, or seek advance customs rulings.

Next Steps for E-commerce Sellers

Launching e-commerce operations in Canada requires adherence to federal regulations. Evaluate your current and projected sales volume against the CAD 30,000 tax registration threshold. Secure a Canadian Business Number and contact licensed customs brokers who handle high-volume e-commerce shipments. Finally, review your product catalog to confirm Harmonized System classifications before your first shipment reaches the border.