How to Navigate CFIUS Review Timelines for Foreign M&A in the United States

- Choosing between a 30-day declaration and a 45-day formal notice dictates your transaction timeline, filing fees, and legal certainty.

- Investments in US businesses involving critical technology, infrastructure, or data (TID) trigger mandatory filing requirements that carry steep penalties if ignored.

- Failing to allocate time for the informal 15-day pre-filing consultation is a frequent scheduling error that delays deal closures.

- Securing safe harbor through a voluntary notice prevents the government from unwinding a completed merger post-closing.

- Mitigation agreements allow high-risk deals to proceed but introduce long-term compliance costs that must be factored into the acquisition's valuation.

Comparing the 45-Day Review vs. 30-Day Declaration Process

The 30-day declaration is a streamlined process for lower-risk transactions, while the 45-day notice is a comprehensive audit for complex or sensitive cross-border deals. Choosing the correct filing path requires balancing your transaction's risk profile against your desired closing date.

Declarations are short-form filings that do not require a filing fee. If the Committee on Foreign Investment in the United States (CFIUS) clears a declaration, the parties receive safe harbor. However, CFIUS often concludes declarations without a definitive clearance, forcing parties to file a standard notice anyway. The formal notice takes 45 days for the initial review but provides a much higher certainty of a definitive answer, though it requires a filing fee based on the transaction value.

| Feature | 30-Day Declaration | 45-Day Formal Notice |

|---|---|---|

| Best For | Low-risk buyers from allied nations | Complex deals, state-backed buyers, TID targets |

| Initial Timeline | 30 calendar days | 45 calendar days |

| Potential Extension | None (Clear, reject, or request notice) | Additional 45-day investigation phase |

| Filing Fee | None | Tiered (Up to $300,000 for large deals) |

| Outcome Certainty | Low to Moderate | High (Ends in clearance, mitigation, or block) |

How to Determine Mandatory Filing Triggers for Tech Acquisitions

Mandatory filings are legally required if a foreign entity acquires a controlling or covered non-passive interest in a US business that deals with critical technologies, infrastructure, or sensitive personal data. Navigating the current regulatory landscape requires auditing the target company's assets before signing a definitive agreement.

Under the Foreign Investment Risk Review Modernization Act (FIRRMA) and its implementing regulations, you must file at least 30 days prior to closing if your target falls into the "TID" category.

- Critical Technology: The target produces, designs, or tests technologies subject to US export controls. If exporting the technology to the buyer's home country requires a specific regulatory license, filing is mandatory.

- Critical Infrastructure: The target owns, operates, or supplies equipment to specific sub-sectors of US infrastructure, such as telecommunications networks, power grids, or public water systems.

- Sensitive Personal Data: The target maintains or collects sensitive data (like biometric, financial, or health records) on more than one million US citizens, or tailors products to US military personnel.

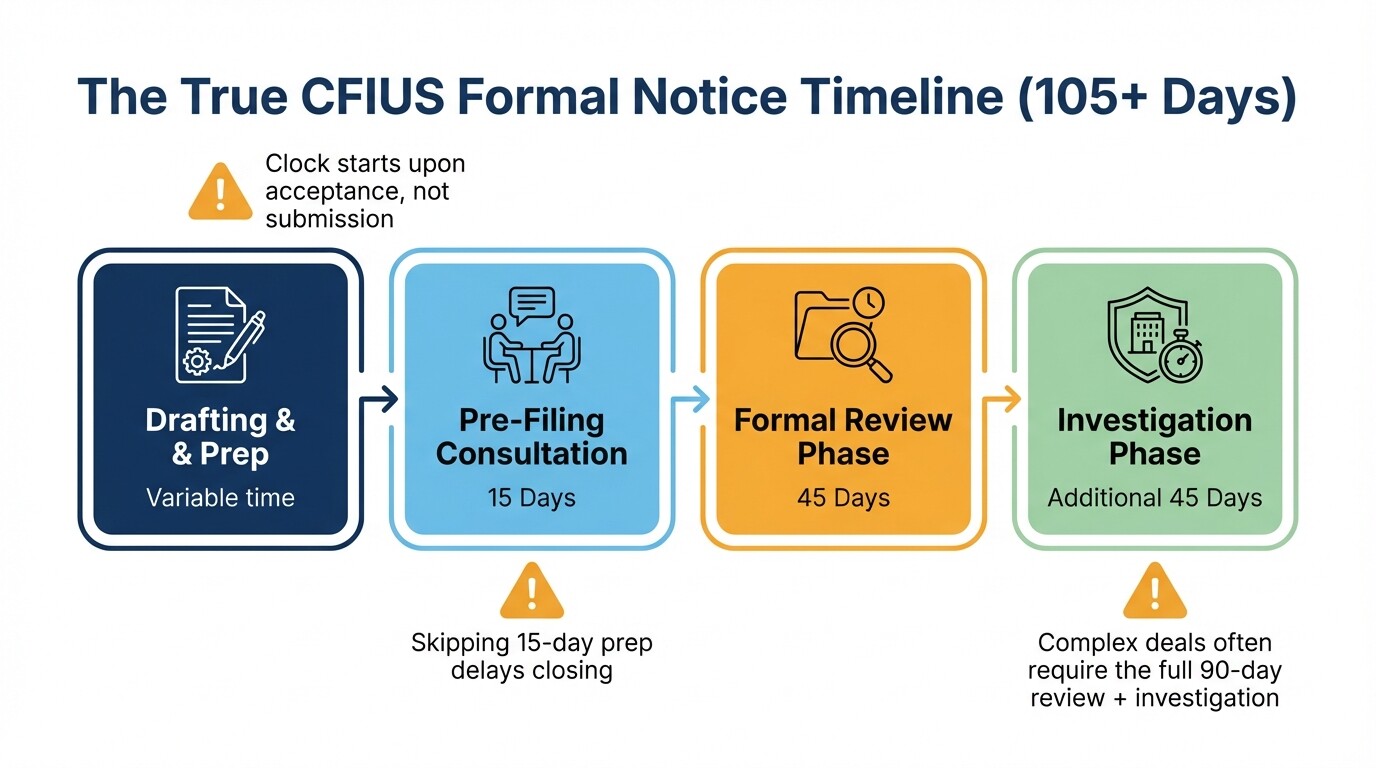

Common CFIUS Timeline Misconceptions

Dealmakers often miscalculate regulatory timelines by assuming government processes fit neatly into statutory windows. These missteps can derail acquisition financing, expire letters of credit, and disrupt integration plans.

- Ignoring the 15-day pre-filing consultation: The 45-day clock does not start the day you finish drafting your notice. The statutory timeline only begins after CFIUS accepts the formal filing. Submitting a draft notice for a customary 15-day pre-filing consultation is critical; skipping or miscalculating this step is a leading cause of delayed closings.

- Assuming "voluntary" means "unnecessary": Many buyers assume that if a deal does not trigger a mandatory filing, they should bypass CFIUS entirely. If a non-notified transaction presents a national security risk, CFIUS retains the authority to investigate and force the unwinding of the deal years after closing.

- Underestimating the investigation phase: Buyers often plan for the 45-day review but fail to account for the subsequent 45-day investigation phase. If CFIUS identifies potential risks or needs more time, they will roll the review into an investigation, stretching the total timeline to 90 days or more.

Step-by-Step Guide to Preparing a Voluntary Notice

Filing a voluntary notice protects your transaction from being challenged post-closing by securing a legal safe harbor. Preparing this comprehensive filing requires gathering extensive corporate, financial, and personal data about the foreign acquirer and the US target.

- Conduct a Security Threat Assessment: Evaluate the foreign buyer's ultimate beneficial ownership, government ties, and historical operations in sanctioned countries.

- Draft the Notice: Compile the required information, including detailed transaction mechanics, the strategic rationale for the acquisition, and the target's US market share. You must also gather personal identifiers (CVs, passports) for all foreign directors and officers.

- Submit the Draft Pre-Filing: Send the draft notice to CFIUS. Expect a 15-day review period where the committee will ask initial questions and request clarifications before officially accepting the filing.

- Pay the Filing Fee: Wire the appropriate filing fee based on the tiered transaction value system. The Department of the Treasury will not begin the 45-day review clock until the payment clears.

- Manage the Q&A Period: During the 45-day review, CFIUS will send follow-up questions. The deal team must respond rapidly, usually within 2 to 3 business days, to prevent the committee from rejecting the notice for lack of cooperation.

Evaluating Mitigation Agreements vs. Blocked Transactions

When CFIUS identifies a national security risk, they will either propose a mitigation agreement to neutralize the threat or recommend the President block the transaction. Buyers must weigh the long-term operational costs of mitigation against the total financial loss of an abandoned deal.

Mitigation agreements are legally binding contracts between the deal parties and the US government. While they allow the transaction to close, they heavily restrict how the foreign buyer can operate the US business. Common mitigation terms include requiring US citizens to hold specific board seats, forcing the divestiture of sensitive business units, or mandating independent third-party compliance audits. These agreements add permanent overhead costs and limit access to the target's intellectual property, which can undermine the original financial rationale for the acquisition.

If parties refuse mitigation, or if the risk is deemed unmitigable, CFIUS will recommend blocking the deal. If the transaction has already closed, the government will order divestment. This results in wasted legal fees, broken deal expenses, and severe reputational damage. Consulting with specialized merger and acquisition lawyers in the United States is crucial to negotiate favorable mitigation terms before a deal collapses.

Frequently Asked Questions

Who has the final authority to block a transaction under CFIUS?

The President of the United States holds the sole authority to formally block or unwind a transaction. However, deals rarely reach the President's desk; most parties choose to abandon the transaction voluntarily if CFIUS signals it will recommend a block.

How much are CFIUS filing fees?

Filing fees apply only to formal notices, not declarations. The fees are tiered based on the total value of the transaction, ranging from $0 for deals under $500,000, up to $300,000 for transactions valued at $750 million or more.

Can CFIUS review a deal after it has already closed?

Yes. If the parties do not file a notice and receive safe harbor, CFIUS has the authority to review the transaction indefinitely. If they discover a national security threat years later, they can force the foreign buyer to divest the US business.

When to Hire a Lawyer

Cross-border transactions require specialized legal counsel early in the letter of intent (LOI) stage. You should engage an M&A attorney well versed in foreign investment regulations before conducting deep due diligence. Do not wait until the purchase agreement is drafted to assess regulatory exposure. Legal counsel is necessary to draft CFIUS-specific conditions precedent in your deal documents, allocate regulatory risk, and manage the extensive data collection required for government filings.

Next Steps

- Audit Target Operations: Request the target's export control classifications, government contracts, and data collection policies immediately upon opening the data room.

- Allocate Risk in the LOI: Include specific clauses in your term sheet detailing which party bears the cost of filing fees and what happens to the deal if mitigation is required.

- Build the Timeline: Map your target closing date backward, adding at least 110 days to account for drafting, pre-filing consultation, formal review, and potential investigation phases.