- Stock acquisitions close faster than asset purchases but transfer all historical corporate liabilities to the foreign buyer.

- Asset purchases let buyers select specific assets and leave behind unknown liabilities. The process requires complex transfers of individual contracts and property.

- Regulatory reviews from the Committee on Foreign Investment in the United States (CFIUS) and antitrust authorities add two to six months to transactions.

- Joint ventures allow foreign entities to enter the US market before committing to a full acquisition.

- Tax structuring and fund repatriation depend on bilateral tax treaties between the United States and the buyer's home jurisdiction.

M&A Timeline Comparison: Asset vs. Stock Purchases

The choice between an asset purchase and a stock acquisition determines the pace of the transaction. Stock acquisitions typically close within three to six months because the corporate entity transfers as a single unit. Asset purchases take five to nine months. The delay comes from the administrative work of transferring individual assets, business licenses, and employee contracts.

| Phase | Stock Acquisition | Asset Purchase | Delay Factors |

|---|---|---|---|

| Preparation | 2 to 4 weeks | 2 to 4 weeks | Negotiating valuation and deal structure. |

| Due Diligence | 4 to 8 weeks | 6 to 12 weeks | Asset titles, anti-assignment clauses, environmental reviews. |

| Drafting | 4 to 6 weeks | 6 to 10 weeks | Individual assignment agreements for assets and real estate. |

| Regulatory | 4 to 24 weeks | 4 to 24 weeks | CFIUS reviews and antitrust waiting periods. |

| Closing | 1 to 2 weeks | 2 to 4 weeks | Transitioning payroll, benefits, and physical assets. |

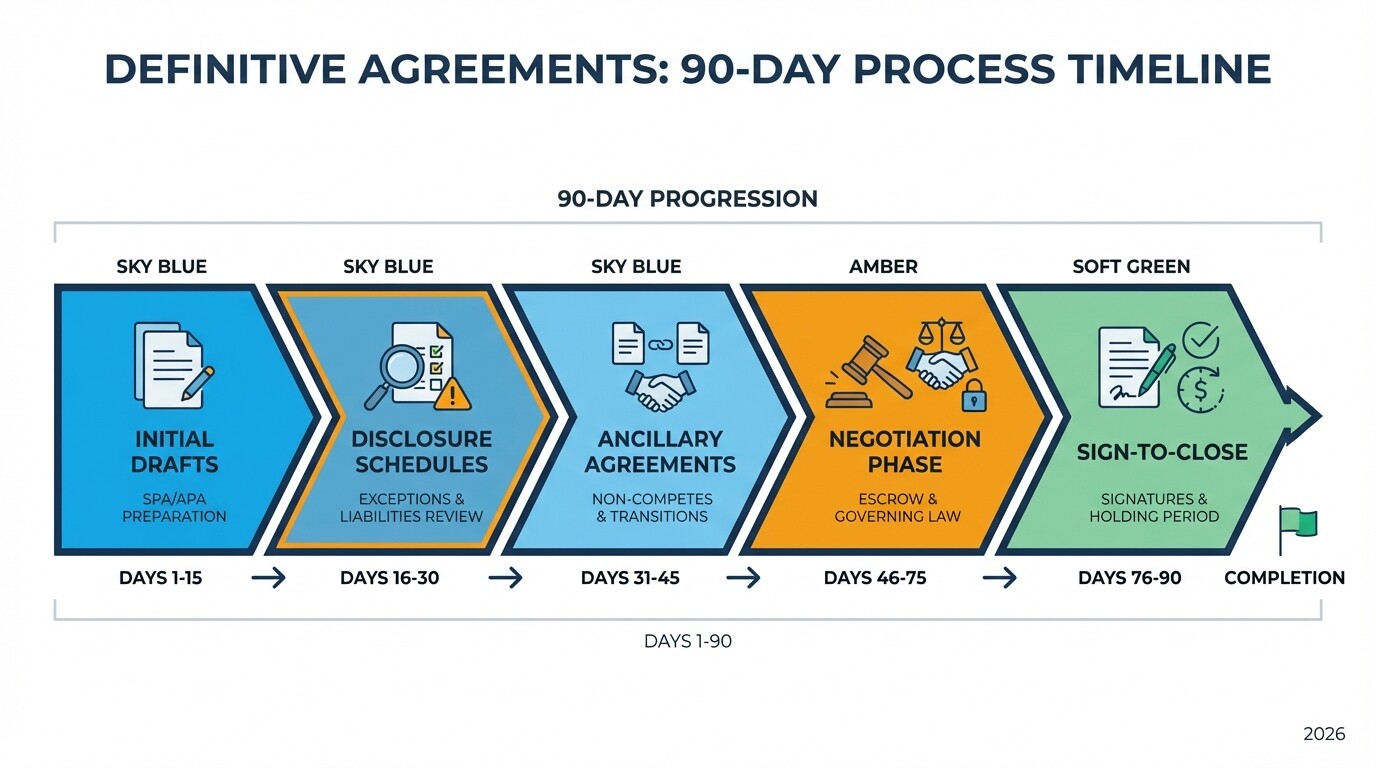

Timeline for Definitive Agreements

Drafting and executing purchase agreements takes 45 to 90 days. This runs concurrently with the later stages of due diligence.

- Initial drafts (Days 1-15): The buyer's legal counsel prepares the Stock Purchase Agreement (SPA) or Asset Purchase Agreement (APA). This includes representations, warranties, and indemnification rules.

- Disclosure schedules (Days 16-30): The target company provides lists of exceptions to the warranties. Buyers review these to identify liabilities.

- Ancillary agreements (Days 31-45): Counsel drafts supporting documents like non-compete agreements, transition services, and executive employment contracts.

- Negotiation phase (Days 46-75): Both parties exchange revisions. Foreign buyers focus on escrow amounts, governing law (usually Delaware), and dispute resolution.

- Sign-to-close (Days 76-90): Parties sign the agreements. If regulatory approvals are pending, the deal enters a holding period before the final exchange of funds and shares.

Legal Liability Risks for Foreign Entities

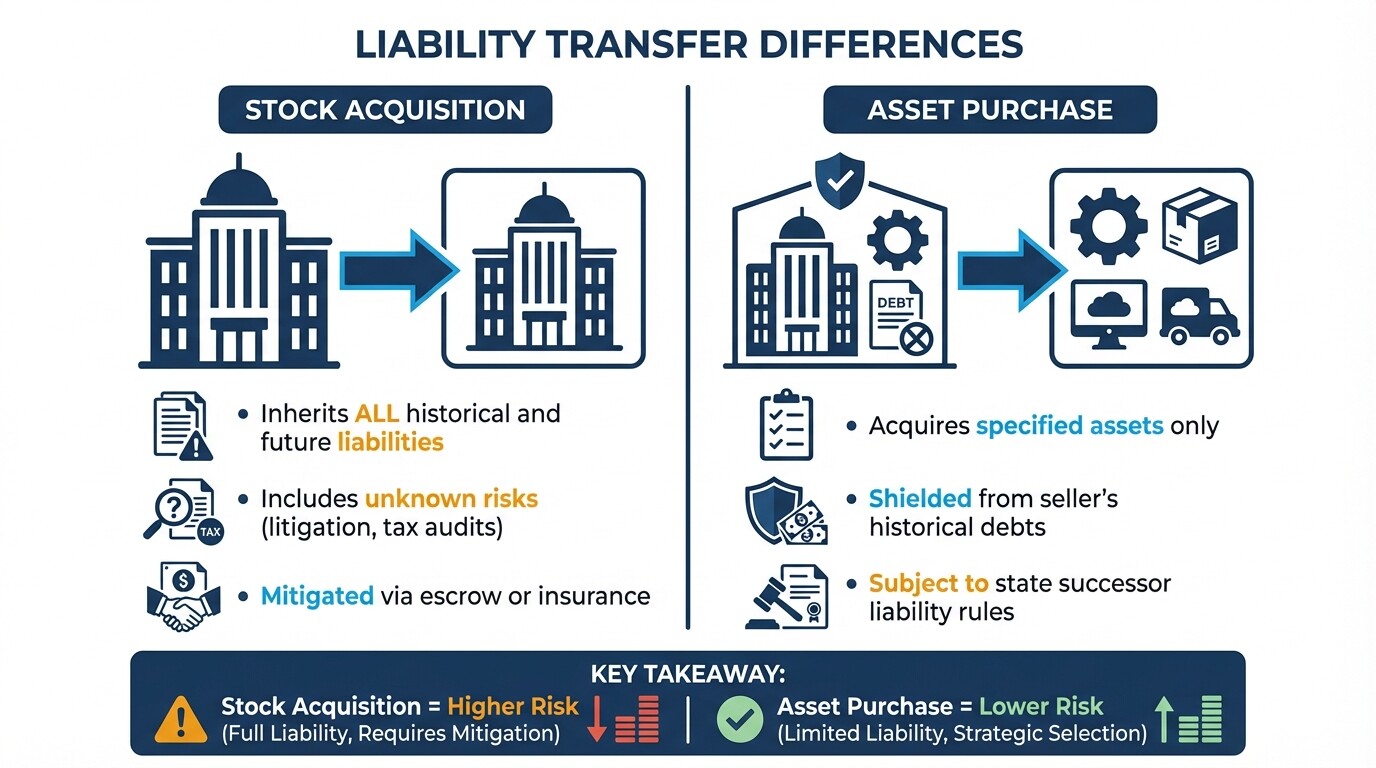

A foreign parent company faces different liability exposures based on the acquisition structure. In a stock acquisition, the buyer acquires the target company entirely. All historical and future liabilities transfer automatically. In an asset purchase, the buyer acquires specified assets and assumes only identified liabilities.

- Stock acquisitions: Foreign buyers inherit unknown liabilities, such as pending litigation, tax audits, and employment violations. Buyers mitigate these risks using escrow holdbacks or warranty insurance.

- Asset purchases: Buyers are shielded from the seller's historical debts.

- Successor liability: US courts sometimes impose successor liability on a foreign buyer in an asset purchase. This happens if the transaction is a fraudulent attempt to escape debt or if the buyer continues the exact same business operations.

- Corporate veil: Foreign corporate entities can hold US assets directly. However, buyers typically establish a domestic US subsidiary (like a Delaware LLC) to serve as the direct acquiring entity. This protects the foreign parent from US liabilities and simplifies tax reporting.

Regulatory Approvals and Due Diligence

Foreign acquisitions of US businesses face federal scrutiny over national security and market competition. Buyers must complete due diligence before triggering these formal reviews.

The Hart-Scott-Rodino (HSR) Act requires parties in large transactions to notify the Federal Trade Commission and the Department of Justice. This triggers a mandatory 30-day waiting period. If the government issues a "Second Request" for more information, the timeline extends by several months.

Foreign investments involving critical technologies, infrastructure, or sensitive personal data require review by the Committee on Foreign Investment in the United States (CFIUS). A standard CFIUS review takes 45 days. Complex cross-border deals frequently enter an additional 45-day investigation phase. CFIUS jurisdiction heavily targets civilian sectors, including healthcare data, financial technology, semiconductor manufacturing, and real estate near sensitive US government facilities.

Tax Obligations and Profit Repatriation

The M&A structure determines the immediate US tax burden and how profits return to the home country. Asset purchases generally favor the buyer for US domestic tax purposes. Stock purchases require international tax planning.

- Depreciation benefits: In asset purchases, buyers receive a step-up in the tax basis of the acquired assets to their fair market value. The foreign buyer's US subsidiary claims higher depreciation deductions, lowering US taxable income.

- Double taxation: Stock acquisitions retain the historical tax basis of the assets. Unless buyers make specific tax elections (such as an IRS Section 338 election), they lose the benefit of stepped-up depreciation.

- Withholding taxes: When the US subsidiary pays dividends back to the foreign parent, the IRS imposes a 30 percent withholding tax. Bilateral tax treaties reduce this rate to 15 percent, 5 percent, or zero percent, depending on the foreign parent's home jurisdiction.

Alternative Market Entry Strategies

If the timelines and risks of a full acquisition do not align with business goals, alternative structures allow foreign companies to leverage US operations with less upfront capital.

- Joint ventures: A foreign company and a US domestic company create a new, jointly owned US entity. The foreign entity accesses US distribution networks while sharing financial risk with a local partner.

- Minority investments: Purchasing a non-controlling stake in a US company gives a foreign business strategic influence. It may bypass certain antitrust filings, though CFIUS may still apply if the buyer accesses critical technology.

- Licensing agreements: A foreign entity can license its intellectual property or brand to an established US company. This generates US revenue with minimal corporate liability.

Common US Corporate Law Misconceptions

Foreign executives approach US acquisitions with assumptions based on their home country's legal systems. Misunderstanding US corporate law leads to delays and financial penalties.

- Complete risk elimination: While asset purchases reduce inherited liabilities, state-specific successor liability laws and bulk sales regulations can still force a buyer to pay the seller's unpaid taxes or environmental cleanup costs.

- Federal law governance: The United States operates under a dual legal system. Federal law governs antitrust and national security reviews. The actual purchase agreement, fiduciary duties, and corporate mechanics are governed by state law. Delaware is the most common jurisdiction.

Initiating Your US Acquisition

Engage legal counsel before signing a Letter of Intent or a Non-Disclosure Agreement. A specialized attorney conducts US-specific due diligence, structures the transaction for tax efficiency, and handles federal CFIUS filings. Attempting to negotiate terms without understanding Delaware corporate law or US antitrust thresholds exposes the foreign parent company to financial risk.

Define your strategic goals and determine whether acquiring specific assets or an entire corporate entity best serves your expansion. Assemble a deal team of legal and financial advisors who understand US regulations and your home country's compliance rules. Draft a Letter of Intent and engage with mergers and acquisitions lawyers in the United States to guide you through formal due diligence and regulatory filings.