- Jurisdiction Selection: Federal incorporation provides nationwide name protection, while provincial incorporation in British Columbia or Ontario avoids resident Canadian director requirements.

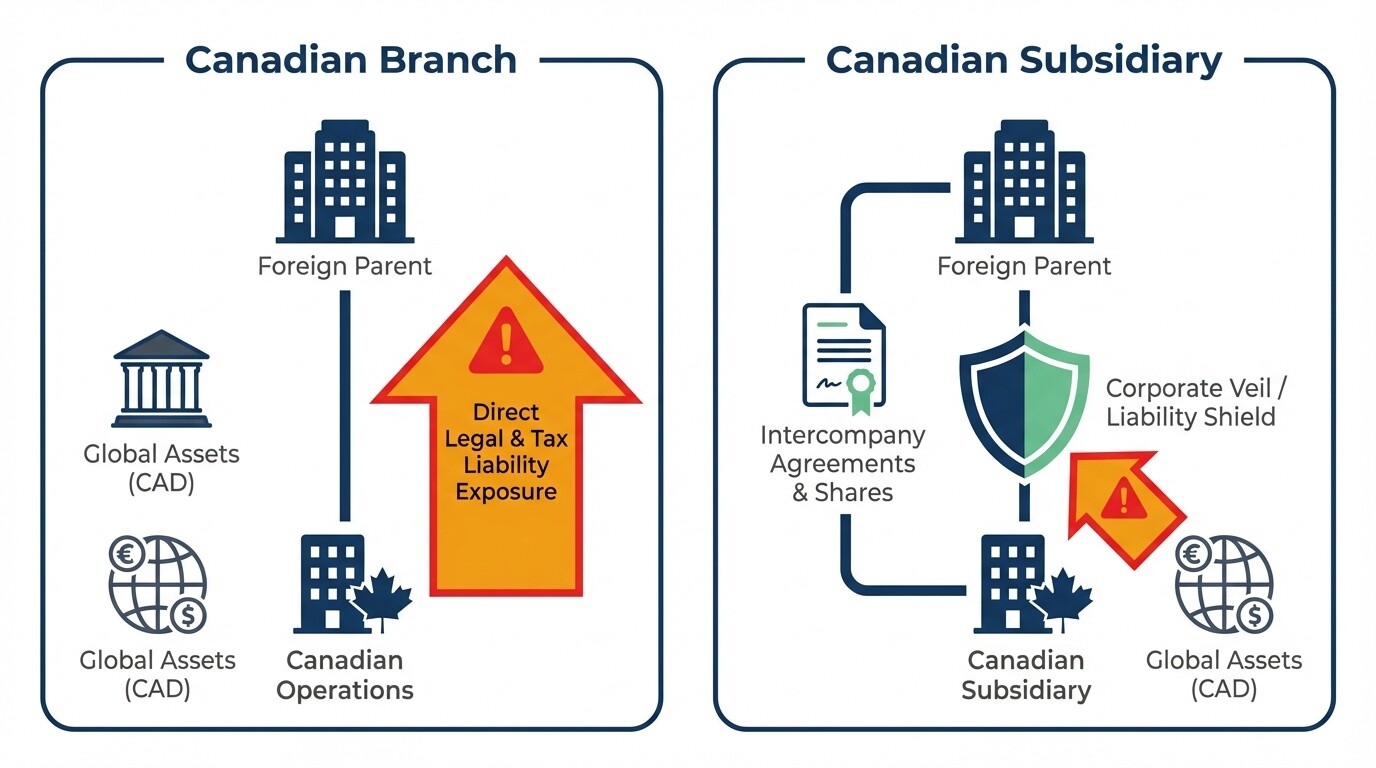

- Corporate Independence: A subsidiary is a distinct legal entity. Formal intercompany agreements are necessary to protect the foreign parent from local liabilities.

- Tax Compliance: The Canada Revenue Agency (CRA) enforces transfer pricing rules on intercompany transactions. You must document arm's-length pricing.

- Director Liability: Canadian corporate directors face personal liability for unpaid employee wages and unremitted taxes. Comprehensive indemnification agreements mitigate this risk.

- Deadlock Resolution: A Unanimous Shareholder Agreement (USA) establishes dispute resolution protocols and maintains parent company control.

Evaluating Federal vs. Provincial Incorporation

Foreign companies expanding into Canada must choose whether to incorporate their subsidiary federally under the Canada Business Corporations Act (CBCA) or provincially. Federal incorporation provides nationwide name protection. Provincial incorporation in British Columbia, Alberta, or Ontario offers flexibility regarding Canadian residency requirements for directors.

Jurisdiction choice affects your administrative workload and governance strategy. Even if you incorporate federally, you must register extra-provincially in every province where the subsidiary conducts business.

Foreign corporations can own 100% of a standard Canadian subsidiary, though regulated industries like telecommunications or aviation have foreign ownership limits. You do not need a commercial office space to incorporate, but you must maintain a physical registered address in your jurisdiction for legal service.

Government filing fees range from $200 to $350 CAD. Factoring in legal structuring, document drafting, and extra-provincial registration, total setup costs generally fall between $1,500 and $4,000 CAD.

| Feature | Federal (CBCA) | Ontario (OBCA) | British Columbia (BCBCA) |

|---|---|---|---|

| Resident Director Rule | 25% must be resident Canadians | No residency requirement | No residency requirement |

| Name Protection | Nationwide | Limited to Ontario | Limited to British Columbia |

| Incorporation Cost | $200 CAD | $300 CAD | $350 CAD |

| Best For | Nationwide brand protection | Operating primarily in Ontario | Structural flexibility |

Required Corporate Records

Managing a Canadian subsidiary requires maintaining precise corporate records and following local director residency mandates. An incomplete minute book attracts regulatory penalties and complicates financing or audit events.

The parent company and its Canadian directors must maintain the following corporate records at their registered Canadian office:

- Articles of Incorporation: Outlines share classes, share transfer restrictions, and board size.

- Corporate By-laws: Rules for internal management, including officer duties and meeting protocols.

- ISC Register: A mandatory transparency register identifying individuals who own or control 25% or more of the shares.

- Director Documents: Signed consents to act as a director and indemnification agreements protecting Canadian directors from personal liability for unpaid wages or tax remittances.

- Securities Register: A ledger tracking the issuance of shares to the parent company.

Intercompany Agreements and Parent Company Protection

Intercompany agreements define the relationship, financial transactions, and operational boundaries between the parent company and its Canadian subsidiary. These contracts protect the parent company from local liabilities and satisfy tax authorities during an audit.

Without formal contracts, courts or tax authorities may view the parent and subsidiary as a single entity. This exposes the parent's global assets to Canadian legal claims.

Sample Limitation of Liability Clause

When drafting a Management Services Agreement or Technology License between the parent and subsidiary, include language reinforcing corporate separateness:

Corporate Independence and Limitation of Liability: "The Parties acknowledge that [Parent Company] and [Canadian Subsidiary] are independent corporate entities. Nothing in this Agreement creates a partnership, joint venture, or agency relationship between the Parties. Under no circumstances shall [Parent Company] be held liable for the debts, obligations, or legal liabilities incurred by [Canadian Subsidiary] in the course of its domestic operations, except as expressly provided in a separate written guarantee."

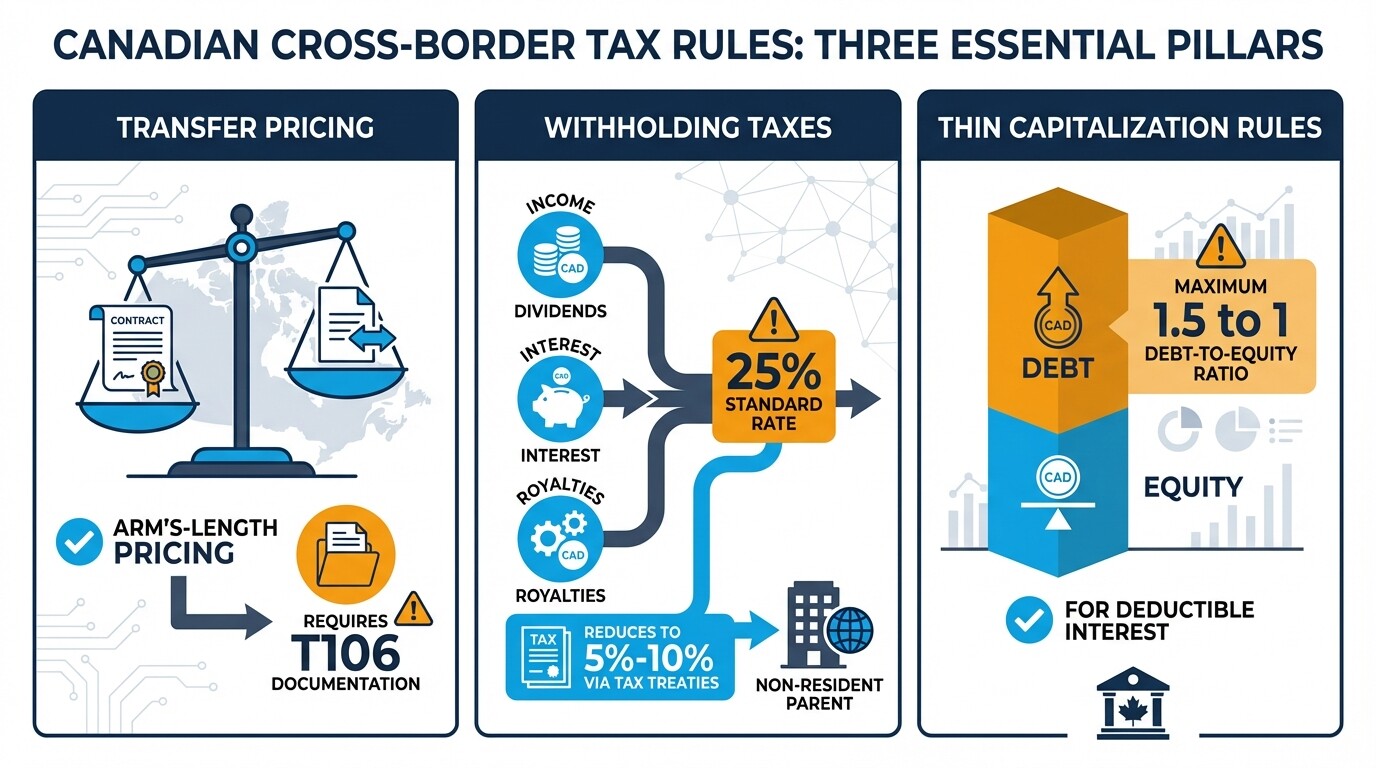

Cross-Border Tax Compliance and Transfer Pricing

Canadian subsidiaries pay domestic corporate income tax. Transactions with a foreign parent must comply with Canada Revenue Agency (CRA) transfer pricing rules. Pricing intercompany services, loans, or IP licenses below or above fair market value triggers tax penalties, adjustments, and double taxation.

- Transfer Pricing Documentation: The Income Tax Act requires Canadian subsidiaries to maintain contemporaneous documentation, such as a T106 form. This proves intercompany transactions mirror what independent parties would negotiate.

- Withholding Taxes: Canada imposes a 25% withholding tax on passive income (dividends, interest, royalties) paid to a non-resident parent. International tax treaties, such as the Canada-US Tax Treaty, often reduce this rate to 5% or 10%.

- Thin Capitalization Rules: The CRA restricts the interest a Canadian subsidiary can deduct on loans from non-resident shareholders. The debt-to-equity ratio generally cannot exceed 1.5 to 1.

Dispute Resolution and Governance Deadlocks

Governance deadlocks happen when a subsidiary's board of directors cannot reach a majority decision. This risk rises when parent company representatives and local Canadian directors disagree.

A Unanimous Shareholder Agreement (USA) prevents operational paralysis. A USA allows the shareholders to restrict the powers of the subsidiary's directors. Under Canadian corporate law, this transfers decision-making power directly to the parent company, ensuring absolute control over the Canadian entity's financial decisions.

Corporate governance best practices handle board deadlocks through specific mechanisms:

- Executive Escalation: The dispute moves away from the subsidiary board to the CEO or Board of Directors of the foreign parent company for a final decision.

- Casting Vote: The Chair of the subsidiary's board, usually a parent company representative, holds a tie-breaking vote.

- Mandatory Mediation: Parties must engage in binding arbitration or formal mediation in a Canadian jurisdiction before taking legal action to dissolve the subsidiary.

Common Misconceptions About Canadian Corporate Law

Foreign executives sometimes assume Canadian corporate law matches US or UK systems. This assumption leads to compliance errors.

- Subsidiary vs. Branch: A branch is an extension of the foreign corporation and exposes the parent to direct Canadian tax and legal liability. A subsidiary is a distinct Canadian corporation that shields the parent from direct liability.

- Employment Law: At-will employment does not exist in Canada. Terminating a Canadian employee, including a subsidiary director acting as an officer, requires reasonable notice or severance pay. You must factor this into corporate governance and executive contracts.

- Director Liability: Canadian directors do not have absolute limited liability. They can be held personally and strictly liable if the subsidiary fails to remit payroll taxes, GST/HST, or pay up to six months of employee wages.

Engaging a Corporate Governance Lawyer

Hire legal counsel before filing incorporation documents. A lawyer ensures your corporate structure aligns with your global tax and risk management strategy. They help navigate provincial residency rules, structure share capital for tax efficiency, and draft intercompany agreements. Working with corporate governance lawyers in Canada protects the parent company from unforeseen liabilities and ensures regulatory compliance.

Next Steps

- Select a Jurisdiction: Choose federal incorporation (CBCA) or a provincial registry like Ontario or British Columbia. Base this on your ability to supply resident Canadian directors and your requirement for nationwide name protection.

- Draft Governance Documents: Prepare the Articles of Incorporation, Corporate By-laws, and a Unanimous Shareholder Agreement to establish the parent company's operational control.

- Execute Intercompany Agreements: Sign licensing, management, and loan contracts between the parent and the Canadian subsidiary. Ensure all pricing is set at fair market value to satisfy CRA transfer pricing rules.